Authored by Sven Henrich via NorthmanTrader.com,

Markets blow up on Friday on a series of tweets, markets jam higher on the pronouncement of dubious phone calls on Monday. The rapid back and forth has many heads spinning and makes for dramatic headlines as people are searching for explanations. To which I say: Keep it simple, especially in the age of the great confusion.

Background: In 2019 market gains have been driven by pure multiple expansion resting on 2 pillars of support in the face of deteriorating fundamentals: 1. Hope for rate cuts and Fed efficacy 2. Trade optimism. But in process little to no gains are notable since the January 2018 highs, in fact most indexes are down sizably since then.

And when markets are purely reliant on multiple expansion the risk for accidents increases when confidence gets shaken. Friday’s escalation on the trade war front again highlights this point.

And in context of global growth slowing an escalation in the trade war is akin to playing with fire as it risks being a trigger to nudge the world economy into a global recession. After all 9 economies are either in recession or on the verge of going into recession.

This morning I was speaking with Brian Sullivan and he asked me what matters most here, the China trade war, the Fed, or technicals. The short answer is they all matter as it is a battle for control, but how to delineate a complex interplay of conflicting forces into some clarity?

Let me give you my take on all 3 fronts. Before I do, for background here’s the clip from this morning:

[youtube https://www.youtube.com/watch?v=nET_UZc3nSU]

China:

Occam’s Razor: The simplest explanation is often the best one and that’s really what’s happening on the China trade war front as far as I’m concerned. The Chinese sensed weakness when Trump delayed the very tariffs he announced in early August and the ‘tariffs delayed’ newsflash came on the heels of markets selling off and it produced a relief rally of size. The Chinese realized Trump’s vulnerability (the US consumer) and wanted to test him. And they did on Friday by retaliating with tariffs on their own. And if you believe the Chinese propaganda their counter punch announcement was specifically aimed at hurting the US stock market. And Trump predictably reacted with rage and emotion and ended up doing more damage than the Chinese by counter punching immediately on twitter. The impression: A decision made out of anger not prudent strategy.

So what happened? Markets tanked hard again and when the damage became apparent in Sunday overnight futures trading a narrative, true or not, was created to bring markets back up. The signal was clear and hence the rally today:

Markets don’t care whether Trump tells the truth or not.

They care that he freaks out when markets drop and immediately backpedals.

Once a poker player reveals his tell he’ll get called again and again and again.— Sven Henrich (@NorthmanTrader) August 26, 2019

https://platform.twitter.com/widgets.js

If the world was wondering how far Trump is willing to go on the trade war front the Chinese got their answer twice in August: $SPX 2800.

After all it’s his stock market alone:

My Stock Market gains must be judged from the day after the Election, November 9, 2016, where the Market went up big after the win, and because of the win. Had my opponent won, CRASH!

— Donald J. Trump (@realDonaldTrump) August 25, 2019

https://platform.twitter.com/widgets.js

Stock market levels are the key measuring stick of the administration’s economic success according the Treasury Secretary Mnuchin. No wonder liquidity calls were needed in December as markets dropped 20%.

The bottomline on China: It’s a double edged sword that breeds both risk and opportunity:

Risk: Failure to curb the rhetoric and show lack of real progress risks triggering a global recession that is already a clear and present danger. Risk that markets are becoming a weaponized tool as part of the trade war. The Chinese already know it, and I suspect so does Trump and his team. They are playing with fire, the appear fine to let the fire smolder, but not let it burn out of control beyond, say 5% of market downside. Then they get itchy. But fires can spread so careful there, especially as there remains zero resolution or specifics other than vague hints at phone calls that neither side can agree to on whether they even took place.

Opportunity: Sentiment is getting so bad on this front that any sign of relief on tariffs and/or progress (i.e. what we saw again today in form of “phone calls” can trigger a massive relief rally. And frankly it only takes a tweet. We saw some of this in the middle of August when some tariffs were delayed. And Trump pretty much hinted at that being a replay possibility today, another rabbit to pull out of his hat again.

