Transformational Markets: History Being Made

No-Bond World And The Risk Of A Daily Liquidity Crisis

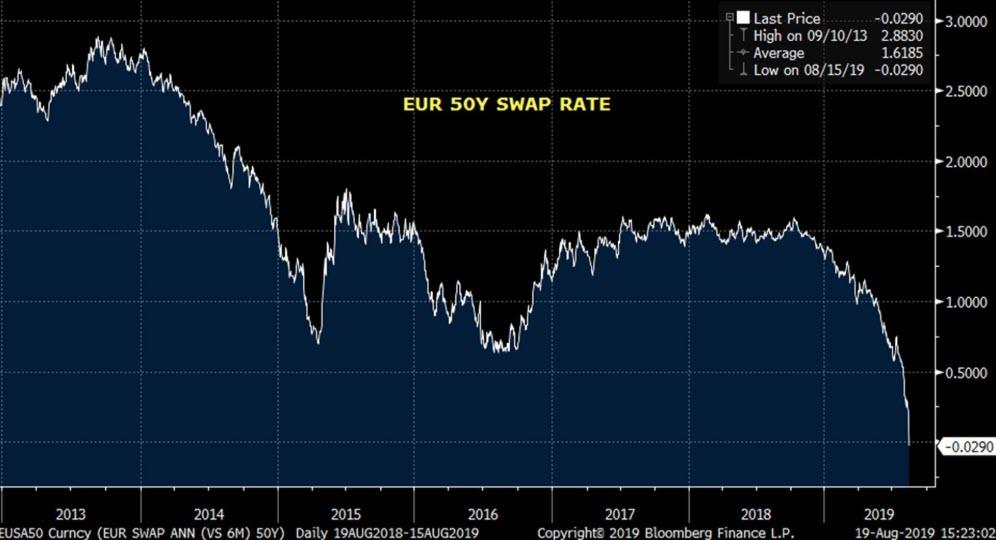

Rates hit new lows this month. Symbolically, the 50-year swap rate in Europe dived into negative territory. Bonds as an asset class are in extinction, a major shift in modern finance as we know it, inadvertently turning ‘balanced portfolios’ into ‘long-equity portfolios’. The ‘nocebo effect’ of enduring negative interest rates is such that negative rates are deflationary, hence self-defeating. Meanwhile, they have potent unintended consequences for systemic risk, which spreads around, leading the market into an historical trap. A ‘Daily Liquidity Crisis’ may result. All the while as markets get off the sugar rush of Trump rate cuts, and Europe has his banking sector at risk of implosion.

History Being Made

It must be a great thing to witness history being made during the span of your career, to find yourself in a market where so much happens for the first time in the history of finance, and close to everything else is at an extreme over the past decade. Nothing much is left around us which is trading regularly, or around historical averages.

In no particular order: the whole of the US interest rate curve dropped below 2% in mid-August, for the first time in history. The whole of the German interest rate curve dropped below zero. The Swiss, Swedish, Japanese curves are also negative for their entirety or whereabouts. The 10yr Swiss government bond yields a mind-blowing -1.2%, a sure bet to make no less than 12% in capital losses by maturity. Peripheral Europe joined in: the 10yr Portugal government bond is close to 0% yield now, about to dive in negative land too.

Across Europe, the EUR 50yr swap rate dipped below zero for the first time ever this month.

Approx 20 junk bonds in Europe trade today at negative yields, including Altice, Nokia, Arena.

Mortgage bonds are trading negative in Denmark (10yr maturities) and Germany (5yr maturities). For the first time ever, the third largest bank in Denmark offered mortgages at -0.5%. For the first time in its history, UBS will charge the super-rich for cash deposits. For the first time in humankind, a supposedly dull invested in a AA-rated Government bond returned 80% in 8 months in price appreciation, 100% in ca. 2 years: the Austria 100yr 2.1% coupon bond, now yielding a generous +0.70%, for a prime government bond that raced faster than a penny stock at the IPO. And then, of course, for the first time in history, over ca. $16.4 trillions worth of bonds globally are trading at negative yields, approx. a third of all govies globally. We thought we had seen the bottom in yields in 2016, having recorded the lowest yields in 5,000 years, only for the record to be broken again in 2019!

