“Lethal For Bullion Banks” – The Looming $600 Trillion Derivatives Crisis

Authored by Alasdair Macleod via GoldMoney.com,

The powerful forces of bank credit contraction are at the heart of a rapidly evolving financial crisis in global derivatives, whose gross value is over $600 trillion; an unimaginable sum. Central banks are on course to destroy their currencies through unlimited monetary expansion, lethal for bullion banks with fractionally reserved unallocated gold accounts, while being dramatically short of Comex futures.

This article explains the dynamics behind the current crisis in precious metal derivatives, and why it is the observable part of a wider derivative catastrophe that is caught in the tension between contracting bank credit and infinite monetary inflation.

Introduction

One of the scares at the time of the Lehman crisis was that insolvent counterparties risked collapsing the whole over-the-counter derivative complex. It was for this reason that AIG, a non-bank originator of many derivative contracts, had to be bailed out by the Fed. By a mixture of good judgement and fortune a derivative crisis was averted, and by consolidating some of the outstanding positions, the gross value of OTC derivatives was subsequently reduced.

According to the Bank for International Settlements, in mid-June last year all global OTC contracts outstanding were still unimaginably large at $640 trillion, a massive sum in anyone’s book. It is unlikely to have changed much by today. But in bank balance sheets only a net figure is usually shown, and you have to search the notes to financial statements to find evidence of gross exposure. It is the gross that matters, because each contract bears counterparty risk, sometimes involving several parties, and derivative payment failures could make the payment failures now evident in disrupted industrial supply chains look like small beer.

Deutsche Bank’s 2019 balance sheet gives us an excellent example of how they are accounted for in commercial banks. It conceals derivative exposure under the headings “Trading assets” and “Trading liabilities” on the balance sheet. You have to go into the notes to discover that under Trading assets, derivative financial instruments total €80.848bn, and under Trading liabilities, derivative financial instruments total €81.910bn, a difference of €1.062bn This is relatively trivial for a bank with a balance sheet of €777bn.

But wait, there is another table that breaks derivative exposure down even further into categories, and it turns out the earlier figures are consolidated totals. The true total of OTC derivatives and exchange traded derivatives to which the bank is exposed is €37.121 trillion. That is nearly thirty-five thousand times the €1.062bn netted difference in the balance sheet. And when you bear in mind that valuing OTC derivatives is somewhat subjective, or as the cynics say, mark to myth, it invalidates the valuation exercise.

Clearly, by taking the mildest of a positive approach to derivatives held as assets, and a slightly more conservative approach to valuing derivatives on the liabilities side, that 35,000:1 leverage at the balance sheet level can make an enormous difference.

Now let us take our imagination a little further. A large number of these derivatives will have commercial entities as counterparties, businesses that have been shut down by the coronavirus since the balance sheet date. With the German economy already heading into recession before the coronavirus closed down much of the global economy, Deutsche Bank’s risk of losses arising from its derivative position could turn out to be in the trillions, not the one billion netted difference shown on the balance sheet.

Not only is there the emergence of counterparty failures to deal with, but there are ever-changing fair values, which will particularly reflect interest rate spreads increasing for Deutsche Bank’s €30.25 trillion interest rate-linked derivatives. We cannot know whether it is net positive or negative for shareholders. And with balance sheet gearing of assets 22 times larger than share capital very little change could wipe them out.

Deutsche Bank is not alone in presenting derivative risk in this manner: it is the elephant in many bank boardrooms. As a weak link, Deutsche is a relevant illustration of risks in the banking system. Since the Lehman crisis, its senior management has been on the back foot, retreating from businesses they could neither control nor understand. They have also made very public mistakes in precious metals, which is our next topic.

Gold derivatives in crisis

While a struggling bank like Deutsche provides us with a laboratory experiment for how a derivative virus can kill a bank, we are now seeing it kill off bullion banks in real time. A rising gold price, out of the control normally imposed by expandable derivatives, has effectively gone bid only in any size. We are told this is due to COVID-19 shutting mines and refineries and disrupting logistics, and so is purely temporary. The LBMA and CME which runs Comex have been issuing calming statements and even announced the introduction of a new 400-ounce gold futures contract alleged to ease the supply shortage.

