World Stocks Drop, Futures Tread Water After China Reports Worst GDP Growth In 30 Years

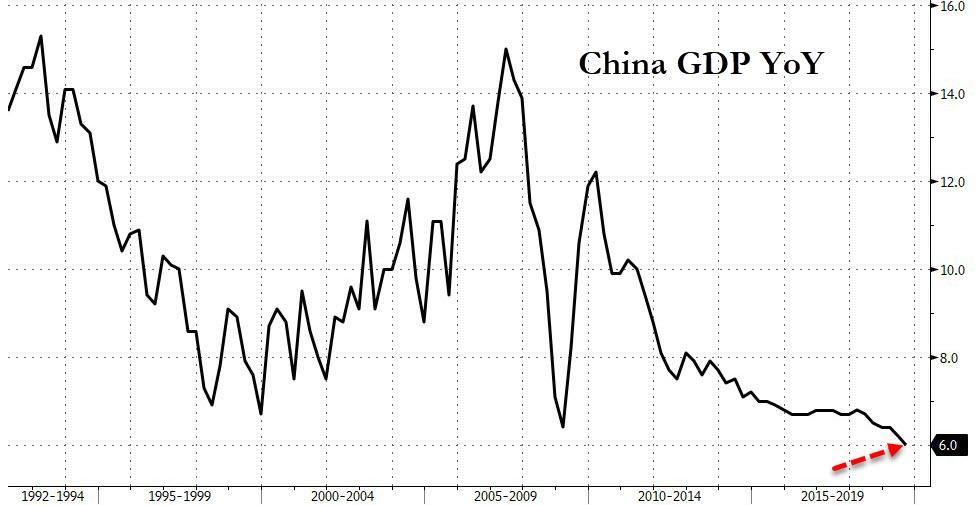

World stocks slipped and US equity futures were unchanged after China posted its weakest growth rate in 30 years, as Q3 GDP disappointed, printing a below-expectations 6.0%...

… while the dollar was set for its worst week in almost four months having been pummeled by pound and euro Brexit rallies.

As a result of the latest disappointing GDP print, Chinese stocks slumped as large banks and insurers weighed on the gauge, their losses accelerating in afternoon trade as the Shanghai Composite dropped 1.2%, with the CSI 300 Index posting its biggest decline this month led lower by information technology shares. Overall, Asian stocks slipped, snapping a five-day rising streak, with most markets in the region dropping, while India bucked the trend. The Topix dropped 0.1%, dragged by telecommunication giants. Japan’s key consumer prices rose at the slowest clip in more than two years in September, the latest sign of weakening inflation. India’s Sensex climbed 0.8%, set for its best week since May, as quarterly earnings reports added to investor optimism

European stocks rebounded from an early loss and were trading unchanged last, despite a sharp reverse in car shares after Renault plunged following the latest profit warning, while rival Volvo declined after saying it was preparing for more output cuts for next year. Yogurt giant Danone dropped after reducing its 2019 outlook.

Across the Atlantic, after fading Thursday’s modest move higher, US equity futures also rebounded after ended Thursday just 1% from an all time high,

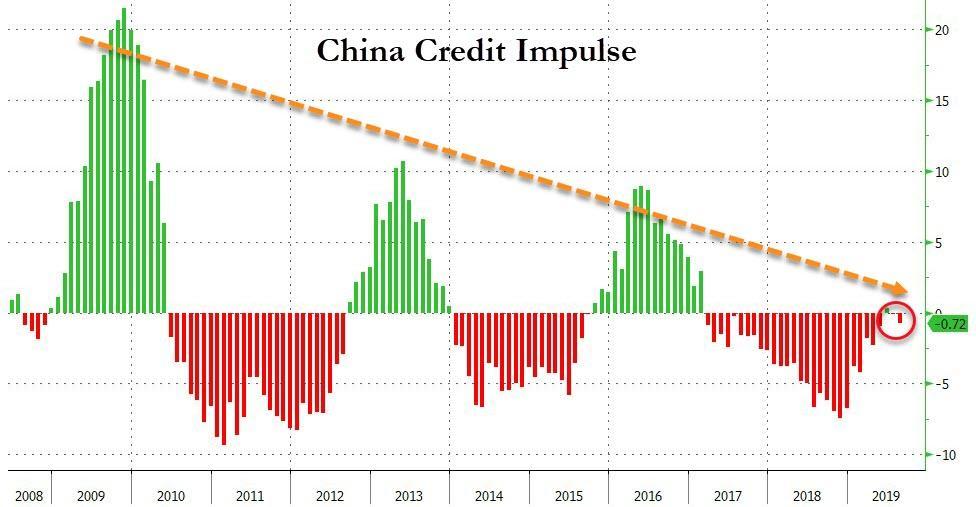

Yet as the world careens to what now appears to be an unavoidable recession, largely driven by the ongoing collapse in China’s credit impulse which is now paralyzed as Beijing is simply unable to inject the amounts of debt needed to push its – and the global – economy higher…

… the spin quickly emerged to mitigate the latest dismal data: it could have been worse.