In equity-land too, outliers abound. Argentina’s MerVal Index dropped 37.9% in one day on August 13th, the largest daily collapse on record, a 15-sigma event, the odds of which are truly infinitesimal; meanwhile, their bonds recorded a 4-sigma event. European banks made new historical lows, exceeding the post-Lehman mayhem; and even flirting with the lows of the mid-80s, some 35 years ago. With less than Eur 20bn, today you can buy the two largest German banks, Deutsche Bank and Commerzbank. The total market cap of the 26 largest banks in Europe is below Facebook’s. And is set to continue shrinking, as rates move lower across maturities.

In currency-land, absent dramatic action from the FED, the US Dollar seems about to break decade-long resistance lines against the world, both developed and developing. The Asian Dollar Index (ADXY) for example, measuring Dollar strength against select Asian currencies, is flirting with a long-running support, and threatens to break with vengeance. Its main constituent (for 41.2%) is the Chinese Renminbi, that crossed 7 against the Dollar for the first time in a decade, as trade tensions flare up and is used as a negotiation tool.

For the future, breaking Guinness records feeds onto more record breakings. As investors in the Austria long-bond doubled up capital in 2 years (that is, before leverage), and investors in 10yr Bund are up 12% year-to-date (before leverage), you may expect the fast gains to attract new speculative demand, and rates to go even lower. If 10yr Swiss is already at negative 1.20% yield, why shouldn’t Bunds be there? With PMI in Germany showcasing an astonishing free fall back to 2012 EU-crisis levels, a handy narrative is there to justify that that’s where they belong, in deep antimatter territory. New lows are baked in the cake.

Negative Rates Are No Natural Law

Deeply negative interest rates are the biggest elephant in the room, evidently. But instead of raising eyebrows and make heads explode, they now seem broadly accepted by market participants and policymakers, having become a sort of natural law in modern-day finance. Forgetting that rates are already negative, the ECB contemplates new cuts; the IMF agrees. By habituation, we got so used to them that they became part of the furniture, boring and dismissed as a sort of déjà vu’. They must be accepted by the world of finance as a fact of life, and all better adapt to them at the margin.

In contrast, lasting negative rates should be seen for what they are, the magic and poisonous blood-red wishing apple, sending Snow White into deep sleep. Markets become ‘Fake Markets’, where valuations are nobody’s problem, and the structure of the market itself morphs in response, to become undiversified, passive, price- and risk-insensitive, abnormally sluggish, half asleep. In induced lethargy.

As investors’ minds hibernate, the market discourse dropped to new lows alongside interest rates, and is nowadays incessantly obsessing on secondary-order elements: the shape of the curve, trade tensions, the independence of the FED, indications from sector rotations, the VIX. For instance, the curve. The US curve has turned negative this month, for the first time in a decade, which has historically correlated well to upcoming recession and steep market declines. Yet, rates have never been this negative before globally, so how can the comparison be equally informative today? If rates are negative, for long enough, all around the globe, shouldn’t curves get flat or negative, eventually, naturally? As we long argued in previous write-ups, negative rates are deflationary and work as a magnet. Rates have been negative despite fluctuations in inflation and growth rates over several years now, which signalled to market participants that price discovery is impaired and perhaps bonds as a financial instrument are dying. It is hard to overstate the historical juncture we are at.

Nowadays, victims of a magic spell, most market participants think it is OK for a bond to yield negatively. In behavioural finance, the spell can be broken down in the ‘ostrich effect’ and the ‘anchor bias’: the mental hack that allows us to ignore the bigger picture and focus on a single element that worked well for us in the recent past, thus sticking the head in the sand to protect against warning signals.

However, there is a simple difference between a coupon-bearing bond and a negative-yielding bond. The difference is that one is a bond, while the other one is not. It is something not seen before in financial history, at this order of magnitude and duration at least, something that needs a new name but surely is no longer a bond. Perhaps, an anti-bond, or a fake-bond, or fake-cash; but surely not a bond. Traditionally, a bond instrument differentiates from an equity instrument in having a capped upside, a recurrent income called the yield, stability and security over cash flows. Negative yielding assets (or shall we say liabilities) have a sure downside, as they guarantee a loss of capital, except it is not capped as it could always be larger upon a credit event.