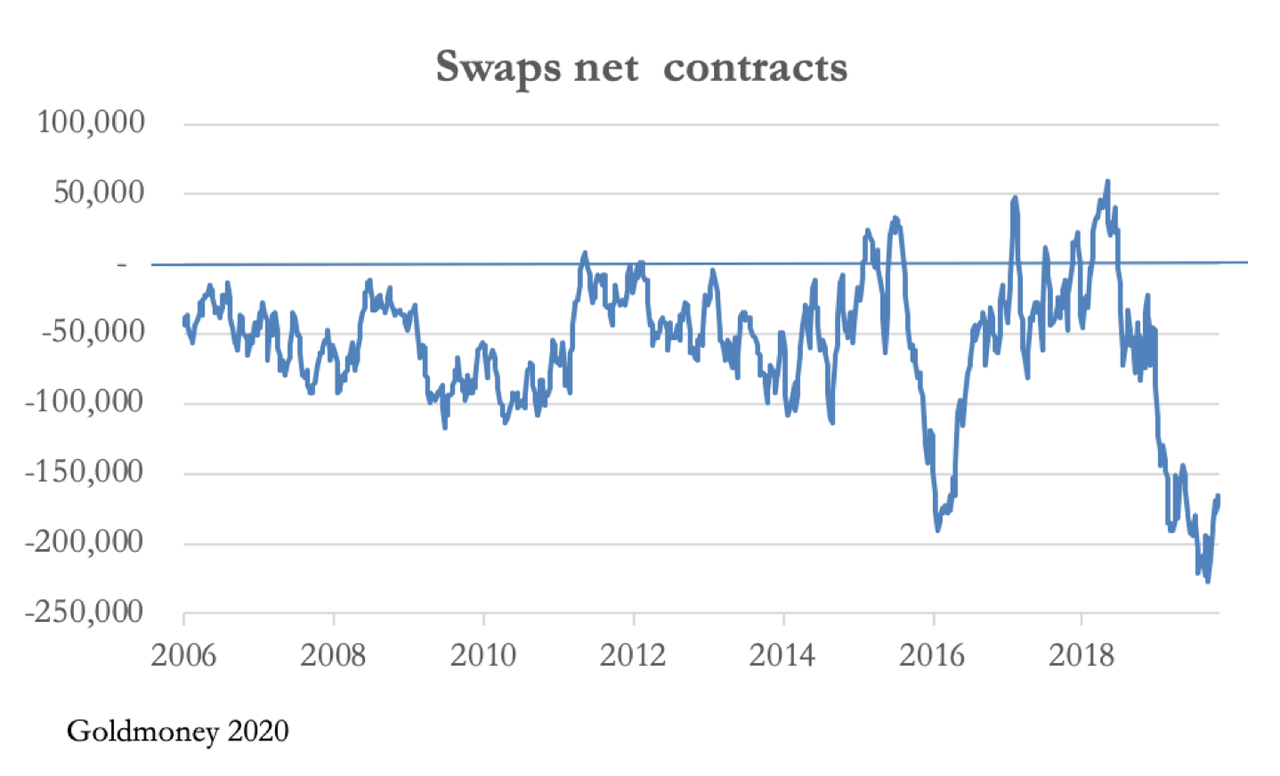

In short, the gold derivative establishment is panicking. The swaps position on Comex shows why.

With their net short position in very dangerous territory, Comex swaps are badly wrongfooted at a time when the Fed and other central banks have announced unlimited monetary inflation, signalling a paradigm shift in the relationship between sound and unsound money. For ease of reference and to understand their relevance, a swap dealer is defined by the Commodity Futures Trading Commission, which collates the figures, as follows:

An entity that deals primarily in swaps for a commodity and uses the futures markets to manage or hedge risks associated with those swap transactions. The swap dealer’s counterparties may be speculative traders, like hedge funds, or traditional commercial clients that are managing risk arising from their dealings in the physical commodity.

Therefore, a swap dealer is one that operates across derivative markets, and typically will trade in London forwards as well as on Comex. In a nutshell, it describes a bullion bank’s trading desk.

In a further piece of disinformation this week, Jeff Christian, head of CPM Group, in an obviously staged interview for MacroVoices claimed that traders in London were forced by their banks to cover trading risk in the futures market as a condition of their funding. The implication was shorts on Comex are matched to longs in London’s forward market and therefore not a problem. This may be true of an independent trader looking for arbitrage opportunities between markets but is not how it works in a bank.

