Stockman: Raiding The Taxpayer Piggy-Bank

Authored by David Stockman via LewRockwell.com,

Janet Yellen is one continuous anti-prosperity horror show and the reason is obvious enough. She got her indoctrination at Yale from the granddaddy of Professor Keynes’ US disciples, James Tobin, in the late 1960s and has spent most of her years since then pontificating in academia or dictating from the Fed.

So now with the arrival of screaming evidence that the banking system desperately needs the disciplining effect of depositor flight, she comes out four-square for euthanizing the $9 trillion of still uninsured deposits in the US banking system.

But let’s cut to the chase. Banks not disciplined by their depositors and not at risk for deposit flight are dangerous institutions. They leave bank executives free to swing for the fences on the asset-side of their balance sheets without fear that attentive depositors will move their money to safer pastures.

For crying out loud. It was bad enough during the last several years when deposits were dirt cheap and knuckleheads like those who ran SVB decided to load up their balance sheets with 10-30 year duration assets against overnight demand deposits, most of which were uninsured.

For the moment that allowed them to book outsized profits and reap the consequent benefit of soaring stock options, but these “profits” were phony as a two-dollar bill. That’s because they were being generated off long-term fixed income assets, the prices of which had nowhere to go except down.

For want of doubt, here is the inflation-adjusted yield on the 10-year UST through the beginning of the Fed’s belated anti-inflation campaign in March 2022. No one in their right mind should have believed these deeply underwater yields were sustainable; and no banker capable of running even a credit union in Podunk Iowa would have matched up overnight deposits with these long-duration securities—investments which were absolutely heading for a nose-dive in value.

Indeed, at the March 2022 bottom, the real 10-year UST yield stood at -6.4%, the lowest level in the 60-years shown in the chart, and undoubtedly the lowest rate ever—since prior to that time the nation’s central bank actually believed in sound money, zero inflation and market-based interest rates.

In a word, anybody who bought long-term treasuries or agency securities at the bottom of the purple line in the chart below should have had their head examined. And most certainly they shouldn’t have been running a multi-billion bank.

Inflation-Adjusted Yield On 10-Year UST, 1962 to March 2022

Nonetheless, Janet Yellen and her fellow Washington clowns got themselves warmed-up last week by bailing-out $155 billion of uninsured deposits at SVB—deposits that had been wantonly put in harm’s way by reckless management on a stock-pumping joy ride.

To wit, between 2020 and 2021 SVB’s assets nearly doubled from $115 billion to $211 billion, while the HTM (securities held to maturity) portion of that balance sheet literally exploded from $17 billion to $98 billion. And more than 95% of this massive HTM book had maturities of 10-years or more!

Here’s the thing. These fools massively mismatched their book even without the safeguard of deposit insurance. What in the world is going to happen when deposits are 100% insured?

More importantly, there is no substitute for career-destroying penalties when they result from the towering incompetence embodied in the blow-up of banks like SVB. Yet in that very regard it turns out that one of the senior financial officers at SVB had apparently gotten his financial training at, well, Lehman and Enron!

So if nothing else, we need deposit flight and bank failures to purge the bad actors, incompetents and reckless cowboys from the banking industry. Yet the de facto policy is now that no depositor can loose money, no bank can fail and no one’s resume should be besmirched.

Whatever that is, it’s not market-based capitalism. And its going to lead to massive waste and malinvestment, not bank-fueled prosperity.

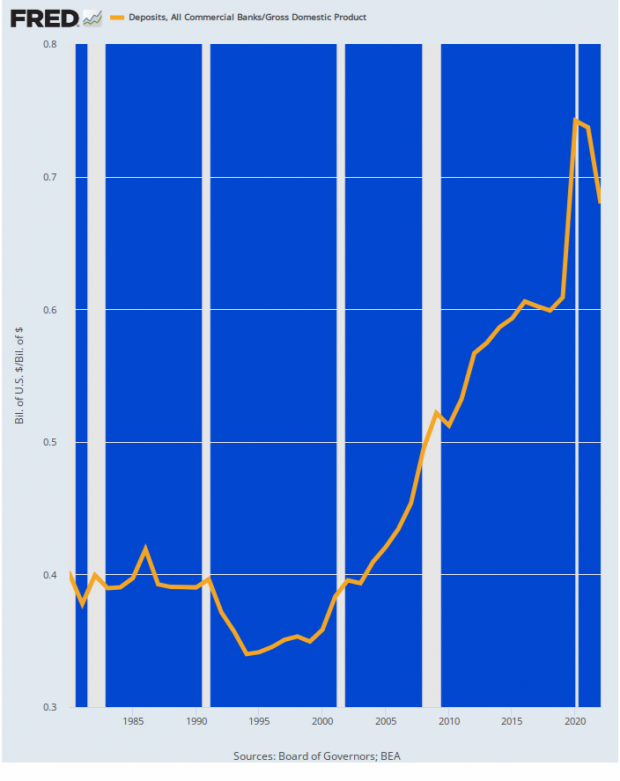

In any event, the chart below shows that the banking system is already extremely dangerous, and that compounding the risk via 100% deposit insurance would amount to lighting the match.