Much of the literacy and the modelling in finance, over history, assumes rates to be floored at zero. None of the founding fathers of economics and finance had to deal with this shape and form of ‘market economy’. It follows that we cannot reach out easily and comfortably to the work of Keynes, Smith, Cantillon, Galbraith, Friedman, nor to the pricing tools of Cox, Ingersoll, Ross, Black, Scholes, Hull, etc.. for guidance. What’s the value in modelling the term structure of interest rates today? Similarly, portfolio management tools like Capital Asset Pricing Model (CAPM), Modern Portfolio Theory (MPT), Value At Risk (VAR), Risk Parity are all ill-equipped to handle a world of lasting negative interest rates.

That leaves us, nowadays, in the middle of the ocean during a storm with no compass to help navigation.

Not even the visionary economist and monetary reformer John Law, founder of the first Central Bank in France in 1716, could ever have imagined the alchemy of finance of negative rates. A bold gambler by background, he saved the country from bankruptcy by introducing ‘paper money’ and banknotes. Well before Keynes and modern economics, he believed that the intrepid expansion of unbacked printed money in circulation could spearhead the economy back into life and create the inflation needed to pay offs debt. Yet, he too worked under the constraint that savers had to be paid something to lend to bankrupt borrowers. Today’s central bankers are bolder risk takers than their godfather John Law, it seems, willing to take more chances than the revolutionary gambler. For the records, John Law’s monetary experiment peaked in the historical Mississippi Bubble.

In such unchartered territory as the one we live within, where financial laws are lab tested on a grand scale and the traditional economics of saving and borrowing are flipped on their heads, the belief that the shape of the curve of interest rates, or the gold/Treasury ratio, or credit/equity correlations, or generic trend-lines, or the VIX/VXX, or Hindenburg Omen .. will help us assess the probability of what’s to come probably sits in between wishful thinking and a fairy tale. New tools are needed, to understand the secular, critical transition we are in. In our efforts over recent years, we devoted our attention to Complexity Theory, to try and add some value to the discourse. To a bare minimum, such theory bothers about non-linear connections, runaway effects, positive feedback loops, far-from-equilibrium dynamics, all so visible in today’s environment. It may well be a wrong or insufficient venture, but surely the interest rate curve is less informative. You can’t fight modern warfare with arrows and catapults.

Happy Ending

By the way, if negative rates are indeed the red apple of the fairy tale of Snow White, we should all fasten seat belts. In the original story by the Grimm brothers, differently than in the Disney movie and others, Snow White was not cured by being kissed; the Prince was amazed at her beauty and had her carried in the glass coffin to his castle; while on route to his kingdom, she was knocked, the coffin shook open and Snow White vomited up the apple. So, it was not a romantic kiss of love to save her, as most believe, but rather a road accident. It was a good crash, that awakened our heroine. Informative.

Bonds: To Be Or Not To Be

No-Bond world. Bonds as an asset class are in an existential crisis. But, if bonds are not bonds, it also means that a lot of ‘balanced portfolios’ out there – incidentally representing the bulk of asset allocation globally – are no longer ‘balanced portfolios’, but rather ‘long-only equity portfolios’, with some ‘cash’ to the side. Except the ‘cash’ is fake-cash, insofar as it can lose money too, and is likely to do so at some point down the road upon resurgence of inflation, default risk or confidence crisis. This is one big unintended consequence of negative rates for global asset allocation and the institutionalized Asset Management industry as we know it. Reluctantly when not unawarely, a lot of institutional investors the world over, mandated with low volatility safe allocation targets and typically expressing it through mostly fixed-income portfolios, find themselves instead to be ‘long only equity’ managers, de facto.

To an extreme, if bonds are retiring as an asset class, we are looking at a totally different market economy than the one we have been accustomed to, a new monetary paradigm, a major historical shift. Which then, again, also means that discussing the shape of the curve, or the FED, or trade wars is petty talking. A bit like having the Incredible Hulk entering the room and joining the meeting, and spending all the time discussing his hair style.

