Black Monday – Can It Happen Again?

Authored by Michael Lebowitz via RealInvestmentAdvice.com,

The 1987 stock market crash, better known as Black Monday, was a statistical anomaly, often referred to as a Black Swan event. Unlike other market declines, investors seem to be under the false premise that the stock market in 1987 provided no warning of the impending crash. The unique characteristics of Black Monday, the magnitude and instantaneous nature of the drop, has relegated the event to the “could never happen again” compartment of investors’ memories.

On Black Monday, October 19, 1987, the Dow Jones Industrial Average (DJIA) fell 22.6% in the greatest one-day loss ever recorded on Wall Street. Despite varying perceptions, there were clear fundamental and technical warnings preceding the crash that were detected by a few investors. For the rest, the market euphoria raging at the time blinded them to what in hindsight seemed obvious.

Stock markets, like in 1987, are in a state of complacency, donning a ‘what could go wrong’ brashness and extrapolating good times as far as the eye can see. Even those that detect economic headwinds and excessive valuations appear emboldened by the thought that the Fed will not allow anything bad to happen.

While we respect the bullish price action, we also appreciate that investors are not properly assessing fundamental factors that overwhelmingly argue the market is overvalued. There is no doubt that prices and valuations will revert to more normal levels. Will it occur via a long period of market malaise, a single large drawdown like 1987, or something more akin to the crashes of 2001 and 2008? When will it occur? We do not have the answers, nor does anyone else; however, we know that those who study prior market drawdowns are better prepared and better equipped to limit their risk and avoid a devastating loss.

History provides us with the gift of insight, and though history will not repeat itself, it may rhyme. While we do not think a 1987-like crash is likely, we would be remiss if we did not at least consider it and assign a probability.

Fundamental Causes

Below is a summary of some of the fundamental dynamics that played a role in the market rally and the ultimate crash of 1987.

Takeover Tax Bill- During the market rally preceding the crash, corporate takeover fever was running hot. Leveraged Buyouts (LBOs), in which high yield debt was used to purchase companies, were stoking the large majority of stocks higher. Investors were betting on rumors of companies being taken over and were participating in strategies such as takeover risk arbitrage. A big determinant driving LBOs was a surge in junk bond issuance and the resulting acquirer’s ability to raise the necessary capital. The enthusiasm for more LBO’s, similar to buybacks today, fueled speculation and enthusiasm across the stock market. On October 13, 1987, Congress introduced a bill that sought to rescind the tax deduction for interest on debt used in corporate takeovers. This bill raised concerns that the LBO machine would be impaired. From the date the bill was announced until the Friday before Black Monday, the market dropped over 10%.

Inflation/Interest Rates- In April 1980, annual inflation peaked at nearly 15%. By December of 1986, it had sharply reversed to a mere 1.18%. This reading would be the lowest level of inflation from that point until the financial crisis of 2008. Throughout 1987, inflation bucked the trend of the prior six years and hit 4.23% in September of 1987. Not surprisingly, interest rates rose in a similar pattern as inflation during that period. In 1982, the yield on the ten-year U.S. Treasury note peaked at 15%, but it would close out 1986 at 7%. Like inflation, interest rates reversed the trend in 1987, and by October, the ten-year U.S. Treasury note yield was 3% higher at 10.23%. Higher interest rates made LBOs more costly, takeovers less likely, put pressure on economic growth and, most importantly, presented a rewarding alternative to owning stocks.

Deficit/Dollar- A frequently cited contributor to the market crash was the mounting trade deficit. From 1982 to 1987, the annual trade deficit was four times the average of the preceding five years. As a result, on October 14th Treasury Secretary James Baker suggested the need for a weaker dollar. Undoubtedly, concerns for dollar weakness led foreigners to exit dollar-denominated assets, adding momentum to rising interest rates. Not surprisingly, the S&P 500 fell 3% that day, in part due to Baker’s comments.

Valuations- From the trough in August 1982 to the peak in August 1987, the S&P 500 produced a total return (dividends included) of over 300% or nearly 32% annualized. However, earnings over the same period rose a mere 8.1%. The valuation ratio, price to trailing twelve months earnings, expanded from 7.50 to 18.25. On the eve of the crash, this metric stood at a 33% premium to its average since 1924.

Technical Factors

This section examines technical warning signs in the days, weeks, and months before Black Monday. Before proceeding, the chart below shows the longer-term rally from the early 1980s through the crash.

Portfolio Insurance- As mentioned, from the 1982 trough to the 1987 peak, the S&P 500 produced outsized gains for investors. Further, the pace of gains accelerated sharply in the last two years of the rally.

As the 1980s progressed, some investors were increasingly concerned that the massive gains were outpacing the fundamental drivers of stock prices. Such anxiety led to the creation and popularity of portfolio insurance. This new hedging technique, used primarily by institutional investors, involved conditional contracts that sold short the S&P 500 futures contract if the market fell by a certain amount. This simple strategy was essentially a stop loss on a portfolio that avoided selling the actual portfolio assets. Importantly, the contracts ensured that more short sales would occur as the market sell-off continued. When the market began selling off, these insurance hedges began to kick in, swamping bidders and making a bad situation much worse. Because the strategy required incremental short sales as the market fell, selling begat selling, and a correction turned into an avalanche of panic.

