So far in March, the data indicates that the yearly growth rate of our measure for US money supply (as measured by the AMS metric) stood at 10.5 percent against 6.6 percent in February and 1.7 percent in March last year.

Given that the Fed is busy throwing money at the economy as if there were no tomorrow, it is tempting to suggest that the momentum of the AMS is likely to increase further and that consequently runaway inflation could emerge in no time.

However, in response to the massive decline in real economic activity, it is possible that banks’ generation of loans out of thin air, i.e., through fractional reserve lending, could fall sharply.

For the time being, the annual growth of our measure for this type of credit—also known as inflationary credit—stood in March at 14.1 percent versus 7.4 percent in February and 3.4 percent in March 2019.

If the momentum of inflationary credit were to fall sharply, it would likely cause the yearly growth rate of money supply to follow suit (see chart). Consequently, a sharp fall in price inflation could emerge. If this were to happen, the government and the central bank would intensify their spending and money pumping to counter the deflation.

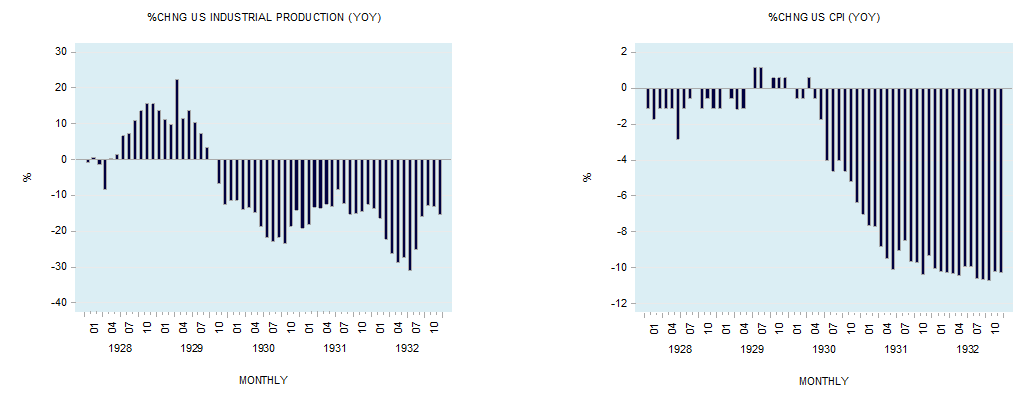

A general decline in the prices of goods and services is regarded as bad news, since it is seen to be associated with major economic slumps such as the Great Depression of the 1930s.

In July 1932, the yearly growth rate of industrial production stood at –31 percent while the yearly growth rate of the consumer price index (CPI) stood at –10.7 percent by September 1932 (see chart).

Is the Fall in Prices Bad News?

Contrary to popular belief, there is nothing wrong with declining prices. In fact it is the essential characteristic of a free market economy to select those commodities as money whose purchasing power grows over time. What characterizes an industrial market economy under a commodity money such as gold is that the prices of goods follow a declining trend. According to Joseph Salerno,

In fact, historically, the natural tendency in the industrial market economy under a commodity money such as gold has been for general prices to persistently decline as ongoing capital accumulation and advances in industrial techniques led to a continual expansion in the supplies of goods. Thus throughout the nineteenth century and up until the First World War, a mild deflationary trend prevailed in the industrialized nations as rapid growth in the supplies of goods outpaced the gradual growth in the money supply that occurred under the classical gold standard. For example, in the US from 1880 to 1896, the wholesale price level fell by about 30 percent, or by 1.75% per year, while real income rose by about 85 percent, or around 5 percent per year.1

In a free market the rising purchasing power of money, i.e., declining prices, is the mechanism that makes the great variety of goods produced accessible to many people. On this Murray Rothbard wrote,

Improved standards of living come to the public from the fruits of capital investment. Increased productivity tends to lower prices (and costs) and thereby distribute the fruits of free enterprise to all the public, raising the standard of living of all consumers. Forcible propping up of the price level prevents this spread of higher living standards.2

Most experts argue that a general fall in prices is always “bad news,” for it postpones people’s buying of goods and services, which in turn undermines investment in plants and machinery. All this sets in motion an economic slump. Moreover, as the slump further depresses the prices of goods, it intensifies the pace of economic decline.