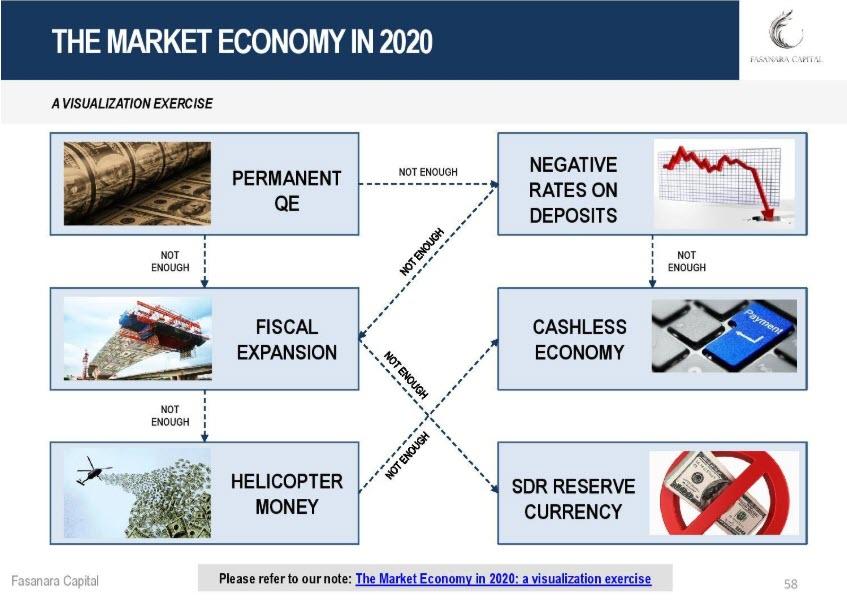

Deep and persisting negative rates are not a surprise after all. In our 2016 piece titled ‘‘The Market Economy in 2020: a visualization exercise. The Emergence of a New Monetary Orthodoxy’’ (link), we discussed how the market may have looked like this time next year, and negative rates ranked top of the list, in recognition of the historical transition we are witnessing in years such as these.

Still, to think that they do not have negative systemic consequences is a costly miscalculation. We think they do, and no need to wait because the process is already unfolding. The longer it goes the more brutal the pull-back, and the more Biblical-type the day of acknowledgement will be.

Source: Fasanara Capital | SCENARIOS, 7th June 2016

The Market Economy in 2020: a visualization exercise. The Emergence of a New Monetary Orthodoxy (link)

‘’It is not the first time in history that we go through an existential crisis of global capitalism. In the 20’s, structural deflation led to Keynes revolution in economics. In the 70’s, chronic inflation led to Milton Friedman counter-revolution, and governments like Thatcher or Reagan. Market-based economies survived both. Today, a new form of global capitalism might have to be worked out, after we decipher how we could still be entangled in deflation despite what we learned from past experiences. We thought we knew it all and we do not. The disruption from technology, working wonders at accelerating returns, is happening so fast that it is tough to come to terms with it and fully grasp its many implications. For what is worth, also the industrial revolution took years to equate to growing productivity and wealth, while it went through its implementation phase. Industrial and aggregate productivity growth slowed down markedly in the years 1890 to 1913, as we moved towards the second industrial revolution (‘electric dynamos were to be seen everywhere but in the productivity statistics’: the modern productivity paradox, the case of the dynamo. Also interesting in this respect the ‘regime transition thesis’ of Freeman/Perez).’’ .. ‘’A new evolutionary phase of combining QE, deficit spending, and ‘helicopter money’ – the nuclear fusion of monetary and fiscal policies – might well be the next stop for policymakers, as they move from price setting to direct resource allocation, in certain markets more than others, in certain places sooner than in others, but the road to that next stage is certain to be bumpy. Policy mistakes and market accidents are legitimate along the way.’’

The Ugly Face Of Enduring Negative Rates: System Stability

The centrally-induced gravitational forces of endless negative yields across vast swathes of the bond universe are winning over market forces. The transformation of the market economy is progressing and central planners are winning, eating out market pricing mechanisms all across.

But there is a flip side, and frightful unintended consequences.

First, the ‘nocebo effect’ of negative interest rates. In medicine, the nocebo effect is opposite to a ‘placebo effect’, insomuch that it depicts the phenomenon in which inert substances or mere suggestions of substances actually bring about negative effects in a patient. As a market participant, if I know that lending does not yield much, but may entail untraditional levels of risks, I do not lend. I wait and see what happens first. As a borrower, if I feel the economy is so desperate as to be in need of endless non-sensical negative rates, I do not borrow. What are the prospects in an economy in need of dramatic measures. Having flipped completely upside down the lending and borrowing scheme, by messing around with the price of money, creates a market economy that leaves economic agents wandering and waiting on the side-lines. They go to sleep, like Snow White after biting the red apple.

