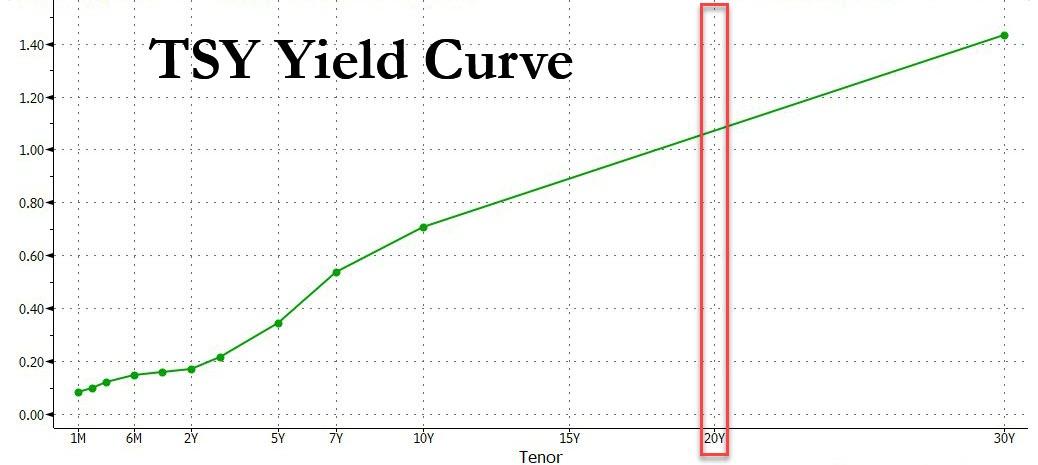

Roaring Twenties: What To Expect From Today’s 20Y Auction

Tyler Durden

Wed, 05/20/2020 – 09:40

Today, May the 20th, marks the first auction of 20-Year Treasury bonds since 1986 with an inaugural auction size of $20 billion, and with the When Issued trading at 1.23%, there is a non-trivial chance the auction will price at 1.20%!

The auction will be closely followed with investors (and the Treasury Department) attempting to judge the degree of demand for duration in the sector. It will also be closely watched by the Fed, because as Bloomberg points out, the central bank already owns more than 70% of the two CUSIPs closest in maturity to the new 20-year.

“The Fed can purchase up to 70% of the outstanding amount of an issue, and has done so with all but two of the bonds closest in maturity to the new 20-year”

via @beth_stanton more @TheTerminal pic.twitter.com/yrqyRpa1vL

— Jonathan Ferro (@FerroTV) May 20, 2020

https://platform.twitter.com/widgets.js

As BMO rates strategists Ian Lyngen and Jon Hill write, it’s likely to provide CTDs for the classic bond contract, therefore the perception is there will be a base of natural buyers. One might assume this factored into the initial size of $20 bn – above the estimates of many. An auction concession of some sort is warranted; although BMO anticipates the new issue will be well absorbed even if it comes at a modest discount. After all, there is no such thing as a bad bond; just a bad price. As such “aside from the reestablishment of a benchmark on the yield curve, today’s session offers very little to trigger a collective rethink of investors’ current interpretation of the macro landscape.”

The main event of the session and arguably week will be the first 20-year Treasury auction since 1986. There is ample reason to expect the inaugural offering will be met by a solid primary market bid. If the sponsorship to last week’s 10- and 30-years were any indication, despite the record large auction sizes and yields within striking distance of all-time lows there is still strong demand for dollar duration. Indeed, the largest stop through at a 10-year auction since March 2017 and a modest tail despite coming at the yield lows of the day for 30s hints of a long-end investor base that is eager to take advantage of the liquidity point supply provides. Especially as the 20-year sector of the curve becomes more established, it is not unreasonable to anticipate an incremental yield pick up in the early days of the new bond as a concession for what will initially be a comparably thinner volume profile.

In terms of valuation, the fact that we have seen 20s cheapen significantly on an interpolated 10s/20s/30s butterfly also bodes well for the takedown. To say nothing of the concession over the past several sessions as 10- and 30-year yields drift toward the top of their respective ranges while the curve steepens. Additionally encouraging is the return of favorable currency-hedged Treasury yields for Japanese investors, which should entice buying interest from an investor base who historically has been active in the long-end of the curve. While month-end is approaching, the fact that 20s will not settle until the calendar flips removes any rebalancing bid that will benefit the new bond at future auctions. All in all, we will look for a solid initial auction and expect a stop near 1pm WI levels.

And some more observations from the BMO rates strategists:

While equity futures suggest stocks are poised to open back near the post-crash highs, the initial euphoria surrounding a Covid-19 vaccine has quickly faded. Progress toward the slow and steady reopening of the global economy continues and results in Europe are encouraging; even if the lack of a resurgence thus far doesn’t imply the pandemic is behind us. In fact, given that the US has been lagging the Continent there is little doubt the coronavirus will remain top of mind for the balance of 2020. This backdrop leaves our range-trading thesis solidly intact as the lower and upper-bounds in 10-year yields that have been in place since late-March continue to hold.

In fact, the more habituated investors become to having 10s in the 54 bp to 78 bp zone, the greater the difficulty in anticipating a breakout. Sure, eventually the extremes will be challenged; rates will go up and rates will go down, just not necessarily in that order. Nonetheless, it will take a paradigm shift in the economic outlook to inspire a truly sustainable repricing. In part, this has driven our interest in determining exactly what the ‘consensus’ for the timing and pace of the recovery is at the moment. Setting aside the V, W, L, U, Swoosh name-calling, investors are resigned to a very deep recession which is followed by a difficult road to recovery. This isn’t new information per se, but as the market discourse on the timing of the rebound has slowly transitioned from months, to quarters and eventually settled on years – we’ll admit some surprise that neither the range in US rates has broken nor has the bullish trend in equities faltered.

The rise of zombie companies in the wake of the lockdowns represents another concern as the post-pandemic reality slowly takes shape. Firms which remain in existence, but only a shell of their pre-crisis business model intuitively need fewer employees and while government assistance has attempted to provide a bridge to make it through the lockdown, the risk has quickly become what companies will find on the other side. The secondary fallout for the labor market remains to be seen, even if expectations are for an elevated unemployment rate as the nation gets back to work. This will continue to edge wages lower and risks a durable period of disinflationary pressures. The Fed has taken dramatic steps to offset the acute downsides from the pandemic, though the longer the shutdowns linger, the more permanent much of the economic damage becomes.

Given all of the above is fairly consensus, anything which materially challenges this base case scenario will lead to an attempt at a repricing. Yesterday’s vaccine-inspired equity rally offers a prime example as such a decisive tool in combating Covid-19 would meaningfully shorten the path to recovery. Beyond greater success in slowing the progression of the coronavirus or limiting its impact, the incremental stimulus efforts on the part of the government and central banks will only serve to reinforce the lengthening timeline before the economy settles into a durable new normal. For the time being, the session ahead offers little to inspire revising investors’ core assumptions and as a result, the trading range is safe for the foreseeable future.

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com