In a word, over the last decade especially the Fed has flooded the financial markets with so much liquidity that the banking system has been literally drowned in excess deposits and reserves. As shown below, banking system deposits have historically been about 40% of GDP, but since the turn of the century that ratio has gone vertical, rising to more than 70% of GDP during the most intense periods of money-printing during 2020-2021.

The flooding of the zone with deposits has been especially acute since the pre-crisis peak in November 2007. During the 15 years since then, total bank deposits have soared from $6.6 trillion to $17.6 trillion or by 6.2% per annum. And in the period since March 2020, that growth rate has accelerated to nearly 10% per annum.

By contrast, since Q4 2007 nominal GDP has expanded by just 3.8% per annum. Yet all thing equal, savings and the resulting bank deposits would have grown at the same rate as GDP. They actually grew at almost double the GDP rate, of course, because the Fed was running the printing presses so red hot that much of the new money never left the financial system, backing up into the banking system, instead.

Bank Deposits As A Percent Of GDP, 1962 to 2022

Needless to say, all of these deposits had to be put to work, and aggressive managements quickly figured out the new banking ball-game. To wit, under the post Dodd-Frank regulatory regime the banking system was switched from one which was constrained by cash reserves (to meet a surge in depositor withdrawals) to one which was purportedly capital-driven based on the standards fashioned by the Bank for International Settlements.

Had the regulators been content to go with plain vanilla capital ratios, the new regime might not have been a total disaster. But naturally the bank lobbies got their hands on the rule-writing process and determined that a spade was not a spade.

That is, not all assets were treated as equal when it came to computing capital ratios. In fact, government debt was determined to be risk-free, requiring no capital backing whatsoever. So banks did what regulators implied they should do—they loaded up with government and agency debt because it required dramatically less capital backing.

In turn, this “capital-light” regime was great for stock prices and executive stock options. Instead of plowing a goodly portion of earnings into capital for growth they allocated it to dividends and stock buybacks, instead. The gamblers in the stock markets were thrilled.

For instance, from JPMorgan’s $258 billion of net income posted over 2015-2022 about $189 billion or 73% was paid out to shareholders in the form of stock buybacks ($102 billion) and dividends ($87 billion). During the same period, however, JPM’s total assets grew from $2.352 trillion in 2015 to $3.666 trillion in 2022.

Since the Fed was fueling asset inflation and repressing money market interest rates during that same period, this 56% growth of total assets was the equivalent of a printing press. The bank’s net interest margin soared, causing its net income to flourish and its market cap to surge from $225 billion in 2015 to a peak of $500 billion in late 2021.

But all that shareholder magic was not just because Jamie Dimon is some-kind of latter day financial Einstein. JPM’s half trillion dollar market cap was partially thanks to the capital-light regulatory regime.

Thus, in 2015 JPM’s ratio of book equity to total assets had stood at 10.50%, which would be minimally safe in a world without “too -big-to-fail”. But as it happened, by 2022 its equity ratio had actually fallen to just 7.97% as the bank loaded up on capital-free government securities.

The implication of that is straight forward. To maintain its 2015 equity ratio JPM would have needed $385 billion of book equity by 2022, not the $292 billion it actually reported. So to actually accomplish the robust asset growth that fueled its fulsome earnings gains it would have needed to retain $93 billion more of its net income over the period.

That is to say, its payouts to Wall Street in the form of stock-buybacks and dividend would have been cut in half! The gamblers would not have been so pleased.

Needless to say, based on this illustration it is easy to see why banks went whole hog buying long-duration governments. It drastically conserved capital, permitting fulsome payouts of dividends and stock buybacks.

On the other hand, the Fed’s ostensible reason for flooding the financial system with cheap credit was to goose bank lending levels, and thereby allegedly fuel stronger economic growth. But again in the case of JPM it is evident that didn’t happen.

In 2015 its loan book stood at $824 billion, which accounted for 64.4% of its $1.28 trillion of deposits. By 2022, however, its loan book at grown only modestly to $1.11 trillion, but that amounted to just 47.7% of deposits, which had soared to $2.34 trillion.