So none of this is a mystery, it’s a giant face saving dance with no specifics or path to resolution. Fact is prices can easily be subject to sell-offs and/or rallies based on vague information on tweets. This broad range risk profile remains on the plate into September.

The Fed:

The Fed’s in a very tough position. For one they, like anybody else, are trying to quantify the real risk to the economy coming from trade wars and the slowdown in data. But realistically they are also playing with fire. Reality is they have limited ammunition and need to be judicious how they proceed, for if a global recession is to ensue they only have 8 rate cuts to work with. In 2001 and 2007 it took 500bp in rate cuts to stop the bleeding, they don’t have that now.Hence they are desperately trying to cling to the “mid cycle adjustment” narrative.

Problem is markets are pricing in 100bp in rate cuts over the next year. Coming from 225bp that’s not a mid cycle adjustment. So markets and the Fed are at odds with each other and it comes down to confidence, efficacy and credibility.

To boot: Central banks are signaling that they alone can’t deal with a coming recession, they are asking for a coordinated global policy response. But as we just saw this weekend, the G7 couldn’t even agree on a joint memo for the first time in 44 years, so dysfunctional is the global political stage at the moment. Hence the issue of efficacy is paramount and markets may be placing too much trust in central banks.

Technicals:

Three important technical developments to keep an eye on:

-

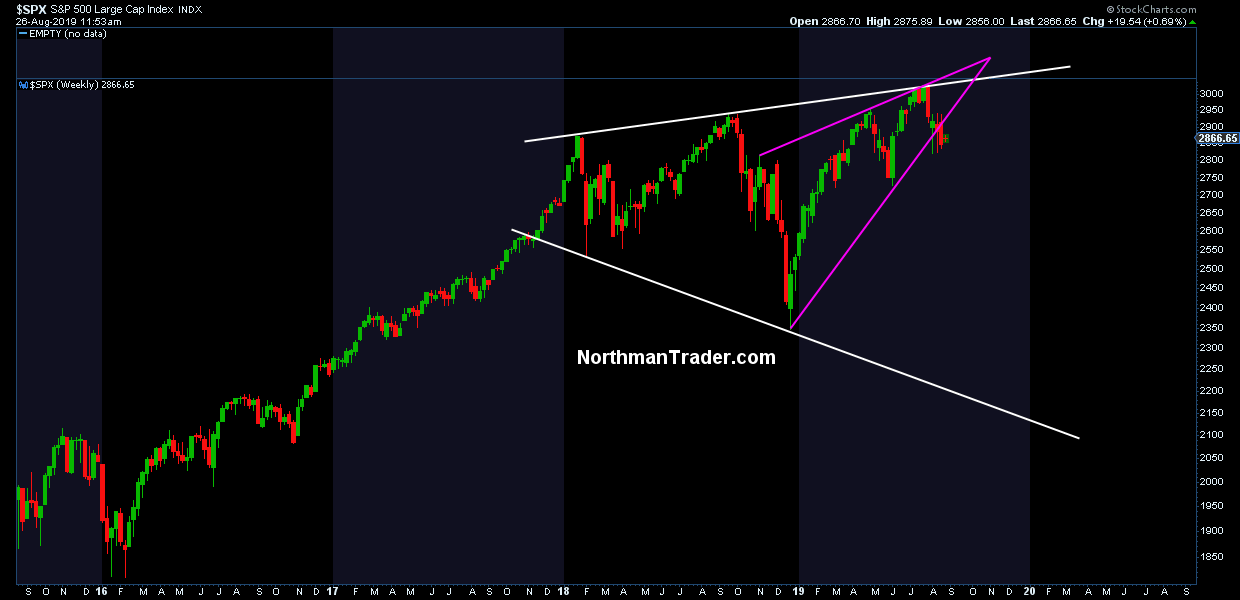

The megaphone structure remains intact and leaves room for lots of downside risk if a global recession is to unfold. The sell zone from 3000-3050 has confirmed and the larger pattern has risk into 2100-2200 $SPX.

