Big-Tech Trounces Small Caps As Rates Rip Ahead Of Powell

China growth forecasts sparked some weakness in crude (and bond yields lower) overnight but a smaller than expected drop in factory orders (and bounce in core orders) helped spark a rebound in everything… most notably, rate-trajectory expectations (with both the terminal rate rising and any hopes for cuts collapsing)…

Source: Bloomberg

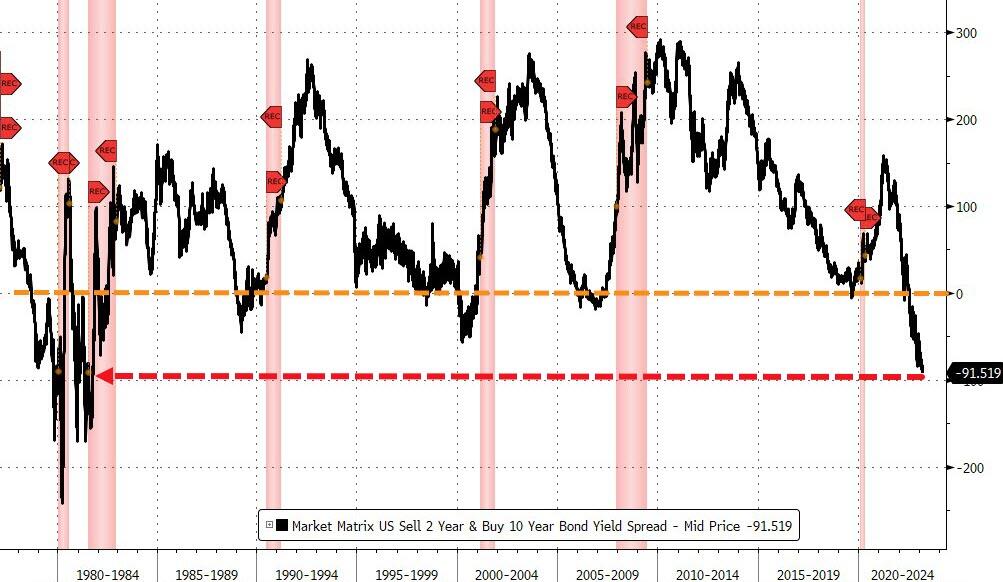

And at the same time, the yield curve (2s10s) pushed to a new cycle low, its most-inverted since Oct 1981, screaming recession…

Source: Bloomberg

But rates rising and recession rearing did not stop investors buying big-tech, but from shortly after Europe closed, US equities all saw selling pressure but Small Caps the biggest loser all day. The Dow, S&P, and Nasdaq gave back their earlier gains by the close ahead of Powell tomorrow…

Nasdaq (mega tech) outperformed Russell 2000 (small caps) by almost 2% – the most since Nov 2021 – with Nasdaq at its ‘strongest’ relative to Russell 2000 since Oct 2022…

Source: Bloomberg

Goldman upgraded Apple – which likely helped support the mega-caps – but the giant tech company’s stock hit a wall again at around $156…

