Investors Are The Most Apocalyptic Since August 2009, Completely Ignoring Last Week’s Quant Crash

Less than 10 days ago, Morgan Stanley laid out what was the biggest challenge facing the market: the fact that nobody was prepared, or certainly positioned, for the economy to turn better. Well, just one day later, the biggest quant crash since 2007 followed, as consensus factor positions violently reversed following a smattering of good news (and IG rate locks) that sent yields higher, and cascaded into the biggest short squeeze of value positions, coupled with a furious crash in momentum stocks.

In short Morgan Stanley was right, and for a few days, the world recoiled in horror as the biggest consensus trade in the world suffered the market equivalent of a train wreck.

And yet, after billions in P&L quickly changed hands from Quant Fund A to Quant Fund B, has anything really changed?

If one looks at the latest – August – Bank of America Fund Manager Survey, which was conducted September 6-12, so after last week’s quantitanic events, polling 235 panelists with $683bn AUM participated in total, the answer is a resounding no because despite the market’s violent reversal away from recession trades, the overarching consensus on Wall Street is that a recession is imminent.

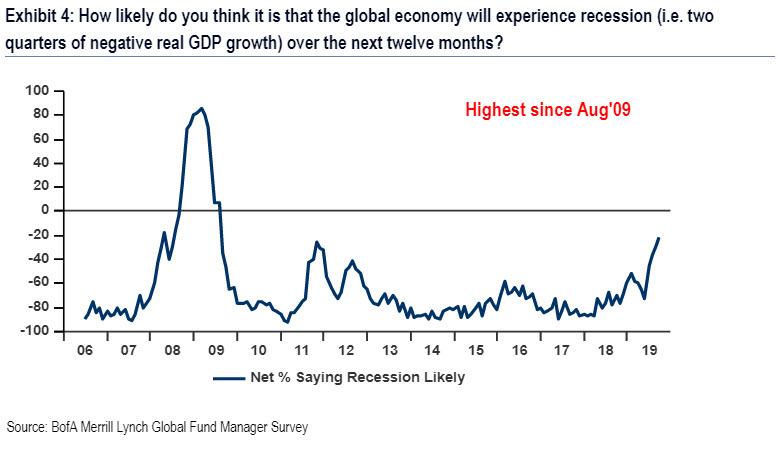

Indeed, as shown in the chart below, recession concerns continue to temper investor risk appetite as 38% of investors polled expect a recession over the next year versus 59% who see a recession as unlikely, the highest net recession risk since August, 2009.

Alongside this, investors have thrown in the towel on any tightening for the foreseeable future, and in September, just 21% of surveyed investors said they expect short-term rates to rise over the next 12-months, a strong reversal from Sept’18 when 87% FMS investors expected higher short-term rates; that said, there was a modest rebound from last month when short-term rate expectations were at their lowest since Nov’08.

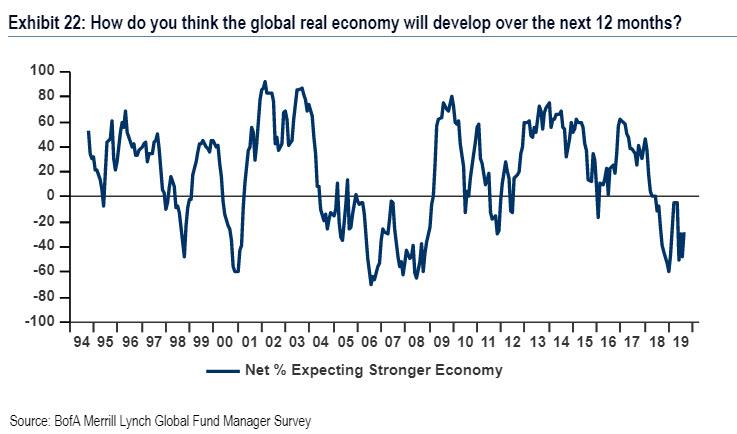

Furthermore, as BofA CIO Michael Hartnett notes, there has been “no inflection” in FMS macro sentiment, despite a very small pick-up in global growth expectations to -28% (from -48%) insufficient to boost profits outlook (still in EPS recession, consensus YoY global EPS growth now -3.1%).

