The Fed Has Lost Control Of Rates Again

Something critical is going on in overnight funding markets: ever since March 20, the Effective Fed Funds rate has been trading above the IOER. This is not supposed to happen, and it just got significantly worse.

As a reminder, ever since the financial crisis, in order to push the effective fed funds rate above zero at a time of trillions in excess reserves, the Fed was compelled to create a corridor system for the fed funds rate which was bound on the bottom and top by two specific rates controlled by the Federal Reserve: the “floor” for the corridor was the overnight reverse repurchase rate (ON-RRP) which usually coincides with the lower bound of the fed funds rate, while on top, the effective fed funds rate is bound by the rate the Fed pays on Excess Reserves (IOER), which served as the corridor “ceiling.”

Or at least that’s the theory. In practice, the effective FF tends to occasionally diverge from this corridor, and when it does, it prompts fears that the Fed is losing control over the most important instrument available to it: the price of money, which is set via the fed funds rate.

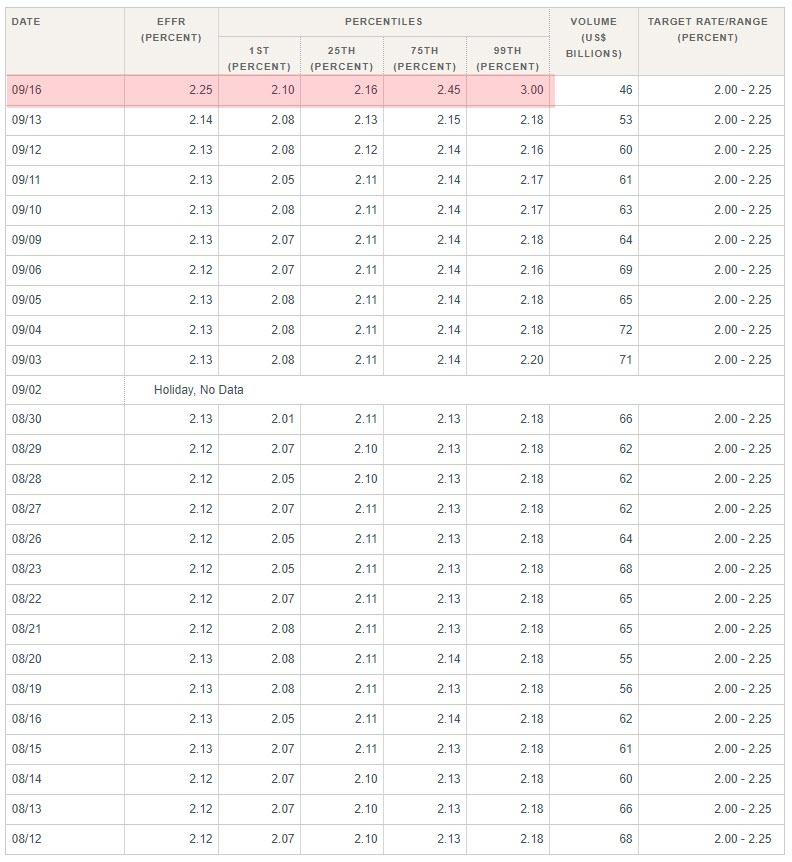

Ever since March 20, this fear is front and center because as shown in the chart below, starting on March 20, the effective Fed Funds rate rose above the IOER first by just 1 basis point. The Fed attempted to technically tamp this down.. and failed. But today the Effective Fed Funds Rate has exploded….

Smashing above the IOER…

Source: Bloomberg

As we noted earlier, no one is sure of what is driving this apparent liquidity shortage

-

elevated UST supply,

-

bloated dealer balance sheets and year-end regulatory constraints

-

a banking system near reserve scarcity,

-

investors selling bonds back to dealers, and

-

banks and money-market funds to make their quarterly tax payment.

The bottom line is simple – The Fed has lost control of its rate-control mechanism.

So what should the Fed do to regain control over interest rates?

According to Barclays to address the expected increase in fed funds volatility, the Fed, having ended the balance sheet runoff this summer instead of waiting until September, could create a standing repo facility – something which has been rumored for months – or conduct standard open market operations, injecting even more liquidity into the system.

But as we noted earlier, the problem for the Fed is that following today’s massive move in repo higher, it now appears that the Fed is once again behind the curve, and this time the funding squeeze could have dire consequences for not only the economy but the market, as the broken repo plumbing means that despite $1.4 trillion in excess reserves, one or more banks are suddenly left without liquidity, which as we explained over a month ago in “Forget China, The Fed Has A Much Bigger Problem On Its Hands”, the only alternative Powell may soon have is to restart QE.

Fun week so far:

-

Monday: biggest ever surge in oil

-

Tuesday: biggest ever surge in GC repo

But stocks are near record highs, because… The Fed.

Tyler Durden

Tue, 09/17/2019 – 09:15

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com