Panic Behind The Scenes: China’s Capital Outflows Are Soaring

For months, pundits have been looking at China’s official data – be it the PBOC’s reserve data or SAFE’s monthly flow report – for indication that capital flight is picking up again as it did in 2015 in the aftermath of the first yuan devaluation, and so far the data has refused to validate predictions that Chinese depositors are quietly pulling their money from China’s financial system.

Does this mean that Beijing has been successful in implementing draconian controls on outbound foreign investment and other capital movements to lock the front door through which money used to leave China.

That’s one possibility. However, as the WSJ notes, instead of using the front door, Chinese capital is increasingly “walking through the back door” following the recent sharp devaluation in the yuan, which has slumped 6% against the dollar since late April, and 10% since mid-2018; of course should the back door open any wider Beijing will find itself again forced to sell down big parts of its currency reserves to avoid a panic. Worries about cracks in currency fortress China are another reason Beijing is likely to remain wary of aggressive monetary stimulus.

It’s also why China – the country where economic data is anything but what is represented by the government – has no qualms about fabricating data to refute a worst case scenario that would unleash a self-fulfilling prophecy leading to more devaluation and more capital flight.

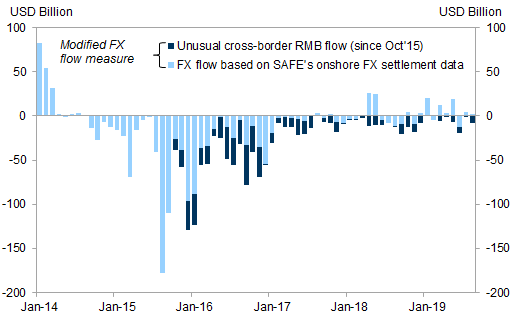

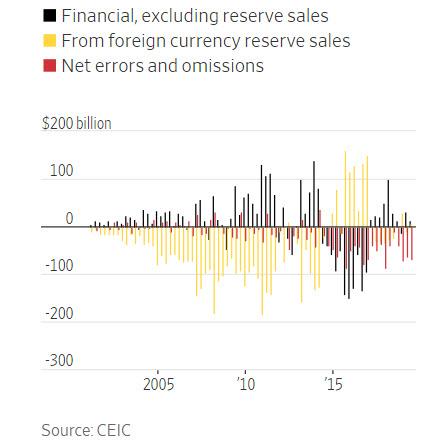

And yet, despite Beijing’s best efforts at misdirection – and outright data fabrication – there is a relatively simple way to keep track of what is really happening with China’s fund flows behind the scenes. As the WSJ notes, the relevant figure to track is China’s “errors and omissions” line in its balance of payments.

This number represents the residual of the main BOP accounts registering trade and investment flows—in other words, capital that has moved across China’s borders without being documented. An equation “plug.”

Whereas in most countries this line item is relatively small, in China, since 2014 when Beijing decided to stop appreciating the yuan against the dollar, it has become :persistently and mysteriously large and negative” with analysts at Rhodium Group and others long suspecting this item represents undocumented capital flight.

And while this shadow capital flight moderated in 2018, the trend recently became even more striking, as “errors and omissions” hit a record first-half high of $131 billion in 2019, the WSJ notes citing Gene Ma of the Institute of International Finance, much larger than the first-half average of $80 billion during the last period of big capital outflows in 2015 and 2016.

On the surface, this suggests that true capital flight is now twice as large as what was observed after the 2015 devaluation, and indicated that while measures instituted a few years ago to limit capital flight have appeared effective, China remains vulnerable to rising outflows through unofficial channels. Furthermore, the country has yet to report its third-quarter figures, following the big yuan depreciation in early August, when it dipped below 7.00 against the dollar for the first time in a decade.

So what to make of this? Two things, and neither is good.

First, as the WSJ notes, Beijing’s decision to allow its currency to offset the pressure from the trade war has been one of China’s key survival strategies so far, but “with increasing signs that the ocean of capital sloshing around behind China’s dike is finding new cracks—and out-of-control domestic food-price inflation adding to the stakes—that strategy is looking riskier.”

The second one is that with capital already fleeing China, any future attempts to boost China’s economy using monetary policy will be promptly punished, which also explains why the world is sinking into recession: as a reminder, in a world where China has been the primary growth dynamo thanks to its tremendous credit impulse after the financial crisis, this massive credit creation mechanism has now shut down…

… as Beijing runs the risk of an out-of-control capital flight should it push too hard to stimulate the local economy at the expense of another sharp devaluation in the yuan. In short, whereas the official data does not show it, reading between the lines suggests that the global economy may be on the verge of collapse.

Tyler Durden

Tue, 10/15/2019 – 21:15

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com