The Everything Bubble, Fictitious Capital, & COVID-19

Authored by Frank Lee via Off-Guardian.org,

The years since the 1970s are unprecedented in terms of their volatility in the price of commodities, currencies, real estate and stocks. There have been 4 waves of financial crises: a large number of banks in three, four or more countries collapsed at about the same time. Each wave was followed by a recession, and the economic slowdown which began in 2008 was the most severe and most global since the great depression of the 1930s.”

Manias, Crashes and Panics – Kindelberger and Aliber

Interestingly enough 1971 was the year when Nixon took the world off the gold standard, which had been in effect since 1944. Fiat-bugs please note.

More to the point, however. Booms and busts have always been normal in a capitalist economy. But in recent years this has been a feature which has been exacerbated by and involves that part of the economy indicated by the acronym FIRE (Finance, Insurance and Real Estate) and its growing importance in the economy in both qualitative and quantitative terms.

Financialisation is a process whereby financial markets, financial institutions, and financial elites gain greater influence over economic policy and economic outcomes. Financialisation transforms the functioning of economic systems at both the macro and micro levels. Its principal impacts are to:

-

elevate the significance of the financial rent-seeking sector relative to the real value-producing sector

-

transfer income from the real value-producing sector to the financial sector

-

increase income inequality and contribute to wage stagnation

Since 1970 this part of the economy has grown from almost nothing to 8% of US Gross Domestic Product (GDP). This means that one dollar in every ten is associated with finance. In terms of corporate profits finance’s contribution now represents around 40% of all corporate profits in the US. This is a significant figure and, moreover it does not include those overseas earnings of companies whose profits are repatriated to their countries of origin.

Thus, the increasing presence and role of finance in overall economic activity and the increase of profits channelled to the financial sector represent the salient indicators as to what has been termed financialization. It is argued by some that financialization may put the economy at risk of debt deflation and prolonged recession.

Financialisation operates through three different conduits:

-

changes in the structure and operation of financial markets,

-

changes in the behaviour of nonfinancial corporations, and

-

changes in economic policy.

Countering financialisation calls for a multifaceted agenda that:

-

restores policy control over financial markets

-

challenges the neoliberal economic policy paradigm encouraged by financialisation

-

makes corporations responsive to interests of stakeholders other than just financial markets

-

reforms the political process so as to diminish the influence of corporations and wealthy elites

The rent-seeking nature of finance is common to all forms of insurance, banking, monopolistic pricing, and property. This has not always been the case, or at least wasn’t as pronounced as it is at present. There was a time when the banking system was junior partner in the relationship between banks and industry. Banks provided industry with loans for investment with a view to maximising profit for both. This is patently not the case today.

Generally speaking, banks will lend for property purchases, stock buy-backs, and perhaps loans for dubious mergers and acquisitions. Moreover, when we speak of ‘profits’ this has now assumed a rather obscure meaning. Profits were generally understood as a realization of surplus value.

Firms made stuff – goods and services – which had a value, which was then sold on the market at a profit. Given the competitive nature of the system, firms invested in increased capital formation and output which increased productivity, surplus value and ultimately profit.

With regard to Investment banks like Goldman Sachs and the commercial banks they do not create value; they are purely rent-extractive. For example, commercial banks make a loan out of thin air, debit this loan to the would-be mortgagee who then becomes a source of permanent income flow to the bank for the next 25 years.

Goldman Sachs makes year-on-year ‘profits’ by doing – what exactly? Nothing particularly useful. But then Goldman Sachs is part of the cabal of central banks and Treasury departments around the world. It is not unusual to see the interchange of the movers and shakers of the financial world who oscillate between these institutions. Hank Paulson, Mario Draghi, Steve Mnuchin, Robert Rubin … on and on it goes.

This financialised system now moves in ever-increasing levels of instability. But what did we expect when the whole institutional structure – its rules, regulations and practises – were deregulated and finance was let off the leash.