Meanwhile, just 11% of FMS investors expecting higher global CPI in the next 12 months, which while up 3%t MoM and 10%t from recent low in Jul’19, is just barely higher than the most bearish FMS inflation outlook since Jul’12.

Amid such apocalyptic sentiment and expectations for plunging rates (to even lower levels from the current record lows), it is perhaps no surprise that fund managers remain overweight assets that outperform in a backdrop of low growth and low rates and have not shown signs of a rotation into value assets (those geared toward rising interest rates and earnings). This would mean that for all the drama over last week’s quant quake, virtually not a single (human) investor has actually changed their strategic positioning.

Furthermore, since the market tends to be a reflexive machine which is driven as much by beliefs as money, it is troubling that even after last week’s historic outperformance of value over growth, only net 7% of FMS investors expect value to outperform growth over the next 12 months… which nonetheless is up 12ppt vs. last month, which was the lowest level since the Global Financial Crisis. Here BofA rubs some more salt in the wound reminding its readers that capitulation into growth stocks by FMS investors last month coincided with a sharp outperformance of value in the past three weeks.

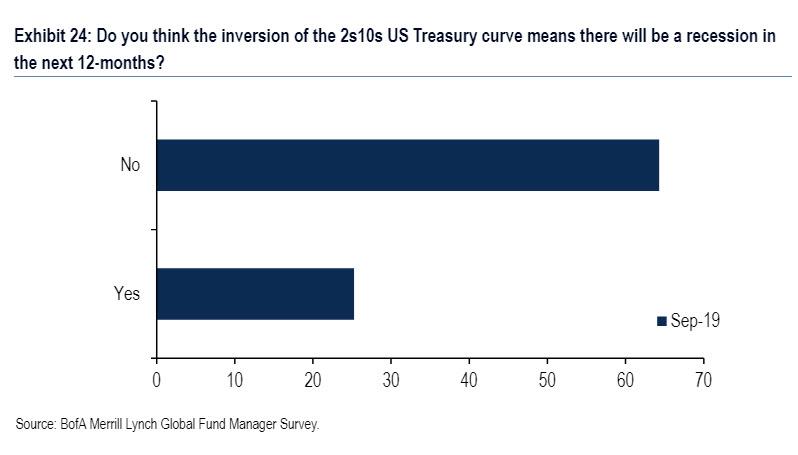

Ironically, all this takes place even as investors refuse to accept reality, and a whopping 64% of respondents said they do not think an inversion of the 2s10s US Treasury curve means there will be a recession in the next 12-months… even as they allegedly are positioning for just such a recession.