The mechanics of gold derivative trading

A bank which has bullion business will almost certainly have a trading desk and be a member of the LBMA. Look at it from a banker’s point of view. The bank has business flows in gold, which requires access to the market and a dealing capability. He will employ one or more gold traders with acknowledged expertise to manage the desk. As a profit centre and because a skilled trader will require it, he will give the desk discretionary trading limits and monthly or quarterly profit targets. Part of the deal with the desk is profits will be struck net of the cost of funding the book, usually a reference to Libor, which is effectively the marginal cost to the bank of expanding its credit to back the dealers’ positions.

When the gold desk has established a profitable track record, the banker will be eager to raise the trading desk’s position limits. For bullion banking this has been going on for years, and while individual trading desks come and go, traders now have a large degree of dealing autonomy. It is not, as Mr Christian misinforms us, just a covered arbitrage business between forwards in London and futures in America.

The LBMA lists twelve market makers, all of which are well-known banks. There are thirty-one other banks, some of which run trading desks which take positions. It is worth noting that dealing in gold is normally one of many banking and trading activities undertaken by an LBMA member bank, including forex trading with which this activity is very similar. All of them are funded by the expansion of bank credit, which is the point of having a banking licence.

Turning to Comex, according to CTFC data there are a maximum of 28 swap dealers which recently have been active in gold futures, either with long or short positions. These numbers tie in nicely with the likely number of trading desks and designated market makers in the banks which are LBMA members.

An LBMA member bank will have physical bullion business and is likely to offer allocated and unallocated accounts to customers. Since the point of banking is to operate a fractional reserve-based customer service, a bullion bank discourages allocated (custodial) accounts, usually by making them an expensive way for customers to hold bullion. Unallocated accounts, which under fractional reserve banking will be a multiple of gold or gold derivatives in the possession of the bank, becomes the bank’s standard customer offering.

One of the benefits of LBMA membership is it gives a bullion bank access to paper markets, so that it can replace physical bullion held against unallocated client accounts with long positions for forward settlement, positions that can be rolled and rolled without ever having to take delivery. Another benefit is access to leased gold from central banks which store bullion in the Bank of England’s vault.

One can begin to see why dealings between LBMA members are so significant, recently hitting 60 million ounces a day, the equivalent of 1,866 tonnes. This represents dealings between LBMA members only and excludes dealings between a member and a non-member. In the distant past they were included in LBMA estimates, which inflated the numbers even further by a factor of about five times.

All this is done on minimum bullion liquidity, which when you take away central bank gold, physical ETF custodial bullion, as well as bullion owned or allocated to miscellaneous institutions, family offices and private individuals stored in London bullion vaults, is not the 8,326 tonnes claimed in a recent LBMA press release designed to calm the markets, but is almost certainly significantly less than a thousand tonnes.

Clearly, running long positions for forward settlement has become a substitute for backing unallocated accounts with a fractional amount of physical metal. While the trading books in London keep the plates spinning in their dangerously geared operation, the profit opportunities on Comex have become a separate matter instead of just a hedging facility.

Officially described as speculators, but better described as suckers, gold and silver futures are the medium for a repeating cycle whereby market makers supply them contracts by drawing on the ability of their banks to create bank credit out of thin air. Once the suckers run out of buying power, the market makers pull the rug out from under them, taking out their stop-loss points. It has been an immensely profitable exercise for swap dealers.

Fortunately for swap dealers, the suckers have short memories. Until last year, it was a frequently repeated exercise, leading to a blasé attitude. Corruption among traders had become rife and they began to be caught spoofing and rigging the fix against bank customers. Dealers were sacked, fined and jailed. Deutsche Bank were fined and forced out of the twice-daily fix. A JPMorgan trader pleaded guilty last August to manipulating the precious metals markets for nine years. Another with the same firm had pleaded guilty the previous October. In the past five years federal prosecutors have brought twelve spoofing cases against sixteen defendants, most pleading guilty.

This corruption is typical of end-of-cycle behaviour, when the derivative ringmasters in precious metals believe they have risen above the law. The point behind the current crisis unfolding in the gold derivative markets is the scam has fully run its course, and the bankers in charge of bullion desks will be increasingly concerned of the reputational damage.