In that, enduring negative rates are deflationary. Thus, in a vicious cycle, defeating the purpose for which they are introduced.

But it is not only a phenomenon of inert substances influencing agents in the economy. It gets quite mechanical. First, as a Central Banker, if I see my fellow bankers indulging in negative rates I may be compelled to follow suit, to not lose in competitive devaluations and currency wars. This is especially the case at those times when geopolitical risks are on the rise.

Then, the involuntary effect on the market structure. The Negative Interest Rate Policy, when combined with Quantitative Easing, has all sorts of amplifying feedback loops with the private investment community. It created today’s undiversified modern financial markets: a homogeneous, over-concentrated, systemically unstable investment community. A number of investment strategies that are diverse only in the labelling/marketing, but do the same job. Two factors explain it all: long Beta/ Carry (or what’s left of Carry at zero rates) and short Volatility. It can be called Risk Parity, Risk Premia, trend-chasing momentum or CTA, low vol ETF or long-short Equity, but is indeed limited to the jolt of those two factors for the most part. This follows logic. If those two factors are all that works, those two factors must disseminate across, percolating down the veins of the financial system like an addictive drug. And so it happened that on repeated use, after use, after use.

The first serious bear market may prove it, and expose the un-diversification of the market community for what it is. Until then, in the absence of feedback mechanisms to realign exposure, the problem cannot but compound further. The longer it compounds for, the more violent the adjustment down the road: a law of mathematics that negative rates cannot replace.

Additionally, zero and negative rates have accelerated the rise of passive strategies and ETFs. As an equity investor, looking at an environment of negative rates globally and knowing something is wrong, I should step to the side, prudently. This should curb equity excesses, and meanwhile keep the S&P below 2000. But such informed investor is no longer there: it is a renowned fact that between 70% and 90% flows daily (depending on the source being BAML, MS or Vanguard) on the S&P are passive. Passive vehicles have no need to overanalyse assets before buying. The long list of pricing anomalies across ETFs proves it rather conclusively.

Meanwhile in the real economy, again mechanically, if insanity prevails and as a junk borrower I can raise cash at negative rates, of course I will, to leverage up and buy back my stock, thus boosting the equity price to unnatural levels. Today’s, Nokia, Altice and many others can decide to do so, in simple math. Soon enough, we are likely to see attempts at raising ultra long-dated junk bonds for a bunch of basis points in annual coupons in return: a bulky yield pick up.

Because of mechanical effects and nocebo effects, the original sin of negative rates and heavy market manipulation led to the ‘fake markets’ we line in today, insensitive to fundamentals, dominated by passive vehicles, fraught with systemic risk.

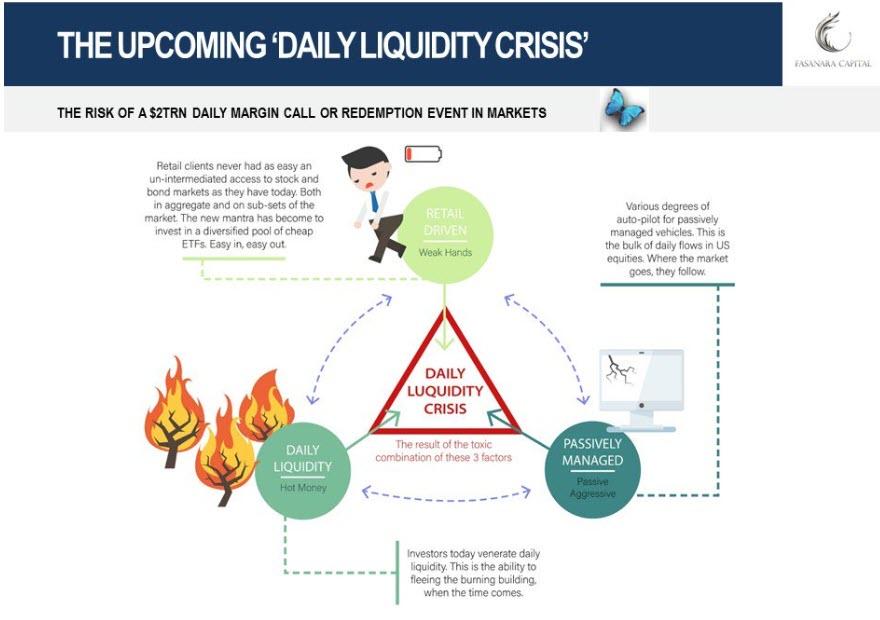

Systemic Risks: The Upcoming ‘Daily Liquidity Crisis’