-

A rising wedge has formed in 2019, and that wedge has broken to the downside, another bearish development:

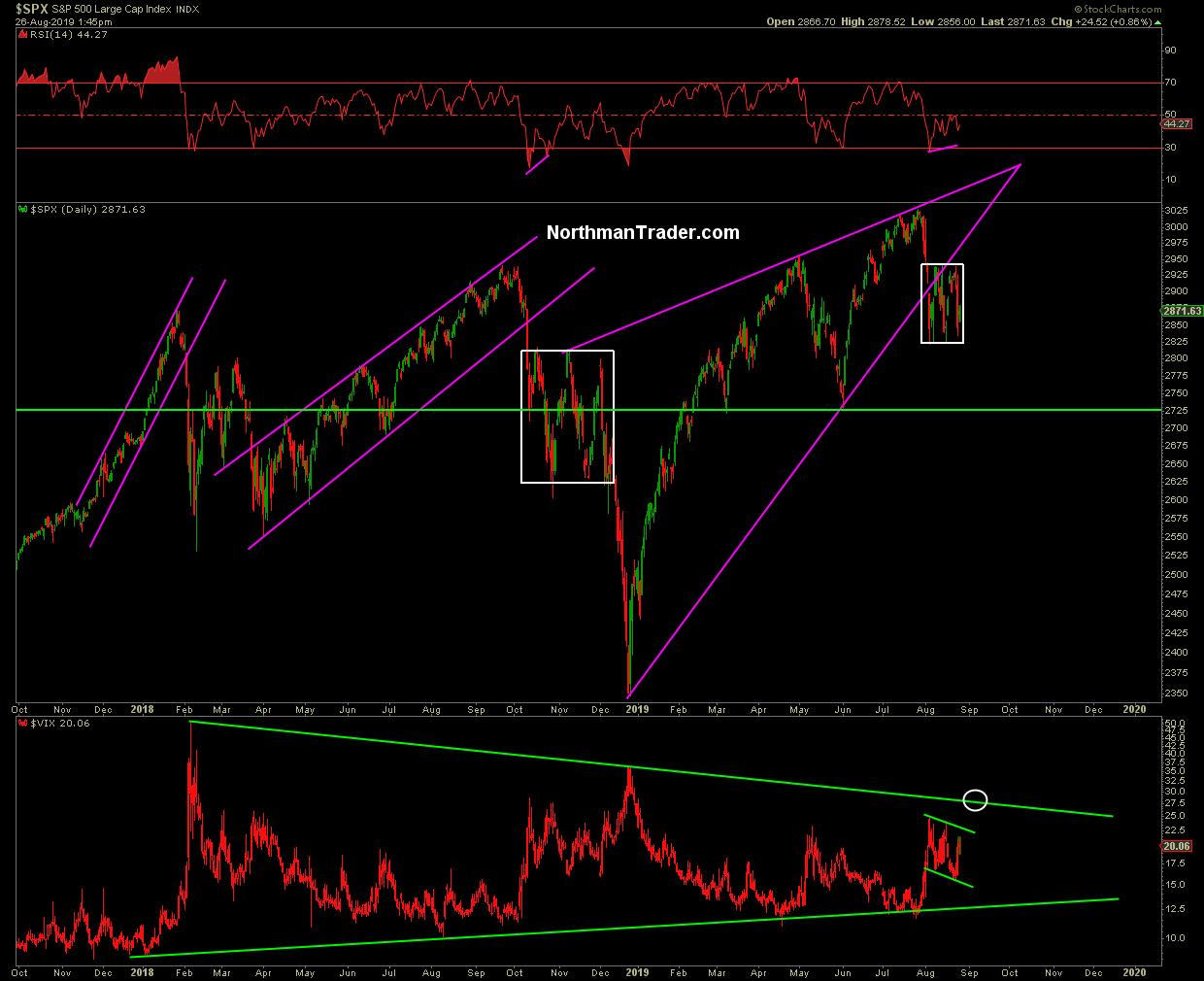

Indeed the last several weeks have shown a consolidation phase similar to the one from last fall, albeit it smaller:

Last year’s consolidation also came on the heels of a pattern break which then resolved lower. A confirmed break of that price consolidation zone to the downside risks lower prices still to come, i.e. a retest of the June lows or lower, and volatility $VIX could break higher into the 28/30 range as it appears to be forming a bull flag.