How the ending of the gold derivative scam started

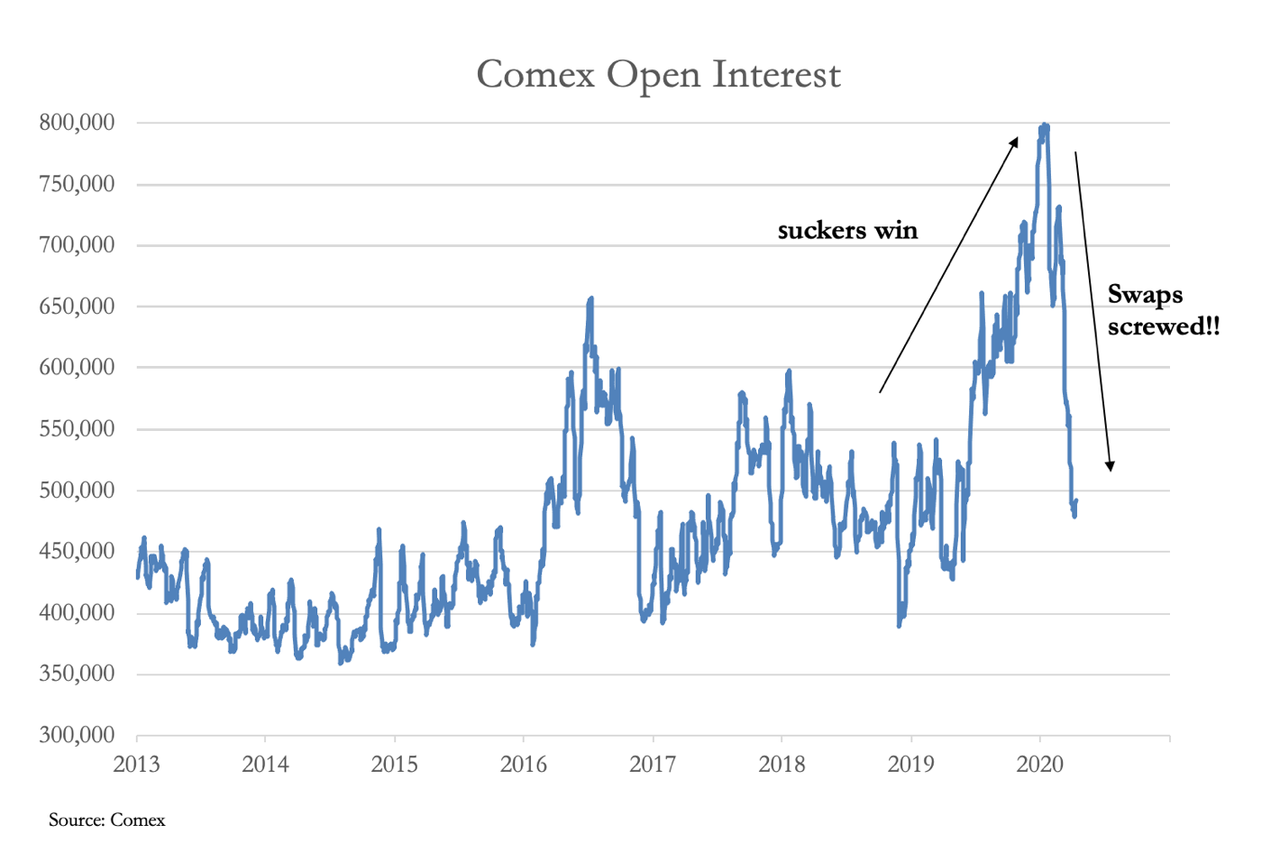

In the past, bullion banks always managed to put a lid on open interest, returning it from an overbought 600,000 contracts to under 400,000 contracts, in the process getting an even book or exceptionally going long, ready for the next pump-and-dump cycle. But then something changed. Last year, the pump-and-dump schemes of the bullion banks’ trading desks went awry, with open interest rocketing to nearly 800,000 contracts by January this year. After several failed attempts, in June 2019 gold had broken above $1350, which encouraged the speculators to chase the price up even further. The interest rate outlook then softened along with the global economy, and by early September, with open interest threatening to rise above the historically high 650,000 level, the Fed was forced to inject inflationary liquidity into the US banking system through repos. At its peak on 23 January 2020, the sum of all short positions on Comex was the equivalent of 2,488 tonnes of gold, worth $125bn. The suckers were finally breaking the banks, who held the bulk of the shorts. This can be seen in the chart below of Comex open interest:

It was imperative that the position be brought under control, and accordingly, it appears that central banks, presumably at the behest of the Bank of England, arranged for gold to be leased to the bullion banks to ease liquidity pressures. And then trading desks were hit by a perfect storm.

