Nomura: Good (Data) Is Bad (For Assets) – The Difference Between R* & R**

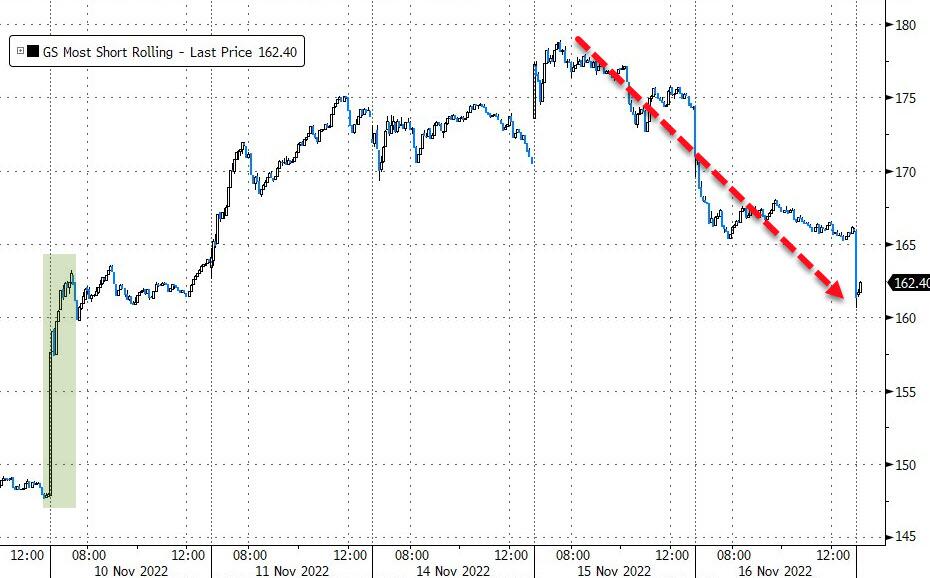

It certainly seems like people are taking off some of their US Equities “risk rentals” which have rallied so violently over the past week since the CPI downside surprise…

…and thematically, have even begun to lay back into their Shorts in all the trash that exploded 20% over the week…

…hence, US Equities Long Term Momentum factor +3.1% and Low Risk factor +3.0% again yday, respectively, as they feel the recent move has “overshot” particularly on the “expensive” / “unprofitable” stuff

And this morning, St.Louis Fed’s Jim Bullard poured even more cold water on the pause/pivot prayers as he hinted at even higher rates for longer.

As Nomura’s Charlie McElligott notes the resilience of the US economic data sits at the core of this renewed confidence in taking some shots again on “FCI tightening” trades, as we see the Bloomberg US Economic Surprise index reaching highs last seen in mid-May ’22, as data continues to beat expectations on the margin – Labor, Retail / Wholesale and Surveys / Biz Cycle Indicators bearing the concentration of the gains (while Housing, Industrials and Personal / Household sectors continue to drag)…

Translation: ”Good (data) is Bad (for assets)”…

As McElligott lays out, this all keeps coming-back to this recent NY Fed research paper concept of R* (neutral rate for the real economy) simply sitting in a totally different universe from R** (neutral rate for financial stability)…

It now seems abundantly clear that “markets” cannot handle much more rate hiking after a decade + of duration- and leverage- binging, as evidenced by the list of “market breakages” experienced over the past 12 months…

…but in the meantime, the real US economy (admittedly outside of Housing and structurally-shrinking Manufacturing sector) keeps banging along, where in peak (cringe) anecdotal fashion, restaurant ressies are “no offer,” luxury malls like Short Hills are packed with lines out of some of the most high-end retailers doors, airports are foaming at the mouth and airline tickets are running 2-3x’s ‘sanity levels,’ there is no locate on new Range Rovers in New Jersey until 2024….and all while New Yorkers are apparently lifting $21k Taylor Swift tickets for next Summer…

And this is why “High for Longer” continues to persist (Fed “Terminal” projections back above 5.00% this morning – but our house view is that it’s gonna have to push through 5.50-5.75, while GS took their Fed projection up yday as well)…

…it’s the same thing: the Inflation is going to soften down to 4-5% on pure base-effect math – but it’s not going to head back to 2% target if you don’t see actual job losses mount…bc right now, Labor and Wage gains are just too strong.