In short, even if it was a good idea to artificially stimulate more loans, which it is not, that didn’t happen despite all of the Fed’s reckless money-printing. Instead, the new money flooded into banks, which bought government bonds and thereby aided the Congressional borrow-and-spend contingent, while at the same time enabling reckless bank managements to take on massive amounts of long-term Treasury and Agency securities at the rock-bottom of an interest rate cycle that will not be seen again for decades to come, if ever.

Yet notwithstanding these realities Yellen last Sunday afternoon launched a campaign to drastically further weaken the banking system by essentially abolishing the last vestiges of depositor scrutiny and discipline. We are referring to the abominable bailout of all depositors at SVB and Signature Bank, but especially the so-called Bank Term Facility Program (BTFP). The latter was bad enough, since it allowed banks to borrow 100 cents on the dollar against 30-year bonds which lost 40% of the market value last year.

But now Yellen’s gone full retard, suggesting outright guarantees of all deposits, regardless of size:

“The steps we took were not focused on aiding specific banks or classes of banks. Our intervention was necessary to protect the broader U.S. banking system,” Yellen said.

“And similar actions could be warranted if smaller institutions suffer deposit runs that pose the risk of contagion.”

As the Wall Street Journal noted this AM “the sound and fury of demands for universal deposit insurance are growing”. For instance, the chronic Wall Street whiner and entitled brat, Bill Ackman, is demanding his bacon be saved via 100% deposit insurance. But so is the usually sensible (on public policy, that is) Elon Musk.

As the financial press breathlessly reported this AM, the Treasury Department staff is reviewing whether federal regulators have enough emergency authority to temporarily insure deposits greater than the current $250,000 cap on most accounts without formal consent from a deeply divided Congress, according to people with knowledge of the talks.

The bolded phrase tells you all you need to know. How in the world after at least 40-years of Congress’ refusal to insure bank deposits at 100% regardless of size, can you have a legitimate decision to take on a $9 trillion liability in behalf of the taxpayers by executive decree?

Indeed, if that isn’t a decision for the representatives of the people to make, we don’t know what is—if you want to even pretend we have a democracy.

After all, 100% deposit insurance would mean that the $125 billion FDIC fund would be guaranteeing $18 trillion of deposits. They can say that the necessary funds—which might rise into the hundreds of billions or even trillions under certain loss scenarios—would come out of FDIC insurance premiums, but c’mon. That would be a giant tax by any other name because all 108 million US households with bank accounts would ultimately pay the premium in the form of lower rates on their deposits.

Not surprisingly, of course, the Washington lobbies have already gotten involved big time in attempting to force thru this profoundly anti-democratic action. To wit, the Mid-Size Bank Coalition of America, which includes banks with assets of as much as $100 billion, urged regulators to lift the current cap on deposit insurance, according to a March 17 letter reviewed by Bloomberg. The organization expressed concern that, if another regional lender fails, more depositors will move their money to the nation’s largest banks, regardless of the underlying health of their smaller competitors.

So what!

Perhaps these virtuous small bankers should have been thinking about the risk of deposit flight when they loaded up their balance sheets with higher yielding assets bearing both interest rate and/or credit risks. Absent these factors, in fact, there is no reason why a conservative bank would be at risk of deposit flight or be unable to weather a temporary flight by borrowing at the Fed’s discount window.

That’s exactly what happened in the last week. The weekly change in discount window borrowings soared to $138 billion, nearly on par with the $180 billion gain during the traumatic first week of October 2008.

Weekly Change In Fed Discount Window Borrowings, 1980 to 2023

Of course, the crybabies in the small and mid -sized bankers brigade don’t like the discount window because there is allegedly a stigma attached to it, and because the current discount rate is 4.75%—well above their average deposit costs. In short, they want some cheap money from Uncle Sam so they can run a asset/liability mismatch, book fulsome earnings and laugh all the way to the bank account for their stock options.

At the end of the day, we are truly getting to the end of the road with this form of crony capitalism and socialization of losses for the big guys wearing the long-pants.

While the usual bipartisan suspects are now busy fixing to pass legislation raising the deposit insurance limit to way above $250,000, at least the House Freedom Caucus has figured out what is at stake and has come out solidly against a 100% guarantee.

Since they won an option to call for Speaker McCarthy’s removal at the time of his election to the job, let’s hope they are ready, willing and able to use it when any semblance of the 100% deposit insurance legislation is brought to the House floor. That’s how much is really at stake.

“Any universal guarantee on all bank deposits, whether implicit or explicit, enshrines a dangerous precedent that simply encourages future irresponsible behavior to be paid for by those not involved who followed the rules,” the House Freedom Caucus said in a statement.

* * *

Reprinted with permission from David Stockman’s Contra Corner.

Tyler Durden

Sat, 03/25/2023 – 14:30

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com