Welcome To Japanification, Where Yields See No Floor

Authored by Bloomberg macro strategist, Laura Cooper

Welcome to the new global era of Japanification, where bond yields will struggle to find a floor as the policy race to zero and beyond propels advanced economies toward tepid inflation and stagnant growth.

Policy makers are unleashing their limited arsenal to cushion the coronavirus shock. Wednesday’s aggressive rate cut from the Bank of England followed the Federal Reserve and others, and hopes are high for the European Central Bank to surprise on Thursday after Christine Lagarde warned of a 2008-like hit to growth.

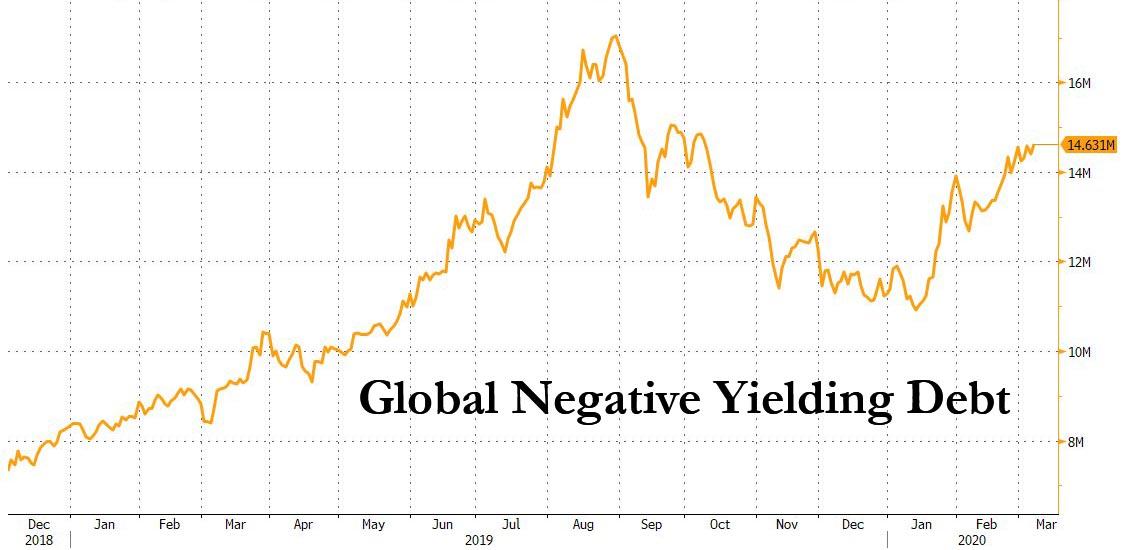

Negative rates are fast becoming the norm. This week, negative-yielding debt jumped to nearly $15 trillion…

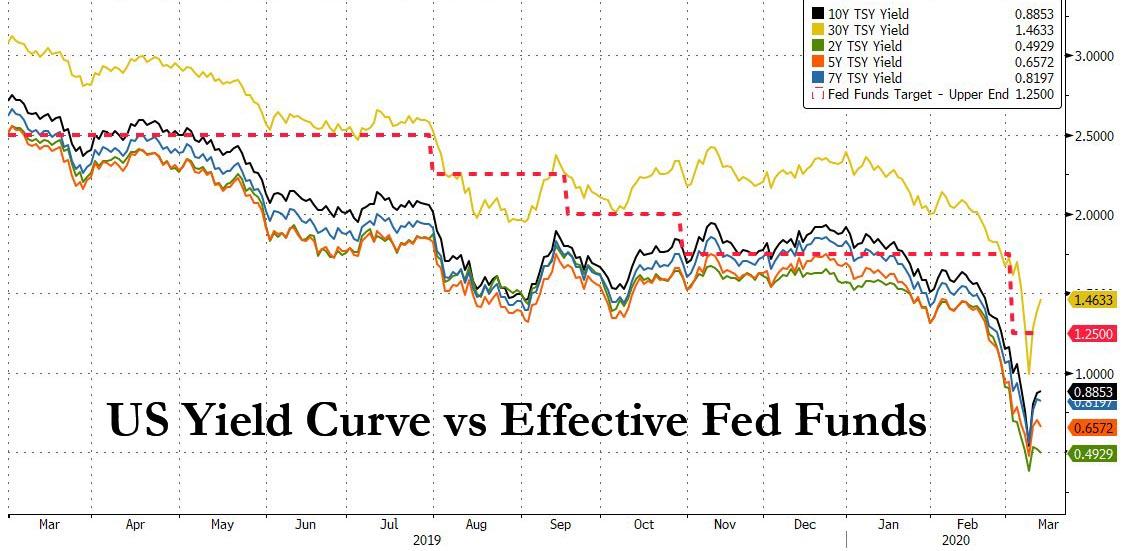

… the short- end of the U.K. curve briefly hit sub-zero for the first time and the entire U.S. curve fell under 1%.