“You can’t get away from the fact that China is slowing, but it’s not slowing more than we thought,” said Michael Metcalfe, head of global macro at State Street Global Markets . “We know that Q4 is going to be a soft patch, but to a degree policymakers are ahead of this, so as long as we don’t have an escalation of the trade war now I think markets can handle it.”

See, everything’s ok. They got this.

Or maybe not: as Bloomberg notes, investors are seeking a fresh stimulus for equities as the weekend approaches, even though US earnings so far have been relatively upbeat, after Morgan Stanley bucked concerns about weak growth.

“With investors pricing in Boris Johnson’s inability to get his Brexit deal passed through the House of Commons, and the slowing activity data out of China this morning, there’s probably less likelihood of another leg higher coming for the S&P to set a new record today,” Aneeka Gupta, associate research director at asset manager WisdomTree in London, said in an interview. “The companies reporting earnings don’t look big enough to change global sentiment.”

So as futures treaded water and were looking for a catalyst for another leg higher, treasuries ticked lower with 10Y yield rising to 1.77%, while most sovereign bonds fell across Europe. German Bunds yields were trading around -0.40%, the highest since early August; the Bund yield is now up 16 bps since Irish and British leaders said on Oct. 10 they saw a path to a Brexit deal, which boosted risk appetite and weakened demand for safe-haven assets like bonds; meanwhile the yield on Greek 10Y bonds fell to a new all time low of 1.31%.

In currencies, sterling pushed higher again after initially dropping to 1.2840, rising as high as 1.9020 before again fading, having previously scored its best six-day streak in near 30 years on Thursday after Britain and the EU sealed a new Brexit deal. Doubts about whether the deal will be approved in the British parliament were still sky high, though, with swathes of lawmakers, who are either reluctant about Brexit or worried the deal is not a clean enough break, due to debate the deal in a rare Saturday sitting.

“Whatever was agreed last night with the EU still has to go through the British parliament… the uncertainty surrounding that still hasn’t changed one iota,” said James McGlew, executive director of corporate stockbroking at Argonaut.

Elsewhere, the euro rested at $1.1125 , not far from $1.1140, its highest since Aug. 26. The dollar remained weak too having seen this week’s weak retail sales data and more U.S. interest rate cut talk contribute to its biggest weekly slide since June. The lira jumped after Turkey and the U.S. agreed to a temporary cease-fire plan for Syria.

In geopolitics, the Kurdish-led SDF accused Turkey forces of targeting both civilian and military areas in Ras al ain. Meanwhile, House Speaker Pelosi and Senate Democratic Leader Schumer said the US-Turkey agreement seriously undermines credibility of US foreign policy and that the House will pass a bipartisan sanctions package on Turkey next week. US Secretary of State Pompeo says he had a productive meeting with Israeli PM Netenyahu, where they talked about countering Iranian influence in the region. Finally, Japan has decided to dispatch its self-defence troops to the Strait of Hormuz, according to Asahi.

In commodities, oil fell on the China data, with Brent crude easing 0.52% to $59.60 and U.S. crude dropping 0.19% to $53.83. “The (China) GDP print has weighed on short-term sentiment and we have seen regional stock markets and oil contracts edge lower because of that,” said Jeffrey Halley, senior market analyst for Asia Pacific at brokerage OANDA. While crude demand growth tends to track economic growth trends, but Halley said China’s need for oil would not recede any time soon. Underlining that view, Chinese official data released on Friday showed robust refinery throughput in September, rising 9.4% from a year earlier to 56.49 million tonnes, on increases from new refineries and some independent refiners resuming operations after maintenance. Gold dipped to $1,488 per ounce.

Looking at the day ahead, investors will be focused on Fed Vice Chair Clarida’s comments on the economic outlook and monetary policy. As a warm up to that we’ll also hear from the Fed’s Kaplan and George before. The BoE’s Carney and Cunliffe are also due to speak in Washington this evening around the big IMF summit. Meanwhile it’s very quiet for data releases with the September leading index in the US this afternoon the only print of any note. Coca-Cola and Schlumberger release earnings.

