Confirmed: Fed Bailed Out Hedge Funds Facing Basis Trade Disaster

Back in December, when the world was still confused about what exactly happened before (and after) the September repocalypse – which has since exploded thousand-fold resulting in the Fed now doing daily $1 Trillion repo operations – we said that in addition to the implicit bailout of JPM (which we described here first, and subsequently others), by restarting its repo operations the Fed was also bailing out dozens of hedge funds engaging in highly levered trades involving a relative value compression trade in the Treasury cash/swap basis… almost identical to what LTCM was doing ahead of its 1998 bailout, which is also why we titled the article “The Fed Was Suddenly Facing Multiple LTCMs.”

In a nutshell, the article explained why and how the return of the Fed’s repo ops was nothing more than the Fed preemptively bailing out all those hedge funds that would have imploded had basis trades gone haywire. Below is a key excerpt from that post:

One increasingly popular hedge fund strategy involves buying US Treasuries while selling equivalent derivatives contracts, such as interest rate futures, and pocketing the arb, or difference in price between the two. While on its own this trade is not very profitable, given the close relationship in price between the two sides of the trade. But as LTCM knows too well, that’s what leverage is for. Lots and lots and lots of leverage.

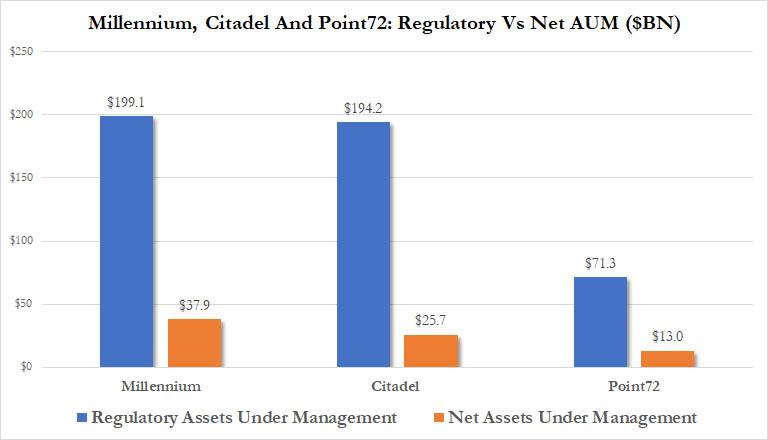

We also said that “hedge funds such as Millennium, Citadel and Point 72 are not only active in the repo market, they are also the most heavily leveraged multi-strat funds in the world, taking something like $20-$30 billion in net AUM and levering it up to $200 billion. They achieve said leverage using repo.”

Needless to say, as always when this website presents something the mainstream press hasn’t even considered, our explanation of what really happen ahead and during the September repocalypse was met with the traditional mockery and derision by the financial “intelligentsia.”

Until today, three months later, when Bloomberg finally confirmed everything we said.

In an article discussing how and why the Fed unleashed its March 12 repo bazooka, Bloomberg writes that “when coronavirus panic kicked off unprecedented turmoil in Treasuries last week, hedge fund leverage was lurking” and goes on to “explain” something we said back in December:

The [hedge funds] use borrowed money from the repurchase market for the popular basis trade, which exploits price differences between cash Treasuries and futures. Though individual firms’ borrowing is a closely guarded metric, people familiar with the transactions said some of them levered up as much as 50 times their own wagers. Leveraged funds’ exposure to the basis strategy could be as much as $650 billion, JPMorgan Chase & Co. strategists said.

Does that sound like “the Fed suddenly facing multiple LTCMs”? Because to us it sure does. And more importantly, what happened in the days ahead of last week’s credit market debacle is precisely what happened ahead of the September repo snafu, only with exponentially more destructive power.

The catalyst for last week’s re-repocalypse was the historic surge in Treasurys that saw the 10Y drop as low as 0.31%, and the 30Y drop below 1%. As investors scrambled into Treasurys, “hedge funds got hammered” again, and the result was “a difficulty in completing trades” which as Bloomberg correctly writes “was a contributing factor to the Federal Reserve’s decision to pledge $5 trillion to keep markets running smoothly.”