All before the full and still unknown effects of the virus shock have fed through to economic data.

Yet emergency cuts alone accelerate the structural shift to monetary policy impotence. Officials across advanced economies deployed coordinated conventional easing from late 2007 through mid-2009. This included the Fed and the BOE who each cut about 500bps, the BOC at 425bps and the ECB at 375bps.

Prior to the Lehman collapse, major developed central banks altogether had about 4,150bps of room above zero in conventional rate cuts. It was just above 600bps on March 2, and this has been reduced by 175bps since.

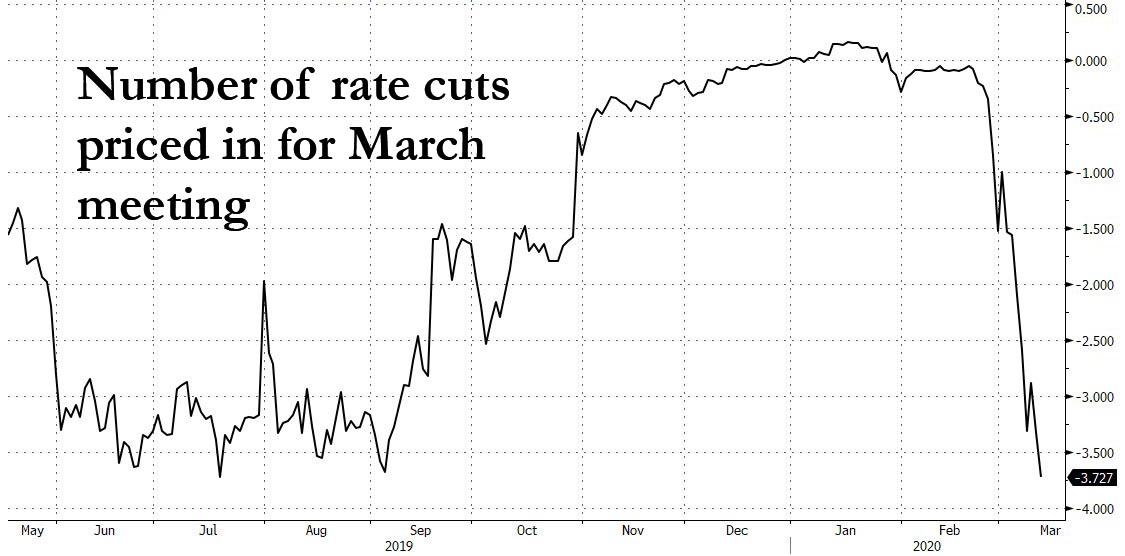

Yet markets continue to bank on cuts – pricing suggests advanced economies will all approach the zero lower bound over the coming 12 months, with five extending deeper into negative.

One could argue the proximity to the zero lower bound in the U.S. and U.K. warrants aggressive policy action to front-run stimulus for more of an impact.

But cheaper money on its own is unlikely to boost demand amid uncertainty and would leave central banks with less future fire power should the global economy tip into recession. It’s clear investors want to see coordinated and targeted stimulus measures that go beyond rate cuts, judging by their contrasting reactions to the Fed and BOE moves.

The trap of disinflationary pressures and stagnant growth is also diminishing central banks’ capacity to lift confidence, let alone market-implied inflation expectations, which are plumbing near record lows in the U.S and Europe. Exhausting the tools of rate cuts and quantitative easing have yet to spur price pressures.

Investors have pinned their hopes on fiscal stimulus, which have so far fallen short of market expectations given a piecemeal approach. The lack of productivity-enhancing measures and a grinding demographic shift are further aggravating the pernicious environment of subdued inflation and low rates.

Beyond the fanfare of emergency cuts, the possibility of the zero lower bound becoming the upper bound got a boost this week. What was previously a floor for bond yields now looks like a trapdoor.

Tyler Durden

Thu, 03/12/2020 – 17:45![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com