The Whirr Of Helicopter Blades: Regime Change Is Coming

Authored by Peter Tasker via PeterTasker.asia,

“The coronavirus pandemic is a public health emergency. But it is also an economic emergency…

This national effort will be underpinned by government interventions in the economy on a scale unimaginable only a few weeks ago. This is not a time for ideology and orthodoxy… We will support jobs, we will support incomes, we will support businesses, and we will help you protect your loved ones. We will do whatever it takes.”

– UK Chancellor of the Exchequer Rishi Sunak 18/3/2020

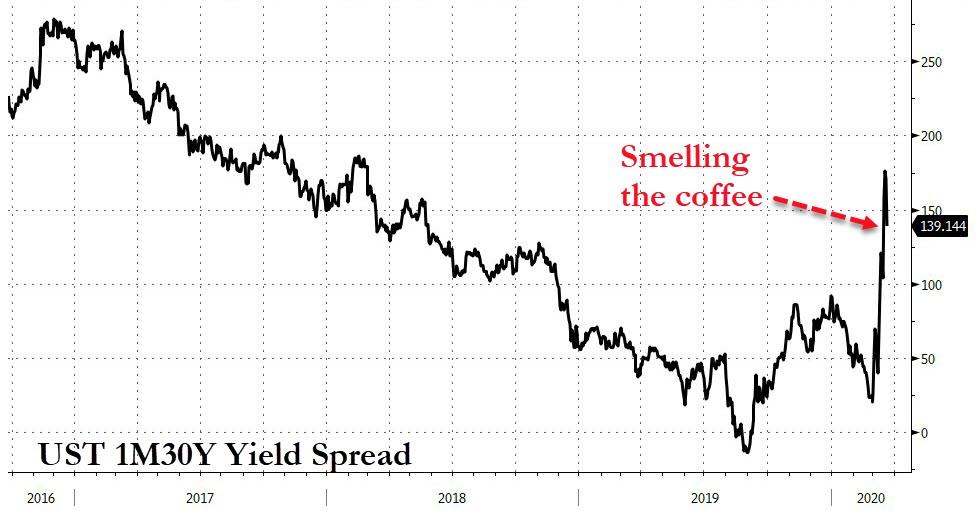

Policy-makers are scared, and rightly so. The coronavirus pandemic has delivered a massive deflationary shock to the world economy, as evidenced by the collapse in the yield on US 10 year government bond to a momentary low of 0.31% on March 9th.

A severe decline in economic activity is an inevitable side-effect of applying the precautionary principle to the virus crisis, which is nonetheless the correct course of action. The same goes for economy policy; underestimating the risks is a far worse mistake than overestimating them. Economic crises kill people too. After Japan lurched into deflation in the late 1990s, suicides leapt by an annual 10,000 cases and stayed at an elevated level for a decade. That increase constitutes a worse toll every year than the global tally for the coronavirus to date.

As this is not a financial crisis – though a wave of bankruptcies and asset price collapses could turn it into one – protecting incomes and jobs has to be the main priority. Quite how this is done will differ from country to country, but ultimately the financial resources can only be provided by governments via bond issuance supported by central banks. A simultaneous reversion to quantitative easing, as has occurred in the United States, clears the way for outright monetization.

“Today, I am making available an initial £330 billion of guarantees – equivalent to 15% of our GDP.. That means any business who needs access to cash to pay their rent, the salaries, suppliers, or purchase stock, will be able to access a government-backed loan, on attractive terms. And if demand is greater than the initial £330 billion I’m making available today, I will go further and provide as much capacity as required. I said whatever it takes –and I meant it.”

– UK Chancellor Rishi Sunak 18/3/2020

“Loans” that are used to fund running costs like wages and rent are unlikely to be paid back. Probably they will end up being deep-sixed in government accounts, along with several other non-performing assets such as student loans and public-private investments. The scale, though, will be far larger.

In the US, President Donald Trump’s more straightforward approach includes cutting payroll taxes and mailing $1000 cheques to American citizens. Although the Trump package is enormous, equivalent to 6% of US GDP, it has been criticized for being insufficient in scale, given the risks of a deep downturn. If it doesn’t work, more will surely follow. This is, after all, a presidential election year.

The key point is that money is likely to flow directly to households, as it never did when monetary policy was the only game in town. How does this differ from “helicopter money”, Jeremy Corbyn’s “People’s QE”, or the proposals of believers in Modern Monetary Theory? In essence it doesn’t, except that the proponents are the leaders of nominally conservative administrations. If the crisis does not abate soon, governments could end up monetizing the wages and salaries of a very large number of people and owning significant slices of industry.

What does all this mean for investors? In all probability, an end to the monetary policy-dominated regime in place since the Global Financial Crisis of 2008 and the investment landscape it created. A reckoning for hyped-up growth stocks on sky-high valuations. An avalanche of bond issuance. Growing risks of inflation. Currency turmoil if central banks attempt to hold yields down once normalization begins.

With a few brief blips, interest rates have been flat or declining for most of the careers of today’s government officials, investors and corporate managers. In recent years, there has been a growing belief that low rates are “structural”, driven by long-term deflationary factors such as demographics and the rise of the internet economy. If that is true, governments can borrow and spend as much as they want with no fear of the consequences.

Thanks to the coronavirus, that theory is about to be tested. And, as we have always suspected, ground zero for regime change will be not Japan or the United States, but the UK.

Tyler Durden

Sat, 03/21/2020 – 10:30![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com