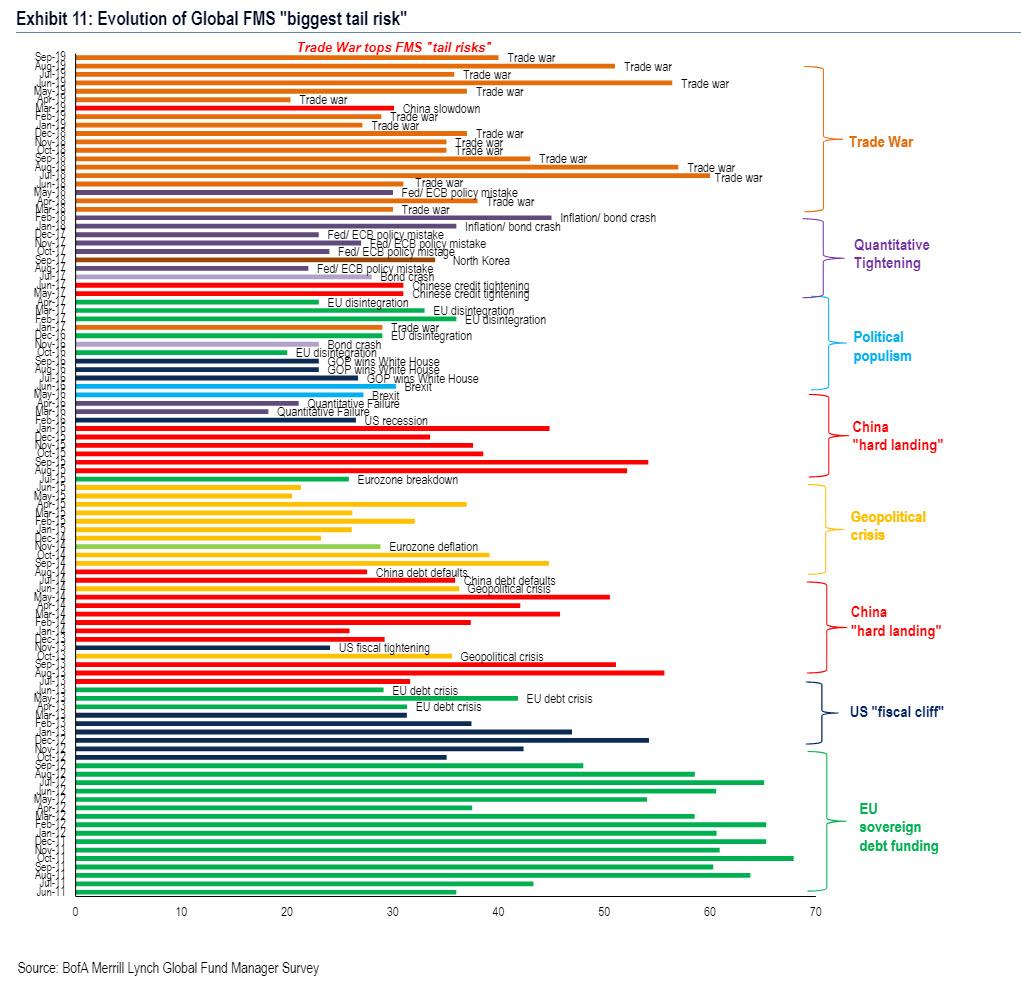

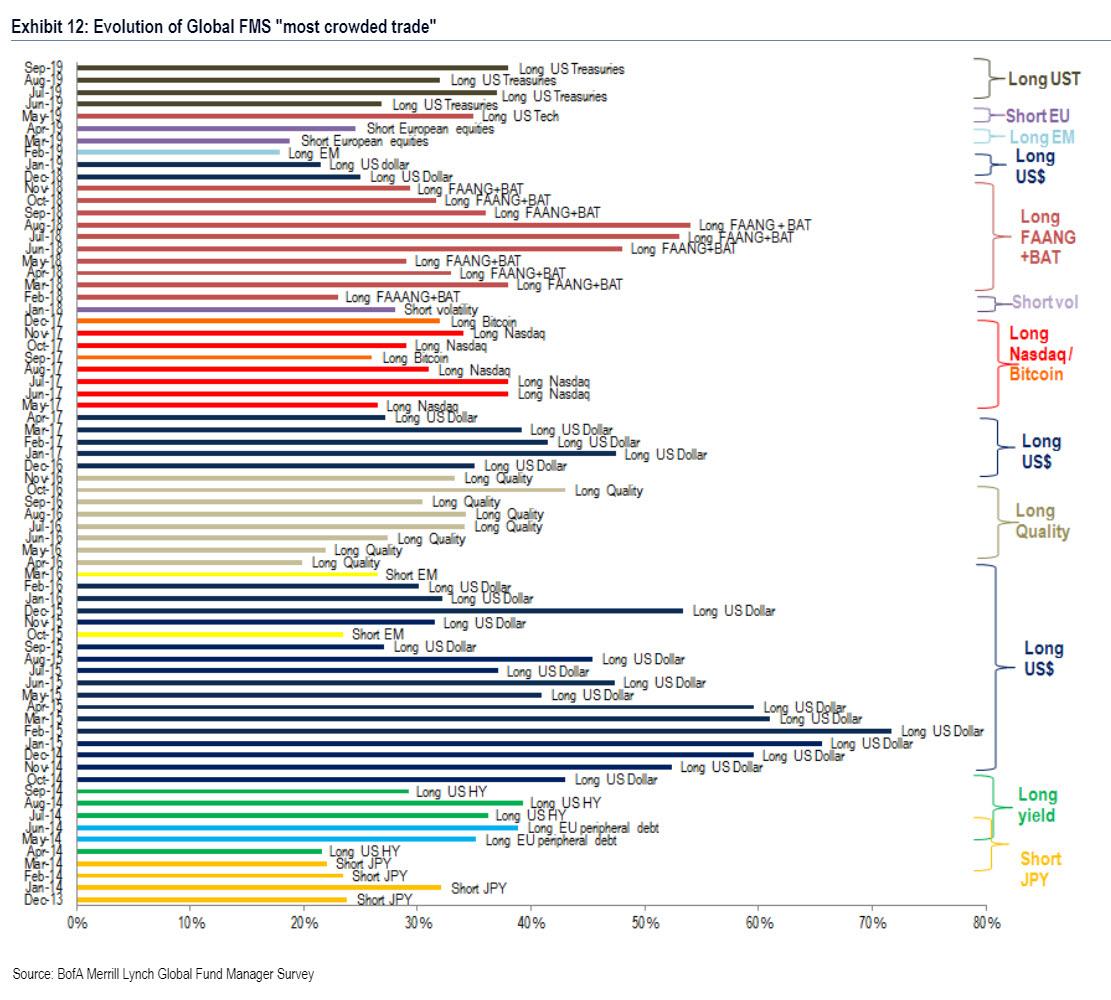

Finally, focusing on everyone’s two favorite charts from the monthly FMS survey, we find no surprises in either the biggest tail risk, or the “most crowded trade”, because in 17 of past 19 months, trade war has been the top tail risk (with monetary policy impotence now #2; onus shifts to “fiscal policy” which FMS investors say is most restrictive since Dec’16;

There was also no surprise what consensus saw as the “most crowded trade”, which for a 4th month was “Long US Treasurys”, although market leadership has been relatively narrow and since 2013 it has shifted from high yielding debt; long US$; long Quality; long Tech; long Emerging Markets; and now long rates.