Equities, especially US equities but also European, are in a state of illusory stability, while clouds gathers at the horizon in the months ahead.Underpinning equity strength are 16.4trn of negative yielding non-bonds. Markets today are propped up by the wrong expectations of further stimulus and a peaceful resolution to the trade spat. Both are likely going to be proven ill assumptions, ultimately. Meanwhile, liquidity in the market is ephemeral across bonds and equities and ready to evaporate: a liquidity crisis lurks ahead.

Systemic risk incubated in the structure of the market over recent years.

In heavily-manipulated markets such as these, three key factors emerged and are dangerously interacting today:

-

Daily liquidity vehicles, be it ETFs or several other formats in major economies, have never been as dominant as they are today.

supposedly-active-but-turned-passive. -

Passive auto-pilot vehicles, either in the form of fully-quant funds, systematic, quantamental, CTA or supposedly-active-but-turned have never been as large a share of the total as they are today.

-

Fickle retail investors never had as easy a direct access to markets as they have today through ETFs of the most disparate natures, often overselling liquidity (way above that of their underlyings) and diversification (often a fraction of what is portrayed).

Unlocked hot money, retail driven, passively managed: the daily liquidity risk is highly underestimated today. With it, the so-called ‘gap risk’, especially overnight gap risk. Which bring us to the real danger in markets these days being the market itself, which may implode under its own weight at a moment’s notice.

Liquidity, defined as the ability to get out of positions at times of market stress, is nowadays overestimated by the proliferation of passive vehicles and daily liquidity vehicles. Now more than at any point in the past decade, investors have the ability to fire-sell positions on any given day for full amounts. If a large-enough shock event takes place, the market system may find it hard to absorb selling flows, therefore leading to a snowball effect of more selling flows and large downside gap risks.

The risk of a $2trn daily margin call or redemption event in markets is no longer a theoretical exercise, it is indeed nowadays workable assumption.When the top three US asset managers alone command a staggering $14trn of AuM, for the most part retail/daily/passive, the issue should be on every market regulator/participant table, and is not. Against that, there is no FED, ECB nor BoJ put together. A massive move overnight is then made entirely possible, by undiversified retail passive daily money.

Our blueprint for the next crisis is not 1987, 2000 nor 2008. But rather the ‘Quant Quake’ of August 2007. Also referred to as the ‘August factor’. At that time, renowned quant funds, including the famed Goldman Sachs QIS fund, lost 30% in short order: without any apparent reason – which itself tells a lot about market brittleness. Except this time around it may be 10-fold worse, insofar as it would not be isolated to quant funds but rather sprawling across fast through the undiversified passive expensive financial network.

Trash Ratios Have Never Been Trashier

Daily liquidity, passively-managed and retail-driven. Liquidity gaps have enough to work with. But this is not all. The daily liquidity is an obsession for investors in Europe, representing the vast majority of investment strategies in the continent these days. In a zero-yield world, managers have wanted to include in their portfolios as much illiquidity premium as possible, by investing into near-unsellable securities up to the statutory limits of their funds. For UCITS funds, the common vehicles for daily liquidity in Europe, that limit was the 10% Trash Ratio. The recent cases of Woodford, H2O, GAM – where illiquid pockets were found in supposedly liquid portfolios and caught the market by surprise – depict a trend which is widespread across the industry, and measures the desperation for performance (and survival) of asset managers after 10 years of yield repression.

This can be expected. It is a logical consequence of the persisting zero-yield environment.

Mark Carney, Governor at the Bank of England, referred to the issue of liquidity mismatches as follows: “This is a big deal. You can see something that could be systemic. These funds are built on a lie, which is that you can have daily liquidity for assets that fundamentally aren’t liquid. And that leads to an expectation of individuals that it’s not that different to having money in a bank,”.