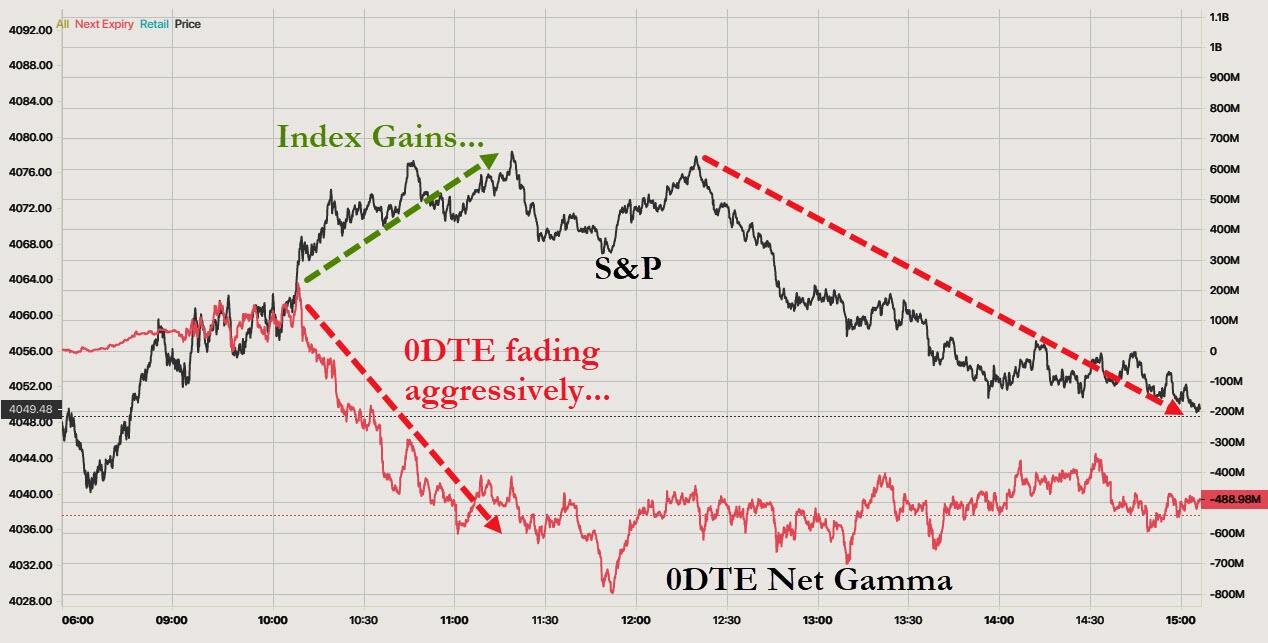

…and may help explain why early on we saw 0DTE traders fading the gains in the index (and then the index catching down to reality in the early afternoon)…

There was aggressive 0DTE put-buying from the cash open to around 1315ET, and not much give back…

Furthermore, the mega-caps dominated performance as the equal-weight S&P dramatically underperformed…

Source: Bloomberg

Value stocks underperformed growth once again, breaking to their relative weakest since Oct ’22…

Source: Bloomberg

It wasn’t a short-squeeze either as the early spike in “most shorted” faded shortly after the factory orders data…

Source: Bloomberg

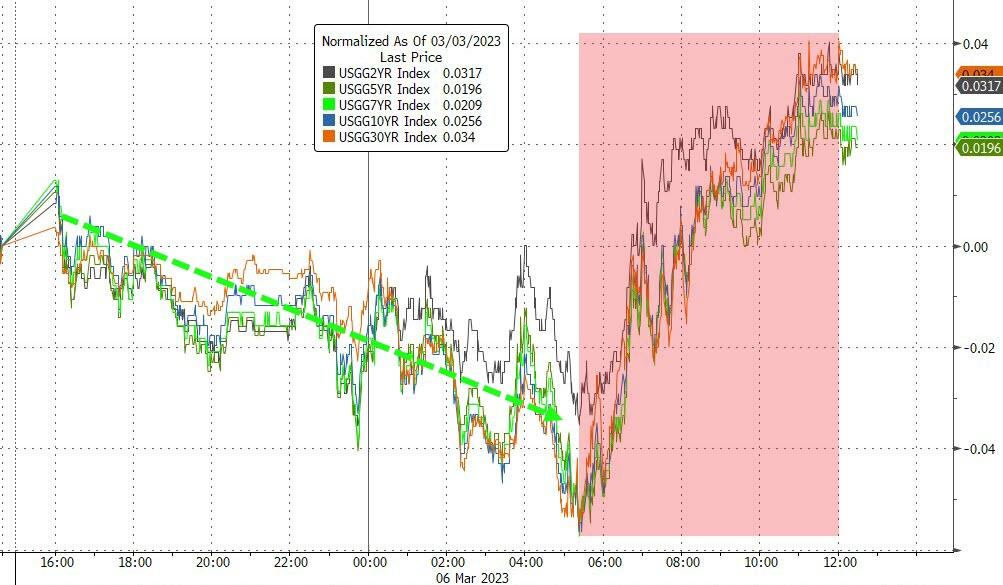

Treasury yields were higher across the curve with the belly modestly outperforming after rallying overnight (weaker China growth?). That’s around an 8-10bps surge in yields during the US session…

Source: Bloomberg

…with 10Y back up near 4.00%, but finding resistance at last week’s 3.98ish level…

