Not All Yield Curves Are Alike… But This Signal’s Never Wrong

By Simon White, Bloomberg Markets Live reporter and strategist

Bull steepenings in the yield curve are generally seen as a precursor to a recession, but they are often preceded by bear steepenings. The 3m30y curve is currently bear steepening, indicating a recession could begin as early as the summer.

I discussed the 3m30y’s nascent steepening on Tuesday. Yield-curve inversions indicate a recession is on the way at some point, but it is the subsequent re-steepening that puts the downturn under starter’s orders.

Not all yield curves are alike, and typically it is the 3m30y curve that starts to steepen first, about five months before the recession’s onset. That curve has been steepening since mid-January, its longest stint without making a new low since it peaked last May.

A few readers pointed out that as this steepening is a bear steepening, with 30-year rates rising more than 3-month rates, it may be less of a concern, and it is bull steepenings that are a more imminent sign of recession.

It is true that bull steepenings are often more violent when the Fed does a volte-face as the economy deteriorates quickly, but bear steepenings are as much a part of the pre-recession picture, and have often preceded the bull steepening in the lead up to a slump.

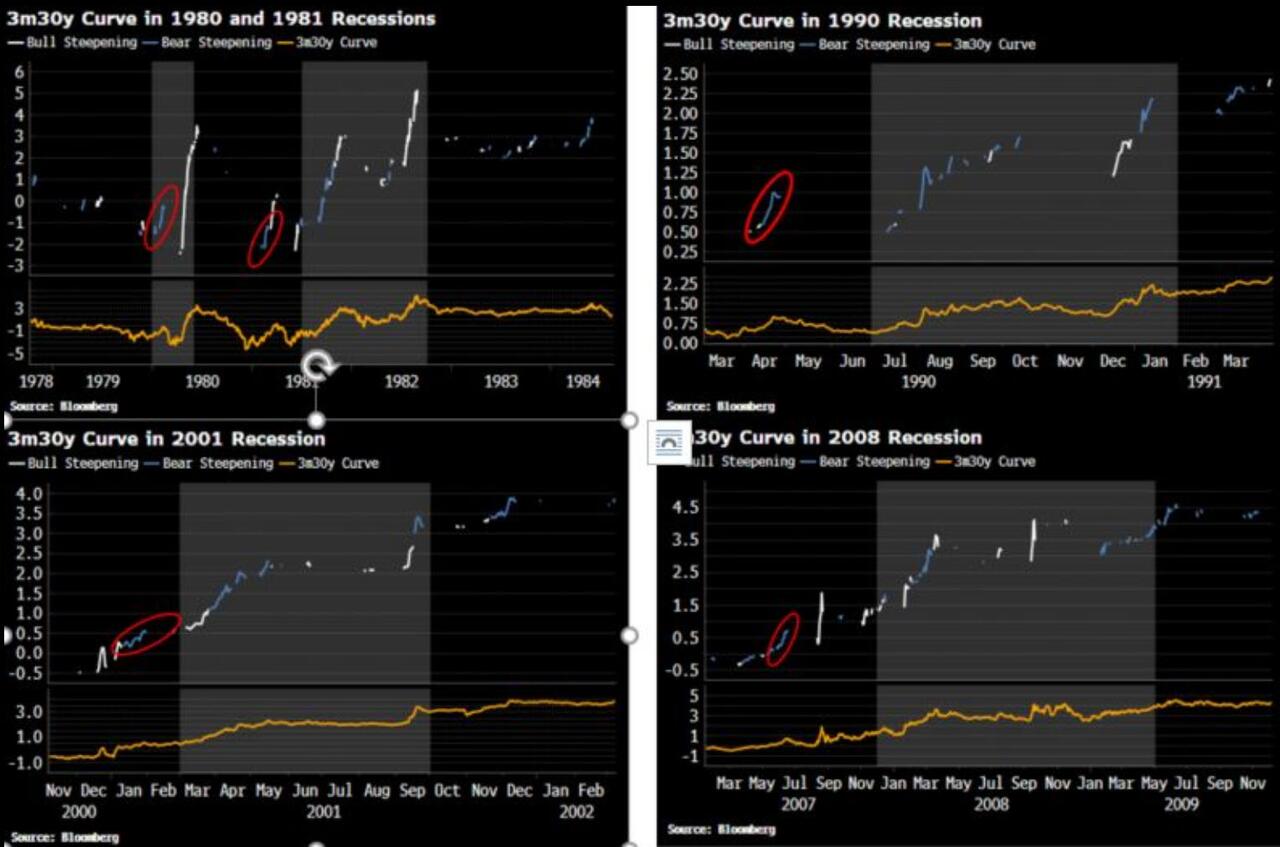

The charts below show the 3m30y curve around the last five (ex-2020) recessions. A bear steepening is defined as the 30y rate being higher over the last month, and the one, two, three and four-week change in the 30y rate being more than the one, two, three and four-week change in the 3m rate (and a bull steepening is defined analogously). This ensures we only capture meaningful steepenings.

As we can see, all the recessions (apart from 1980’s) were preceded by a significant bout of bear steepening in 3m30y about 3-9 months before the recession started. Bull steepenings tend to come later.

The recession itself is often a mix of bull and bear steepenings (as well as periods of flattening).

There are enough pockets of weakness in the economy that the recession sign from the 3m30y’s steepening – whether bear or bull – should still be paid attention to.

Bull steepenings tend to come later. The recession itself is often a mix of bull and bear steepenings (as well as periods of flattening).

There are enough pockets of weakness in the economy that the recession sign from the 3m30y’s steepening – whether bear or bull – should still be paid attention to.

Tyler Durden

Thu, 02/23/2023 – 07:20

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com