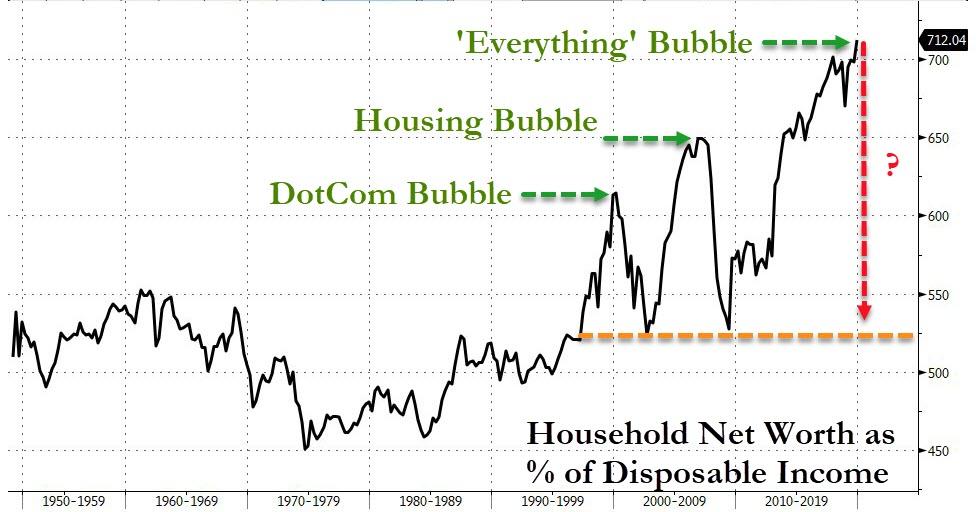

Thatcher, Reagan, the ‘Big Bang’ had set the scene and there was no going back: neoliberalism and globalization had become the norm. From this point on, however, there followed a litany of crises mostly in the developing world but these disturbances were in due course to move into the developed world. Serial bubbles began to appear.

US stock prices [which of course would only ever go up] began to decline in the Spring of 2000, and fell by 40% in the next three years. Whilst the prices of NASDAQ stocks decline by 80%.”

Manias, Panics and Crashes – Kindleberger and Aliber

Chastened monies moved out of this market and into property speculation. It is common knowledge what happened next. The run-up to 2008 was floated on a sea of cheap credit. The price of stocks pushed property prices to vertiginous heights until – pop, went the weasel.

The reason was quite simple. Any boom and bust has an inflexion point where boom turns to bust. This is when buyers incomes, and borrowers inability to extend their loans could no longer support the rise in the price level. Euphoria turned to panic as borrowers who once clamoured to buy were now desperate to sell. 2008 had arrived.

The strange thing, however, regarding the property price boom-and-bust was that it was based upon pure speculation. Prices went up, prices went down. Some – a few – made money, quite a few lost money. Investors were wondering what had happened to their gains which they had made during the up phase. Where had all that money gone?

The short answer is – nowhere. It was never there in the first place. It was fictitious capital. Gains which had appeared and then disappeared like a will ‘o’ the wisp. As opposed to physical capital – machinery, labour and raw materials, and money capital which enabled through purchase the production of value to take place, we have fictitious capital which is a claim on future production. If my house goes up by 10% that is a capital gain, if everybody’s house goes up by 10% that is asset-price inflation

Fictitious capital is a by-product of capitalist accumulation. It is a concept used by Karl Marx in his critique of political economy. It is introduced in chapter 25 of the third volume of Capital. Fictitious capital contrasts with what Marx calls “real capital”, which is capital actually invested in physical means of production and workers, and “money capital”, which is actual funds being held.

The market value of fictitious capital assets (such as stocks and securities) varies according to the expected return or yield of those assets in the future, which Marx felt was only indirectly related to the growth of real production. Effectively, fictitious capital represents “accumulated claims, legal titles, to future production’’ and more specifically claims to the income generated by that production.

The moral of the story is that it is not possible to print wealth or value. Money in its paper representation of the real thing, e.g., gold, is not wealth it is a claim on wealth.

Of course, this would be lost on establishment economists, bankers, and financial journalists, whose view is that the policy should be QE, liquidity injections, and so forth. A one-trick pony.

And what has all of this to do with Coronavirus? Well, everything actually.

I take it that we all knew that the grotesquely overleveraged world economy was heading for a ‘correction’ but that’s a rather a soothing description. “Massive correction” would be a better description. That is the nature of the beast. The world was a bubble of paper money looking for a pin. It found one.

Have a nice day all.

Tyler Durden

Mon, 03/23/2020 – 23:25![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com