Price Activity- The rally from 1982 peaked on August 25, 1987, nearly two months before Black Monday. Over the next month, the S&P 500 fell about 8% before rebounding to 2.65% below the August highs. This condition, a “lower high,” was a warning that went unnoticed. From that point forward, the market headed decidedly lower. Following the rebound high, eight of the nine subsequent days just before Black Monday saw stocks in the red. For those that say the market did not give clues, it is quite likely that the 15% decline before Black Monday was the result of the so-called smart money heeding the clues and selling, hedging, or buying portfolio insurance.

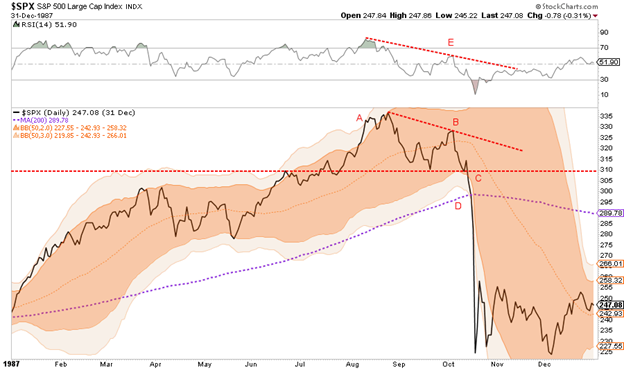

Annotated Technical Indicators

The following chart presents technical warnings signs labeled and described below.

-

A: 7/30/1987- Just before peaking in early August, the S&P 500 extended itself to three standard deviations from its 50-day moving average (3-standard deviation Bollinger band). This signaled the market was greatly overbought. (description of Bollinger Bands)

-

B: 10/5/1987- After peaking and then declining to a more balanced market condition, the S&P 500 recovered but failed to reach the prior high.

-

C: 10/14/1987- The S&P 500 price of 310 was a point of both support and resistance for the market over the prior two months. When the index price broke that line to the downside, it proved to be a critical technical breach.

-

D: 10/16/1987- On the eve of Black Monday, the S&P 500 fell below the 200-day moving average. Since 1985, that moving average provided dependable support to the market on five different occasions.

-

E: August 1987- The relative strength indicator (RSI – above the S&P price graph) reached extremely overbought conditions in late July and early August (labeled green). When the market rebounded in early October to within 2.6% of the prior record high, the RSI was still well below its peak. This was a strong sign that the underlying strength of the market was waning. (description of RSI)

Volatility- From the beginning of the rally until the crash, the average weekly gain or loss on the S&P 500 was 1.54%. In the week leading up to Black Monday, volatility, as measured by five-day price changes, started spiking higher. By the Friday before Black Monday, the five-day price change was 8.63%, a level over six standard deviations from the norm and almost twice that of any other five-day period since the rally began.

A longer average true range graph is shown above the longer term S&P 500 graph at the start of the technical section.

Similarities and differences

While comparing 1987 to today is helpful, the economic, political, and market backdrops are vastly different. There are, however some similarities worth mentioning.

Similarities:

-

While LBO’s are not nearly as frequent, companies are essentially replicating similar behavior by using excessive debt and leverage to buy their own shares. Corporate debt stands at all-time highs measured in both absolute terms and as a ratio of GDP. Since 2015, stock buybacks and dividends have accounted for 112% of earnings

-

Federal deficits and the trade deficit are at record levels and increasing rapidly

-

The trade-weighted dollar index is now at the highest level in at least 25 years. We are likely approaching the point where President Trump and Treasury Secretary Steve Mnuchin will push for a weak dollar policy

-

Equity valuations are extremely high by almost every metric and historical comparison of the last 100+ years

-

Sentiment and expectations are declining from near record levels

-

The use of margin is at record high levels

-

Trading strategies such as short volatility, passive/index investing, and algorithms can have a snowball effect, like portfolio insurance, if they are unwound hastily

There are also vast differences. The economic backdrop of 1987 and today are nearly opposite.

-

In 1987 baby boomers were on the verge of becoming an economic support engine, today they are retiring at an increasing pace and becoming an economic headwind

-

Personal, corporate, and public Debt to GDP have grown enormously since 1987

-

The amount of monetary stimulus in the system today is extreme and delivering diminishing returns, leaving one to question how much more the Fed can provide

-

Productivity growth was robust in 1987, and today it has nearly ground to a halt

While some of the fundamental drivers of 1987 may appear similar to today, the current economic situation leaves a lot to be desired when compared to 1987. After the 1987 market crash, the market rebounded quickly, hitting new highs by the spring of 1989.

We fear that, given the economic backdrop and limited ability to enact monetary and fiscal policy, recovery from an episodic event like that experienced in October 1987 may look vastly different today.

Summary

Market tops are said to be processes. Currently, there are an abundance of fundamental warnings and some technical signals that the market is peaking.

Those looking back at 1987 may blame tax legislation, portfolio insurance, and warnings of a weaker dollar as the catalysts for the severe declines. In reality, those were just the sparks that started the fire. The tinder was a market that had become overly optimistic and had forgotten the discipline of prudent risk management.

When the current market reverses course, as always, there will be narratives. Investors are likely to blame a multitude of catalysts both real and imagined. Also, like 1987, the true fundamental catalysts are already apparent; they are just waiting for a spark. We must be prepared and willing to act when combustion becomes evident.

Tyler Durden

Wed, 09/11/2019 – 10:05

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com