Market Snapshot

- S&P 500 futures little changed at 2,996.75

- STOXX Europe 600 down 0.2% to 392.33

- MXAP down 0.2% to 159.69

- MXAPJ down 0.2% to 514.12

- Nikkei up 0.2% to 22,492.68

- Topix down 0.1% to 1,621.99

- Hang Seng Index down 0.5% to 26,719.58

- Shanghai Composite down 1.3% to 2,938.14

- Sensex up 0.7% to 39,328.60

- Australia S&P/ASX 200 down 0.5% to 6,649.68

- Kospi down 0.8% to 2,060.69

- German 10Y yield rose 1.4 bps to -0.394%

- Euro up 0.04% to $1.1130

- Italian 10Y yield fell 3.7 bps to 0.549%

- Spanish 10Y yield rose 1.8 bps to 0.244%

- Brent futures up 0.3% to $60.08/bbl

- Gold spot down 0.2% to $1,488.88

- U.S. Dollar Index little changed at 97.58

Top Overnight News from Bloomberg

- Johnson is battling to sell his new Brexit deal to skeptical members of the U.K. Parliament ahead of a crucial vote on Saturday. The prime minister has no majority in the House of Commons but needs to convince his own Conservatives, as well as opposition politicians, to back the divorce accord he struck with the EU on Thursday. If Johnson secures Parliamentary backing for his Brexit deal with a smooth transition, then interest-rate hikes are on the table for the Bank of England, according to Deputy Governor Dave Ramsden

- China’s economic growth slowed in the third quarter amid weak demand at home and as the trade war with the U.S. drags on exports. Gross domestic product rose 6% in the July-September period from a year ago, the slowest pace since the early 1990s and weaker than the consensus forecast of 6.1%

- Labour leader Jeremy Corbyn called for a second referendum, saying in Brussels that Boris Johnson’s deal — which he described as a “sell-out” — was worse than that put forward by May. Scotland’s first minister, Nicola Sturgeon, said her Scottish Nationalist Party will vote against the deal as well, complaining that it creates too great a separation from the EU

- Turkey agreed to a temporary pause of military operations in Syria that could be extended if Kurdish fighters formerly allied with America leave the border region, U.S. Vice President Mike Pence announced after a hastily arranged visit to Ankara. The “immediate” cease-fire will last 120 hours

- Interest rate cuts are supporting Australia’s economy and housing market, Reserve Bank governor Philip Lowe said. “I don’t think it’s the right assumption to make that we are going to have a lot more work to do to get inflation back to target and growth back to trend,” he said adding negative interest rates are unlikely

- Prime Minister Shinzo Abe’s cabinet on Friday approved draft legislation to impose tougher rules on foreign investment in stocks related to national security despite opposition from market participants

- Mick Mulvaney set out to offer an impassioned defense of President Trump’s dealings with Ukraine, but he may have only made matters worse for his boss — and himself

- The lira jumped to its strongest level in almost two weeks after the U.S. agreed not to impose any further sanctions on Turkey as part of a temporary cease-fire deal in Syria struck between Ankara and Washington on Thursday

Asian equity markets traded cautiously after the rally from the Brexit deal breakthrough petered out and as participants mulled over mixed Chinese data including GDP which printed at its weakest in nearly 3 decades. ASX 200 (-0.5%) underperformed with Consumer Staples and Tech frontrunning the broad declines across its sectors, while Nikkei 225 (+0.2%) edged a fresh YTD high as it benefitted from recent currency outflows as well as reports South Korea is willing to enter discussions to settle bilateral tensions with Japan on forced-labour issues. Elsewhere, Hang Seng (-0.5%) and Shanghai Comp. (-1.3%) were indecisive and eventually deteriorated following a flurry of tier-1 data releases from China which showed its economic growth slowed to the weakest pace since 1992, although Q/Q and YTD GDP figures matched analysts’ forecasts, while Industrial Production surpassed estimates. Finally, 10yr JGBs were relatively flat after a rebound from yesterday’s late selling pressure in which prices briefly tested 154.00 to the downside, while demand subdued as Japanese stocks remained afloat and with today’s BoJ Rinban operations at a relatively tepid JPY 150bln in the long and super-long end.

Top Asian News

- Turkish Markets Rally as Erdogan Clinches Syria Deal With U.S.

