A Dive Into WeWork’s $3.3 Billion In CMBS Exposure

Authored by Manus Clancy & Catherline Liu, follow up to “Here Are The Billions Of Loans Exposed To A Potential WeWork Bankruptcy“

Worrisome news surrounding WeWork continues to stream in after the co-working giant’s recent IPO postponement, with the firm’s roster of high-profile staff departures growing by the day and S&P executing a downgrade of its credit status to below junk bond territory.

With there being some uncertainty about the firm’s profitability prospects, its ability to raise capital for future growth, as well as other liquidity concerns, the new CEO is reportedly exploring cost-cutting measures. This includes the shedding of some of its assets, such as the potential sale of three of its latest business acquisitions.

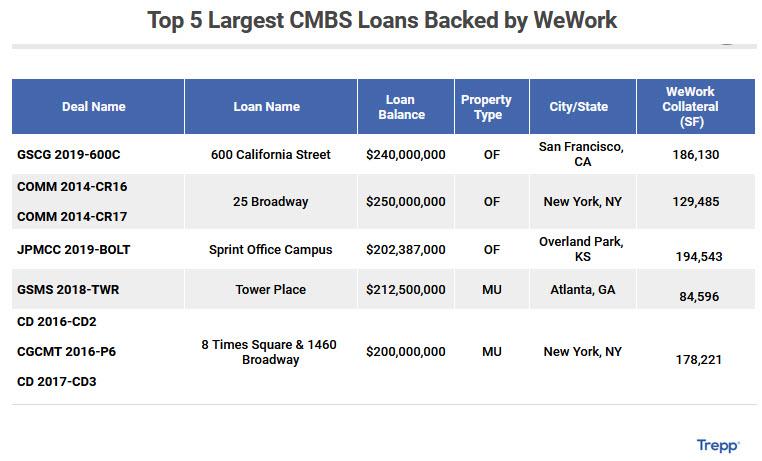

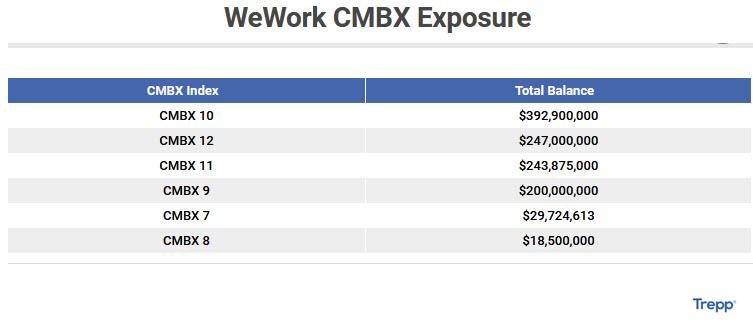

WeWork is a top-five tenant at 36 office facilities behind more than $3.3 billion in CMBS debt across 50 deals, with the brunt of these leases scheduled to expire between 2024 and 2035. In terms of state concentration, New York contains the largest WeWork CMBS footprint with total debt amounting to $1.5 billion across 29 notes. California and Massachusetts carry the next two largest loan exposures at $803.3 million across 14 notes and $230.0 million across three notes, respectively.

The co-working giant also recently sought CMBS financing to fund its $330 million acquisition of 600 California Street, marking it the firm’s very first San Francisco office purchase. The $240 million loan is securitized in the single-asset GSCG 2019-600C deal which closed in late August. (So in this case, there are two levels of WeWork exposure – as lessee and as the property owner.)

Roughly 78% of the WeWork-backed CMBS loans were recently issued from 2016 onward and have fairly minimal seasoning – so all of the loans are current on payment at the moment. From a credit perspective, the loans have a weighted-average LTV of 55.89% and a weighted-average DSCR of 1.92x. With a lot of the knowledge and investor jitters surrounding WeWork as a tenant already baked into new issue pricing, it will take some time for the distress to play out.

Last month, Trepp spoke with Debtwire, on their podcast, “ABS in Mind: WeWork, the unwanted tenant”. We discussed Trepp’s findings while digging into WeWork’s CMBS exposure.

WeWork is certainly a growing exposure for the CMBS market; one that concerns people. The volume of WeWork loans in CMBS, post 2010, is approaching 1% of the entire CMBS market and about 4% of loans backed by offices, so that exposure is meaningful.

The biggest issue is not the pulling of the IPO per se, but the broader concerns about the firm’s viability. The worst-case scenario would be that the firm continues to burn through cash and can no longer support all of its lease obligations. If that were followed by a period of non-payment of rent by WeWork, but physical occupancy and current payments by the firm’s sub-lessees, that would make for some interesting work for landlords and special servicers. Stay tuned.

Listen to the podcast here:

[soundcloud url=”https://api.soundcloud.com/tracks/679653815″ params=”color=729eff” width=”100%” height=”166″ iframe=”true” /]

Tyler Durden

Sat, 10/05/2019 – 13:19

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com