The coronavirus put large swathes of the global economy into lockdown, disrupting payment chains in industrial production. This meant that formerly solvent businesses now face collapse and are turning en masse to their banks for liquidity. The bankers’ natural instinct is no longer the pursuit of profit, but fear of losses, and they now have an overwhelming desire to contract outstanding bank credit. In a panic, the Fed cut the Fed funds rate to the zero bound and promised unlimited liquidity support in a desperate attempt to avoid a deflationary spiral. Meanwhile, our swaps traders in gold futures were caught record short, the worst possible position for them given the evolving situation.

The coup de grâce has now come from their banking superiors. Despite the efforts of the Fed to persuade them otherwise, bankers in their lending have become strongly risk-averse and know they will be forced to commit bank credit to failing corporations against their instincts. For this reason, they are taking every opportunity to reduce their balance sheet exposure to other activities. One of the first divisions to suffer is bound to be bullion bank desks running short positions, synthetic in London and actual on Comex, which are wholly inappropriate at a time of massive monetary inflation.

It is this last pressure that has led to an unusual combination of collapsed open interest, shown in the chart above, and rising gold prices, accompanied by a persistent premium of $40 or more over the spot price in London. Clearly, there is good reason for the LBMA and the CME to panic. If the gold price rises much further, there will be bullion desks, managing shorts on Comex and fractionally reserved positions in London, at risk of bankrupting their employers.

The Comex contract, which anchors itself to physical gold through the option of physical delivery at expiry, will face enormous challenges when the active June contract expires at the end of next month. At expiry, the speculators have a chance to obtain delivery. Normally, when the spot price is lower than the future, only the insane would insist on delivery at the higher price. But with very low availability of bullion and price premiums for delayed delivery common, London is being rapidly drained of physical liquidity as well. It is like a good old-fashioned one-two boxing combination: first the Comex market is delivered a body-blow, and then the LBMA gets an uppercut.

Many central banks who have stored their earmarked gold at the Bank of England will be unhappy as well, having leased their gold in the expectation it would stabilise the bullion market. They will not do it again for an interesting reason: gold leasing rates have turned strongly negative, with the two-month rate currently minus 3.7%. No sensible entity is going to pay a lessor to lease its gold and will want leased gold returned instead. Therefore, the availability of gold for leasing is now cut off and gold already leased will need to be returned if delivered to the lessors, or unencumbered if it remained in the Bank of England’s vaults as is the normal leasing practice.

Gold liquidity in London will then disappear entirely, at which point those with a claim to custodial gold will hope that their property rights remain protected.

Broader implications of the failure of gold derivatives

This article has gone into some detail why Comex and the LBMA face their current difficulties, and why liquidity is vanishing. For any bank with large unallocated gold liabilities, bearing in mind they are fractionally reserved mostly against derivatives instead of bullion, these problems are likely to lead to their withdrawal from the market. ABN-Amro is already reported to have closed its customers’ accounts, having forced them to sell positions, and other banks will surely follow.

The gold derivative market is probably the largest foreign exchange cross after the US dollar euro. But it is also the most fundamental of all monetary exchange markets. The relationship was famously captured in John Exter’s inverse pyramid, which showed how the world’s credit obligations were all supported on a diminishingly small apex of gold.

The liquidity pressures that result from banks trying to reduce their balance sheets also affects other derivative markets, and from our discourse on Deutsche Bank’s balance sheet, we can see that the whole banking system is in a very precarious position with respect to derivatives. While we survived the Lehman crisis with only one investment bank failing, the collapse of industrial production of goods and services due to lockdowns to control the spread of the coronavirus will almost certainly lead to multiple bank failures. Bankers are staring into an abyss.

For central banks, monetary inflation is everywhere the solution. Bank rescues, payment chain failures, the furloughing of millions of employees, helicopter money to bail out whole populations, money to bail out governments, money to support all categories of financial assets: the list is endless in scope and infinite in quantity. The survival of the global financial system is at stake. If it survives, state-issued money will have been destroyed. But then what is the point of owning financial assets valued in valueless currency?

While this process of monetary destruction would have reasonably been expected to evolve over time, the coronavirus has accelerated it. The fate of the $640 trillion derivative mountain recorded by the Bank for International Settlements is sealed and will be settled through bank bankruptcies and state-directed elimination. In observing the train wreck that is precious metal derivative markets, we are at Act 1 Scene 1 of a rapidly-evolving and dramatic derivatives tragedy.

Tyler Durden

Sat, 04/18/2020 – 07:00![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com