And because of that economic ‘strength’, equities still feel fragile:

-

The “sign of possible regime change” I highlighted in the last note – where US Equities Index Option Skew has steepened for 5 out of the past 6 days while Stocks violently rallied, standing in stark contrast to the perpetual flattening in Skew to 0%ile over the course of 2022 YTD – I believe has been a function of folks actually needing to hedge again, because they were starting to actually put on some exposure again after this violent “force-in” rally that very few people actually wanted to happen

-

And also as previously mentioned in recent weeks, my spidey senses too have been tingling with this persistent VIX Upside being sought for 6 consecutive weeks in size, most of it “wingy” / “crash” stuff

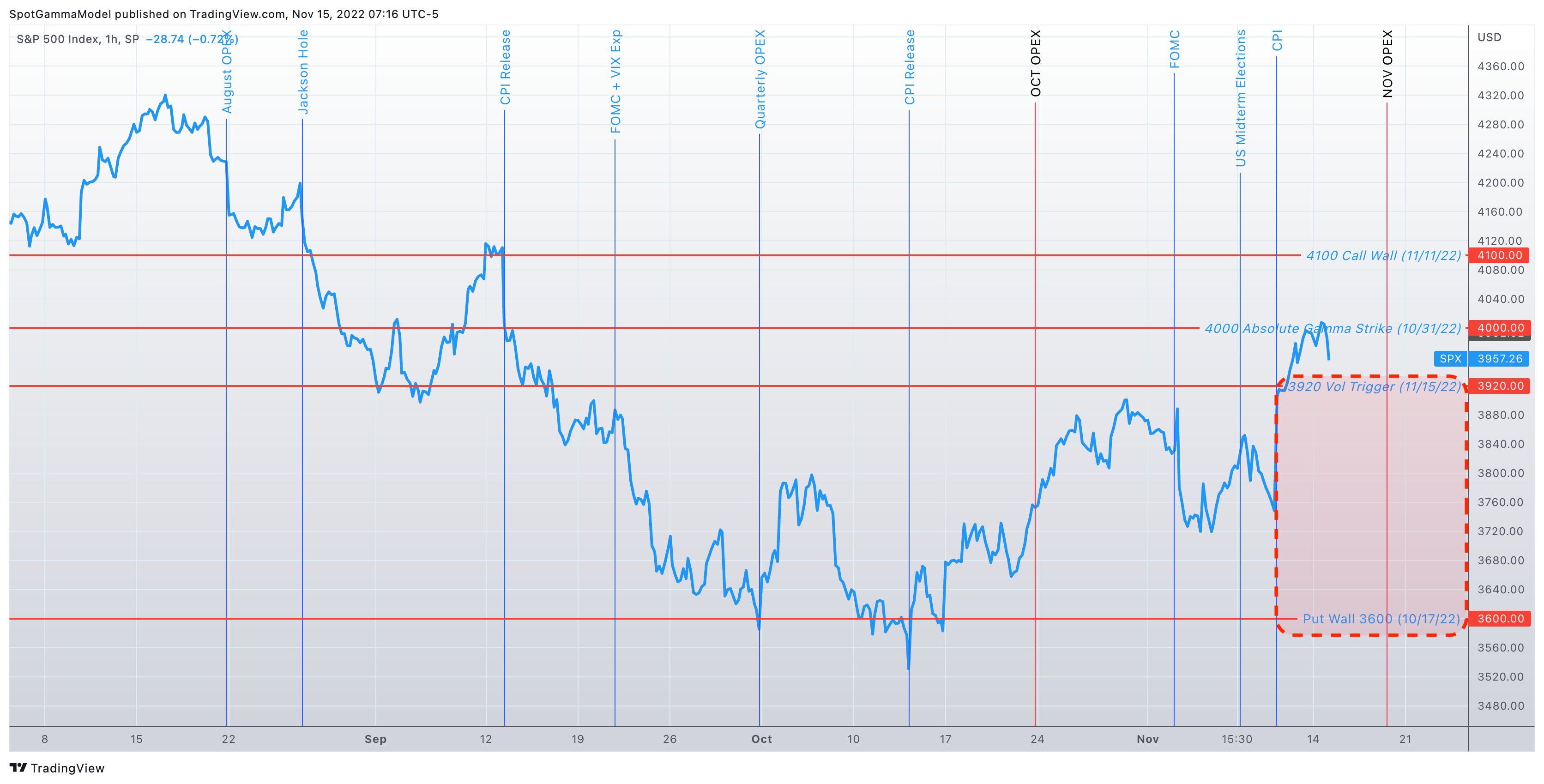

The S&P has tumbled back down to its 100DMA this morning…

…as we see Spot selloff this morning, we now see SPX back at “Gamma Flip” level as we speak (3918), while both QQQ and IWM have pushed back into “Short Gamma” territory

And as SpotGamma notes, that ‘negative gamma’-inspired volatility could be triggered with Fridays OPEX, and we have been therefore recommending adding some puts (here & here). The concern here is that we do not see much support of any kind from 3900 down to 3600 (chart here, description here).

{kind=link}

Tyler Durden

Thu, 11/17/2022 – 11:20

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com