Source: Bloomberg

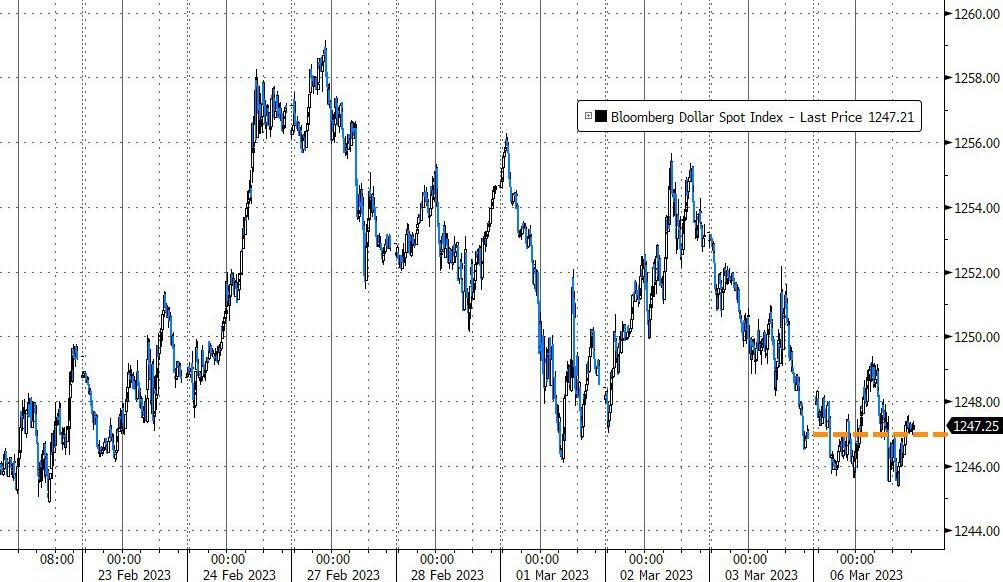

The dollar oscillated in a narrow range but ended the day basically unch…

Source: Bloomberg

Bitcoin drifted largely sideways after Thursday evening’s plungegasm…

Source: Bloomberg

Oil prices ended the day higher after early (China) weakness. WTI spiked back above $80, three-week highs…

Gold futures ended very modestly lower but held above $1850…

Having ripped back up to a $3 handle (after briefly tagging a $1 handle), US NatGas prices were clubbed like a baby seal today, puking over 13% as weather forecasts shifted milder over the weekend, slashing the outlook for heating demand at a time when larger-than-normal domestic inventories weigh on prices….

Finally, while investors are apparently more confident in the coming weeks, they are pricing considerably more uncertainty in to the markets this week…

Source: Bloomberg

With S&P implied vols notably elevated into payrolls (and Powell tomorrow), then fading back below 20 – and lower than at the start of last week.

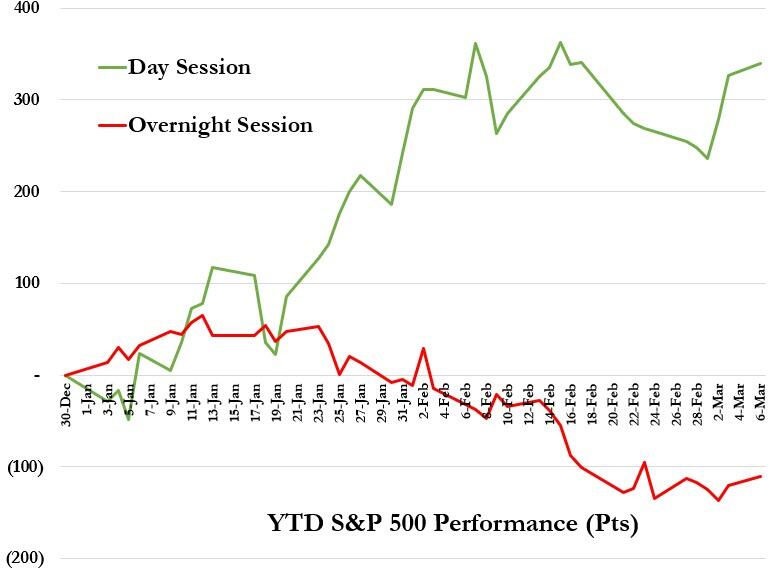

It’s also worth noting that the S&P has dramatically outperformed during the day-session in 2023 (relative to the overnight session)…

A very different regime from the last few years “easy trade”.

Tyler Durden

Mon, 03/06/2023 – 16:00

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com