Platts: 6 Commodity Charts To Watch This Week

Via S&P Global Platt’s ‘The Barrel’ blog,

A new production record for Permian basin gas, and rising transport costs for crude oil into Asia, are top of S&P Global Platts editors’ picks this week. Plus: EU renewables output, Egypt’s return to abundant natural gas supply, a US power price spike, and the squeeze on European steel mill margins.

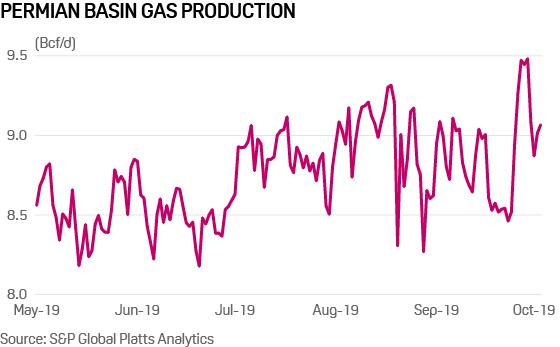

1. Gas pipeline start-up helps Permian output to new highs

What’s happening? Gas production in the Permian Basin of West Texas edged up to a record high in late September, rising to nearly 9.5 Bcf/d, following the startup of Kinder Morgan’s Gulf Coast Express Pipeline. The 2 Bcf/d intrastate pipeline, which is designed to move associated gas production from the US’ most prolific shale play to the Texas Gulf Coast, entered commercial service about one week ahead of schedule on September 25. In October, Permian production has backed off to about 9 Bcf/d, but is still outpacing output levels that averaged less than 8.8 Bcf/d prior to the pipeline’s startup. Gas prices in the Permian Basin have come under significant pressure in recent days as incremental production floods the West Texas market. On September 27, cash prices at the Waha hub fell nearly 50 cents in intraday trade, tumbling to $1.02/MMBtu, before settling around $1.20/MMBtu.

What’s next? Weaker shoulder season demand is likely to drive additional price volatility at Waha this month and into November. In recent trading, the balance-of-month October forward price at Waha fell to $1.06/MMBtu, down from over $1.60/MMBtu just last week.

2. Crude oil transport costs shoot up on US sanctions

What’s happening? Global tanker freight rates continued to soar last week, with costs for US tankers bound for Asia hitting all-time highs, after US sanctions on two shipping entities of China’s transport giant COSCO fueled concerns over tanker availability and the cost of transporting oil. COSCO, which is accused of breaking US sanctions on Iranian oil exports, shipping unit operates more than 100 tankers including VLCCs, suezmaxes, aframaxes and panamaxes. The cost of taking a VLCC, which normally carries 2 million barrels, from the US to China hit a record $10 million this week as a result.

What’s next? Due to the rising cost of tanker transport, crude buyers will continue to look for supplies from closer, regional alternatives – a trend that already hitting regional arbitrage economics and denting demand for specific crude grades. On October 3, ICE Brent futures’ premium over Dubai crude slipped below a key $3/b inflexion point for the first time since August, with the arbitrage for North Sea light crude to Asia curbed by the surge in freight costs.

3. Europe’s green power generation keeps rising

What’s happening? Combined wind and solar generation across Europe’s Big Five power markets (Germany, France, Spain, Italy, GB) is up 11% year on year. The green energy produced to end-September is equivalent to Europe’s total steam coal imports in 2018. Over the summer cheap gas and strong renewables kept a lid on power prices and allowed below-normal hydro reservoir stocks to be preserved for more lucrative winter price period.

What’s next? To date German onshore wind has been the single most disruptive source of green power in Europe. As German onshore additions slow, offshore wind is the new force to be reckoned with. The last turbine has just been installed at the 1.2 GW Hornsea One facility in UK North Sea waters, the world’s largest to date. With a 50% load factor, each megawatt is going to punch well above its weight versus onshore wind and solar, with Hornsea producing enough power for a million households.

4. Changing fortunes of Egypt’s gas sector

What’s happening? Egyptian gas production has been rising quickly over the past two years, buoyed mostly by the startup of the supergiant Zohr field operated by Italy’s Eni. The country is again a net exporter of gas as production growth has outpaced demand growth.

What’s next? Egypt has resumed large-scale LNG exports from the Idku plant and plans to restart LNG supplies from the Damietta plant by the end of 2019. Egypt is also set to begin to import Israeli pipeline gas from 2020 – mostly for domestic use, but potentially to add to its growing surplus of gas for export as LNG.

5. Extreme weather creates volatility in US power markets

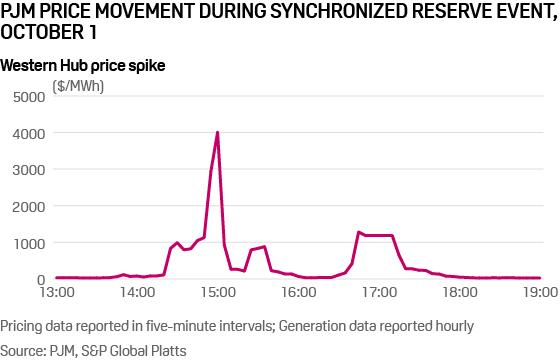

What’s happening? Unseasonably warm US Mid-Atlantic weather with temperatures above 90 degrees Fahrenheit resulted in PJM Interconnection under-forecasting load by roughly 5 GW on October 1, which triggered a reserve event and shortage pricing that drove real-time power prices above $4,000/MWh. Oil-fired resources quickly ramped up in response. The following day, PJM issued its first demand response action in five years as the heat continued, calling on customers to reduce consumption. Preliminary peak load over 126,000 MW would be the second-highest October demand total for the PJM footprint on record.

What’s next? Continued erratic weather could lead to more supply/demand and pricing volatility in US power markets.

6. Europe’s steel mills see scant relief from lower input prices

What’s happening? European hot-rolled coil (HRC) steel spreads in the third quarter remain weak, taking into account lower regional HRC steel prices and declines in coking coal and ferrous scrap, analysis by S&P Global Platts shows. Steel to raw materials spreads were largely flat in Q3 from the low in Q2, and much weaker than in Q1 2019 or 2018 and 2017. The Northwest Europe HRC to raw materials spread averaged at Eur251.40/mt ($276.54/mt) in September, based on Platts’ calculations. For Q3, the indicative margins averaged Eur235.75/mt, from Eur229/mt in Q2. The dip in steel spreads over the past six months continues to press steel mills to cut costs and reduce marginal steelmaking, to minimize raw materials purchases and higher-grade feedstocks as productivity falls, according to market sources.

What’s next? Mills are looking for further cost cuts, and capacity adjustments to meet underlying weak steel demand are being implemented. Higher regional steel prices are likely to be the catalyst for higher European steel to raw materials spreads and steelmaking profits, as coking coal and iron ore spot prices remain better supported by demand in China, which grew this year to a new high.

Tyler Durden

Mon, 10/07/2019 – 13:10

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com