That said markets have been down 3 weeks in a row and oversold conditions are building which is likely to set up for another rally ahead of critical Fed and ECB meetings in September and certainly markets are attempting to do this today.

But be clear, markets remain structurally at risk and neither bulls or bears can rest easy here in this headline driven environment. It remains a big battle for control. The technicals say lower for markets, but it’s also clear that the forces of intervention are keeping a very close eye on markets and are stepping in to adjust their narratives at any sign of trouble. Looking at the charts they are increasingly at risk of losing control.

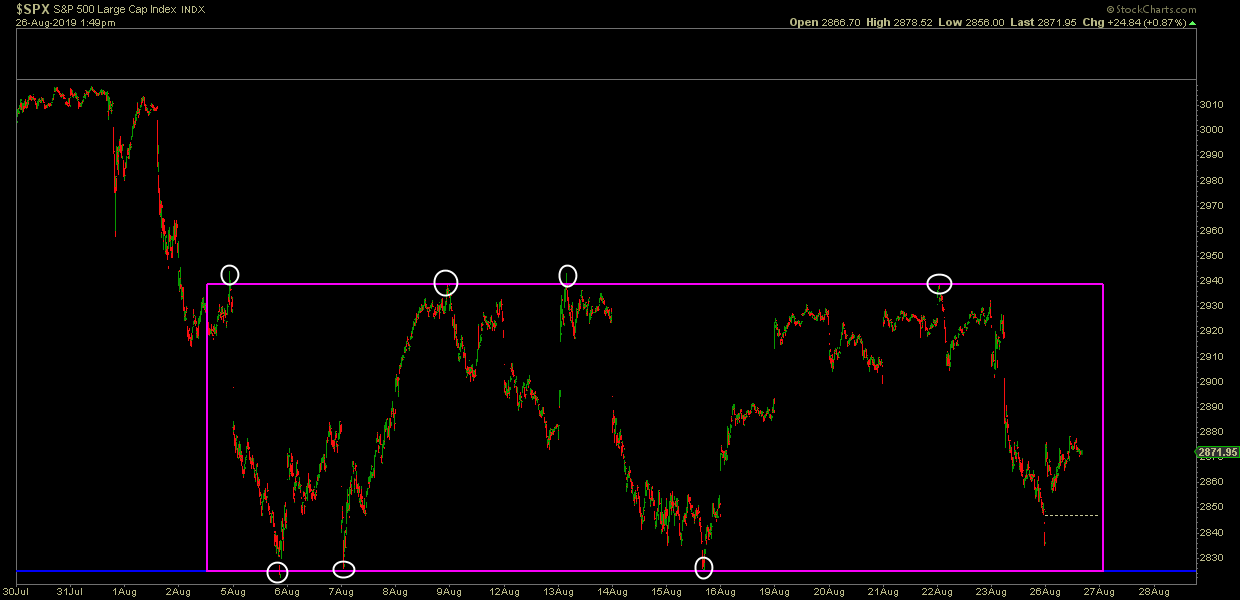

Fact is we remain in a precisely defined price consolidation zone and neither bulls or bears have won the final argument yet. That will only come on a confirmed breakout or breakdown. That range is now 2820-2935 on cash $SPX:

It’s easy to overcomplicate things and game theory the hell out of the Chinese, the Fed, seasonality, buybacks, etc. But let’s just keep it simple: Rallies keep being driven by rate cut hopes and trade optimism. Not by growth, earnings or fundamentals. Technicals continue to reflect patterns and structures that show risk to the downside building. But bears need to prove their case and that means break $SPX 2800 to the downside with conviction. But apparently a tweet or mere mention of a phone call are enough to scare them away 😉 For now anyways. Without a trade deal going beyond vague phone calls the global macro pictures keeps deteriorating. Every single day. Don’t believe me? Check yields. They seem hardly impressed by phone calls.

So what matters more, the trade war, the Fed or technicals? I can only answer for myself and that is technicals, the part of the equation I can see, analyze and react to with reason and a clear view of shifting risk/reward in either direction. I’ll leave the chasing of tweets to others.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com