Trash ratios are not alone in housing illiquidity risks across UCITS funds. Other sources of illiquidity include:

-

Overlay derivatives, where managers sell volatility to enhance performance and revive carry, on both Equity (sell puts or calls to take in premium upfront, reverse convertibles / autocallables), Credit (sell swaptions on rates, sell credit spread options, sell CDS or other unfunded instruments), Currency, or combinations (exotic options)

-

Those ETFs – and other daily liquidity vehicles – where liquidity and diversification are overstated, at the source: theoretically sellable on a daily basis but, in reality, liquidity will evaporate when is most needed on steep market downturns – illusory liquidity

Back To Square One, After Trump Sugar Rush Digression

When was the last time that we had rates moving to negative territory en mass, the US Dollar was feared to appreciate wildly, the Renminbi to break into new lows and create havoc, PMIs tumbling? At the end of 2015.

In between now and then, stands globally-coordinated monetary intervention and then, in late 2016, the preparatory work that would lead to the ‘’Trump fiscal sugar rush’’ of massive tax cuts.

If monetary intervention worked wonders at the time, we can expect a lower marginal effectiveness today, as most ammo have been spent, and global Central Bank coordination itself is more arduous today on account of trade tensions and political interference.

If the market is a bubble now, it was a bubble a year or two ago too, one which got blown some more by monetary and fiscal steroids. The can was kicked down the road at great cost.

The Next Jolt in Europe: Banks

Abstracting from a changing market structure and secular trends, and going back to traditional market analysis for a moment, the most imminent issue the market will have to deal with in H2 2019 seems to be in Europe, even before trade wars.

Europe is going through a rough patch, and this is no news. As we argued most recently in January, European Parliament Elections were a criticalevent, well-beyond an over-hyped Brexit topic. The event did not turn out for the best, as populist parties advanced further, inarguably, and a lack of vision for the long-term was still evident. Meanwhile, the political environment in Italy complicated further, with the government disaggregating and new elections in sight. With deep and enduring negative rates, European banks are in a dire situation to say the least. Recent new multi-decade lows of the banking sector are inevitably the variable to watch from here. The ECB will try to buy more time with new monetary stimulus, and Germany will introduce some form of fiscal stimulus (finally). We will need to see the actual policies that will be introduced, before assessing. In general, though, despite such temporary measures in extra time, structural issues do persist, and market forces may at some point prevail. The monetary intervention is marginally ineffective, whatever the size, and fraught with more collateral damage on the banking sector itself. A yield curve control measure is likely to be introduced, to peg long-end yields from imploding further (Germany) or rise uncontrollably (Italy). Incidentally, a stronger Dollar in the process, on a weaker EUR, cannot help risk assets globally either, at a time when the Dollar is strong and threatens to break long-range trend-lines against most of the world currencies.

New Problems New Tools

The reason for our disaffection with traditional market analysis is that it seems impotent to help navigate the historical tectonic shifts we have in front of us.

At a time when traditional market analysis is less helpful than usual to assess the probability and vicinity of a major adjustment from bubble conditions for financial markets, and isolate the critical threshold beyond which events gather momentum and speed, the science of Complexity can instead help shed some light. Differently than in finance, it is often used in other complex dynamic systems, sush as ecosystems, societies, climate, oceans, brain, human immune system etc to help analyse the dynamics of criticality close to tipping points.

A number of factors seem to suggest that we are approaching the tipping point in markets. The early warning signals that we analysed in previous write-ups are enumerated in the Table below.

In recent times, we also spent time working on modelling and visualising the fragility of the market structure (Cascade Effects In Modern Undiversified Passive Markets and Analysis of Market Structure: Towards A Low-Diversity Trap), in addition to deriving system-level indicators of market fragility (How To Measure The Proximity To A Market Crash: Introducing System Resilience Indicators ‘SRI’).

While inconclusive, such tools help describe system degradation in recent years and today concur in framing systemic risk at high alert status, current market conditions as profoundly fragile, and in proximity to a major shift, a system-wide critical transition.

Source: FASANARA CAPITAL | PRESENTATION, 11th May 2018

Market Fragility (Part II): Tipping Points & Crash Hallmarks

Presentation and Video Recording, on Markets as Complex Dynamic Systems and a conceptual framework for rethinking Systemic Risk as a Complexity Problem, in 3 steps: Tipping Point Analysis, Early Warning Signals Analysis, Butterflies Analysis. link.

‘’So then, let us not be like others, who are asleep, but let us be awake and sober.’’

First Thessalonians 5:6

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com