High leverage amplifies profits and losses and can be responsible for forced liquidations — and market fluctuations. This week, a sell-off in Treasury futures tied to margin calls pushed outstanding contracts to their lowest level since 2018. Many firms also get funding from money markets, whose problems have prompted the Fed to provide emergency funding

And there it is – just as we said, the Fed’s first priority in the bailout waterfall, long before consumers and businesses were even considered, was the sanctity and stability of those multibillion hedge funds that suddenly faced a spectacular implosion… just like in the case of the original LTCM. Only it’s even more poetic, because whereas with LTCM – which blew up when an economic black swan (the Russian default and the Asian crisis of 1997) blew out the LTCM basis trades, forcing the first Fed bailout in the modern era, what happened last week may have been the very last bailout cascade in Fed history, only this time it will involve everything, not just one solitary hedge fund run by idiot Nobel-prize winners.

“Too big to fail is back, and this time it’s not the banks, it’s levered financial institutions,” said Mark Yusko, the chief executive officer of Morgan Creek Capital. Yusko – who apparently forget to the original Fed bailout was not of a bank but of a levered financial institution (LTCM) said he supported the Fed’s stepping in, but added that hedge fund firms have gotten too big by borrowing too much. “It’s a bailout,” Yusko said, repeating what we said in December.

And whereas Bloomberg failed to connect the dots last year, this time around it actually did some original reporting and found some of the smaller funds that would have been devastated had the Fed not stepped in with its trillion-dollar a day repos:

- ExodusPoint Capital Management lost 4% this month through March 13, on pace for its worst month ever, according to people familiar with the situation. It was unclear how much the basis trade contributed to the loss.

- An LMR Partners’ fund fell 12.5% in the first two weeks of this month and spurred the firm to raise new capital.

- Capula Investment Management’s Global Relative Value Fund dropped 5.2%, people said, and Field Street Capital Management’s fixed-income relative-value flagship fund, in which the basis trade is substantial, sank 14.5% and had to reduce the size of its positions.

That said, that’s just three macro hedge funds out of a universe of hundreds, and what is important, is that the trade was so ubiquitous (thanks to those hedge fund idea dinners) that everyone was doing it.

“We’ve had 10 years of a perfect paradise and so people have been picking up pennies thinking there’s no risk in holding strategies like the basis trade,” said Kathryn Kaminski, chief research strategist and portfolio manager at AlphaSimplex Group. “A lot of the strategies, like the basis, that hedge funds tend to use don’t work when markets aren’t stable. You’ll see more of these types of blowouts.”

Curiously, and contrary to totally unfounded recent rumors, some of the far bigger firms fared better: as Bloomberg notes, the market unwind had a relatively small impact on multi-strategy funds Citadel and Millennium Management, although as we reported yesterday Millennium is closing several “trading pods” after weathering a modest 2.7% drop this month through March 12, and was down 1.9% for the year. In light of the S&P’s 30% drop, that may seem like a stunning performance, but somehow Izzy Englander always manages to pull out a rabit out of hat (someone may want to check into what the HFT guys on the 6th floor of 666 Fifth are doing for the answer to that).

But whereas the mega-levered Millennium and Citadel, whose in house risk-management lackeys are truly draconian in their position limits, managed to avert a debacle by unwinding the positions quickly after sustaining small losses – courtesy of the Fed’s massively expanded $500BN repos – others were not so lucky, and many other firms focuses on the basis trade suffered far steeper losses.

One among them was BlueCrest Capital Management, whose trader Raymond Wang was fired on March 9, the day after that historic Sunday night when the 30Y traded bidless for hours as the S&P crashed limit down, because he couldn’t find a buyer for the investment firm’s losing positions in the basis trade. Other firms, who had less leverage on, survived until that Thursday when the Fed launched the repo bazooka, allowing all those who had the basis trade on to quietly exit stage left, bailed out by a deceiving Fed that told the world its mission was to rescue main street when in reality it was just making sure the billionaires had someone to dump their money-losing positions to.

Tyler Durden

Fri, 03/20/2020 – 22:24![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com