For consumers to postpone their buying of goods because prices are expected to fall would mean that people have abandoned any desire to live in the present. But without the maintenance of life in the present no future life is conceivable.

Should “Bad” Price Deflation Be Fought?

Even if we were to accept that price declines in response to an increase in the production of goods promotes the well-being of individuals, what about the case in which a fall in prices is associated with a decline in economic activity? Surely, this type of deflation is bad news and must be fought against.

The Problem with Money Creation

Whenever a central bank pumps money into the economy, it benefits various individuals engaged in activities that sprang up on the back of loose monetary policy, and it occurs at the expense of wealth generators. Through loose monetary policy, the central bank gives rise to a class of people who unwittingly become consumers without first making any contribution to the pool of real saving. Their consumption is made possible through the diversion of real savings from wealth producers. They only take from the pool of real savings and do not contribute anything in return.

Observe that both consumption and production are equally important in the fulfillment of people’s ultimate goal, which is the maintenance of life and well-being. Consumption depends on production, while production depends on consumption. The loose monetary policy of the central bank breaks this bond by creating an environment where it appears possible to consume without producing.

Not only does easy monetary policy push the prices of existing goods up—or prevent goods from becoming less expensive—but the monetary pumping also gives rise to the production of goods which are demanded by non–wealth producers. Now, goods that are consumed by wealth producers are never wasted, for these goods sustain them in the production of goods and services. This is, however, not so with regard to non–wealth producers, who only consume and produce nothing in return.

As long as the pool of real savings is growing, various goods and services that are patronized by non–wealth producers appear to be profitable. However, once the central bank reverses its loose monetary stance, the diversion of real savings is arrested. Non–wealth producers’ demand for various goods and services is then undermined, exerting downward pressure on their prices.

The tighter monetary stance arrests the bleeding of wealth generators as it undermines bubble activities. The fall in the prices of various goods and services comes simply in response to the arrest of the impoverishment of wealth producers and hence signifies the beginning of economic healing. Obviously, to reverse the monetary stance in order to prevent a fall in prices amounts to renewing the impoverishment of wealth generators.

As a rule, what the central bank tries to stabilize is the so-called price index. The “success” of this policy however, hinges on the state of the pool of real savings. As long as the pool of real savings is expanding, the reversal of the tighter stance creates the illusion that the loose monetary policy is the right remedy. This is because the loose monetary stance, which renews the flow of real savings to non–wealth producers, props up their demand for goods and services, thereby arresting or even reversing price deflation.

Furthermore, since the pool of real savings is still growing, the pace of economic growth remains positive. Hence the mistaken belief that a loose monetary stance that reverses a fall in prices is the key in reviving economic activity.

The illusion that monetary pumping can keep the economy going is shattered once the pool of real savings begins to decline. Once this happens, the economy begins its downward plunge. The most aggressive loosening of monetary policy will not reverse it.

Moreover, the reversal of the tight monetary stance will eat further into the pool of real savings, deepening the economic slump. Even if loose monetary policies were to succeed in lifting prices and inflationary expectations, they could not revive the economy while the pool of real savings is declining.

- 1. Joseph T. Salerno, “An Austrian Taxonomy of Deflation” (paper presented at Boom, Bust, and the Future, Mises Institute, Auburn, AL, Jan. 19, 2002), p. 8.

- 2. Murray N. Rothbard, What Has Government Done to Our Money? (Auburn, AL: Ludwig von Mises Institute, 1991), p. 17.

The Mises Institute exists to promote teaching and research in the Austrian school of economics, and individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. These great thinkers developed praxeology, a deductive science of human action based on premises known with certainty to be true, and this is what we teach and advocate. Our scholarly work is founded in Misesian praxeology, and in self-conscious opposition to the mathematical modeling and hypothesis-testing that has created so much confusion in neoclassical economics. Visit https://mises.org