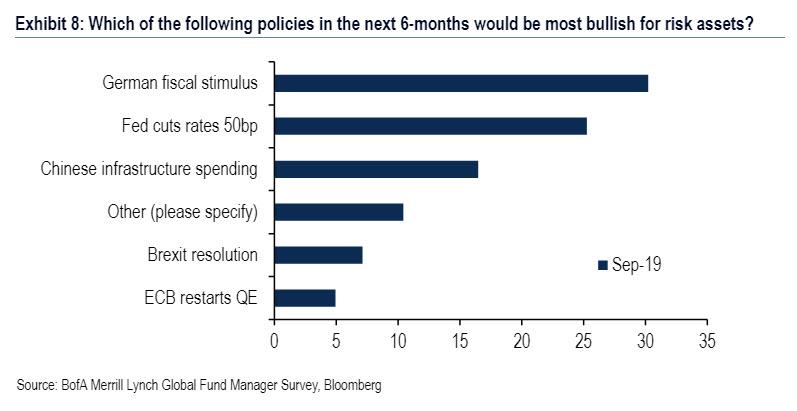

Finally, outside “trade deal” (38% FMS investors expect no resolution), top 3 most bullish policy actions = German fiscal stimulus, 50bps cut by Fed, China infrastructure = steeper yield curve.

Incidentally, if anything, the chart above confirms just how clueless Wall Street is as a German fiscal stimulus, all €50BN of it, would have absolutely no impact on the bigger economic picture, as that less than is the amount of liquidity the Fed just injected in one overnight repo.

Tyler Durden

Tue, 09/17/2019 – 15:11

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com