What’s Next For Oil As Prices Go Negative?

Authored by Nick Cunningham via OilPrice.com,

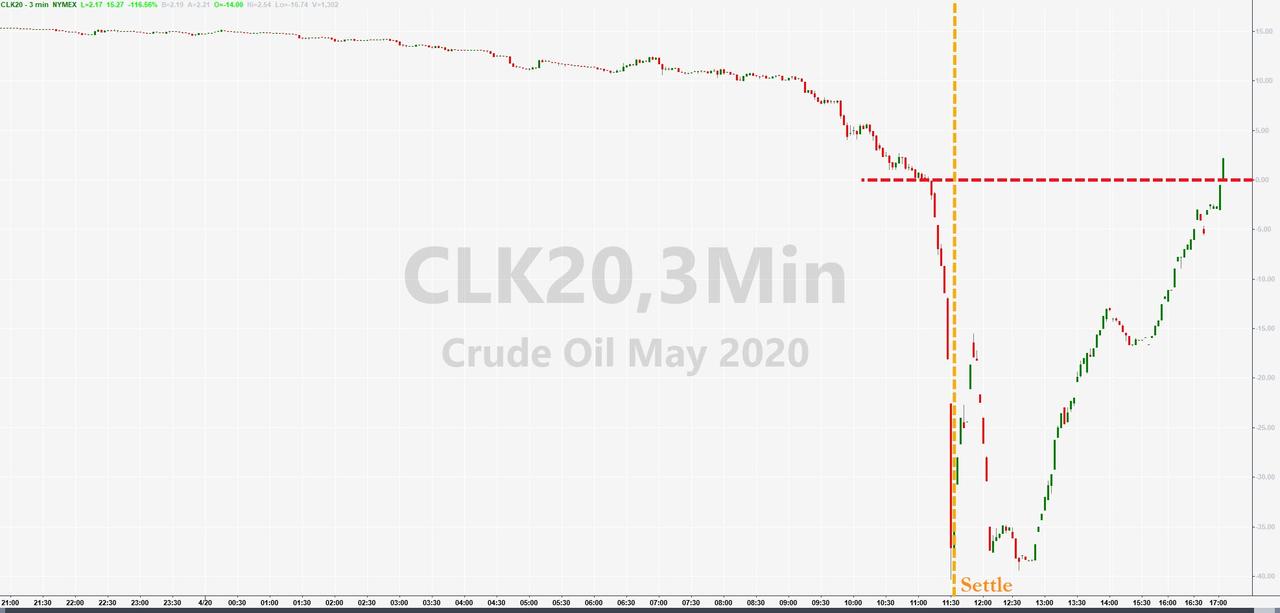

Oil prices crashed through zero, closing out the day at -$37 per barrel, an unprecedented meltdown (only to rip back to zero tonight)…

There are mitigating circumstances to these insane numbers. The prices for WTI reflect the contract for May, which expires this week. The collapse is a reflection of traders abandoning the May contract, and moving on to June. The thinly-traded May contract loses some relevance, and analysts say that the June contract – trading at $20 per barrel as of Monday – now becomes the important number to watch.

Nevertheless, it is hard to ignore the historic numbers flashing across the screen. As futures contracts expire, they tend to converge with the realities of the physical market. Prices went negative because the physical market in Oklahoma and Texas is so overwhelmed. OPEC+ did agree to historic production cuts, but not for April. In any event, the cuts pale in comparison to the decline in demand. But taken together, the effects of the price war on the supply side are colliding against the depths of demand destruction at the same time.

The result is really ugly. Nobody wants physical delivery of WTI for May, and with storage options dwindling in some places, traders liquidated their positions, selling contracts at crazy discounts. With the contract expiring on Tuesday, nobody wanted to be left holding the bag. Unable to actually accept physical delivery, traders ended up paying someone to take oil off of their hands. Surely, some fascinating reportage will be written about the last guy that got stuck with an unwanted May contract.

“The intraday WTI destruction today is certainly epic in scale, which is largely a case of jitters ahead of the WTI May 2020 futures contract expiring tomorrow and storage fears finally materializing,” Louise Dickson, Oil Market Analyst at Rystad Energy, said in a statement.

“But if you have been watching the physical spot prices in the North Sea, currently trading in the $15-18 range, this drop in WTI May 2020 futures isn’t as shocking.”

On the one hand, the negative pricing will be chalked up to a weird one-off glitch, a confluence of historic firsts due to a price war, pandemic and downward economic spiral. The bizarre development may quickly be forgotten as traders move on to the June WTI contract, which is trading at $20 per barrel. But while June doesn’t appear quite as catastrophic, oil at $20 is not a price at which most oil companies can survive for any lengthy period of time. Moreover, there is no reason to think that $20 is the floor.

The second quarter is “likely to be the most uncertain and disruptive quarter that the industry has ever seen,” Schlumberger CEO Olivier Le Peuch, said on the company’s earnings call last week.

On Monday, Halliburton also offered a grim outlook for the oil market.

“We expect activity in North America land to sharply decline during the second quarter and remain depressed through year-end, impacting all basins,” Halliburton’s Chief Executive Officer Jeff Miller said in a statement. The oilfield services giant reported a net loss of $1 billion in the first quarter.

The oil rig count dropped by another 66 last week, another steep reduction. The Permian basin lost 33 rigs. Production declines have already started, but more shut ins are necessary in the short run as spot prices come under tremendous pressure.

Ultimately, the market continues to be at the mercy of the pandemic. Several billion people are living under some version of a lockdown. The hits keep on coming. Demand for road fuels in India has plunged by 50 percent, for instance. Analysts have repeatedly revised oil forecasts, with an increasing recognition that the shock to demand will be lengthier than previously expected. In April, at least, demand will be down by 29 million barrels per day (mb/d).

Those staggering figures may not be quite as large in May and beyond, but there is little chance that global demand bounces back to 100 mb/d anytime soon, if ever.

Mark Lewis, global head of sustainability research at BNP Paribas Asset Management, argues in the FT that we may have just witnessed the permanent peak in oil demand.

Greater efficiency, more EVs and also permanent changes in behavior stemming from the pandemic could add up to a peak in consumption.

Tyler Durden

Tue, 04/21/2020 – 07:00![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com