- WhatsApp Protests Erupt in Lebanon as Economic Crisis Deepens

Top European News

- BOE’s Ramsden Says Smooth Brexit Puts Rate Hikes on the Table

- French Border Blocked as Catalan Protesters Begin Strike

- LSE CFO to Retire Once Bourse Completes Refinitiv Takeover

- After Hemorrhaging $100 Billion, Europe Stages a Comeback

In FX, the sterling remains relatively strong, but in much more sedate trade awaiting the fate of the latest Brexit deal at the hands of MPs tomorrow, with the Parliamentary vote expected to be very tight. However, despite ongoing DUP opposition and little sign that the coalition party will be won round, Cable is nudging higher within 1.2840-1.2920 confines and Eur/Gbp remains depressed between 0.8660-15 parameters. For the record, option break-even pricing is around 2 big figures and the loftiest since the 2016 EU referendum, though this could be deemed quite conservative given even bigger swings in the Pound seen of late.

- NZD/AUD – It’s been nip and tuck down under for the most part this week, but the Kiwi has overtaken the Aussie in wake of mixed Chinese data overnight, as Nzd/Usd breaches 0.6350 and the Aud/Nzd cross reverses further from post-Aussie labour report peaks just shy of 1.0800 through 1.0750. Nevertheless, Aud/Usd is consolidating gains above 0.6800 amidst general Greenback weakness with the DXY hovering around 97.500 ahead of the final pre-October FOMC Fed speakers and following mostly sub-consensus US data and surveys in the run up.

- EUR/CAD/CHF/JPY – All narrowly mixed against the Buck, as the single currency maintains 1.1100+ status and in bullish mode alongside Cable, eyeing yesterday’s circa 1.1140 high that coincides with the 100 DMA and is close to a Fib retracement level. Meanwhile, the Loonie is sitting tight in a 1.3130-45 band, while the safe-haven Franc and Yen roam either side of 0.9875 and 108.60 respectively.

- NOK/SEK – In contrast to the Antipodean Dollar dovetailing noted above, clear divergence has been more apparent in Scandinavia where Norway’s Crown is extending declines to new record lows vs the Euro and losing more ground relative to its Swedish peer. Thursday’s seemingly poor jobs data from Sweden has been largely shrugged aside due to sub-standard elements of the figures collated, while it remains a close call whether the Riksbank retains its tightening bias and/or the Norges Bank reaffirms and on hold stance after September’s 25 bp hike.

- EM – Although rallies or recoveries against the Dollar are trending across the region, Usd/Try has reversed further than most other pairs (to circa 5.7500 at one stage) on the back of sheer Lira relief that the US has put sanctions on hold in acknowledgement of the 5-day ceasefire in Northern Syria forged with Turkey.

In commodities, crude prices are drifting higher, although there is a lack of fresh fundamental drivers. ING note that factors possibly contributing to yesterday’s WTI (post-DoE) rise were inventory draws across all the other refined products. The key driver behind the draws seen across the products, argues the bank, was seasonal refinery turnarounds, with refinery run rates falling by 2.6 percentage points over the week to average 83.1%, the lowest level since September 2017. Looking ahead, the UK Parliament’s vote on PM Johnson’s new Brexit deal is likely the most notable weekend risk factor, albeit the docket includes a slew of Fed voters on US economy ahead of the Fed blackout period. Elsewhere, in metals, Gold prices have steadily declining on Friday morning, despite lower equities and the downbeat Chinese data. On which note, Copper prices remain under pressure, as data provided further evidence of a slowdown in its biggest market, China. Desks are citing the slowdown as more evidence of the negative effect of the US/China trade war on global growth. However, this week’s constructive tone on the state of US/China trade negotiations from both sides, combined with the agreement on a Brexit deal by the EU and UK has helped to cushion losses. Meanwhile, this week Dalian iron ore futures have suffered from one its largest weekly declines in two months. Analysts point to tightening restrictions on Chinese steel production over air quality issues and, more broadly, the slowing global demand for Chinese steel and iron ore.

US Event Calendar

- Oct. 18-Oct. 21: Monthly Budget Statement, est. $83.0b, prior $119.1b

- 10am: Leading Index, est. 0.0%, prior 0.0%

Central Banks

- 9am: Fed’s Kaplan Speaks in Washington

- 10:05am: Fed’s George Speaks at Fed Energy and Economy Conference

- 11:30am: Fed’s Clarida Speaks on Economy and Policy Outlook

DB’s Jim Reid concludes the overnight wrap

I’m looking after the children on my own tomorrow and I’m trying to assess how keen they’ll be to have the World Cup Rugby on the telly in the background in the morning and the Parliament channel on as their primary entertainment in the afternoon. I’m not sure whether they’ll be more screaming in front of the telly or within it.

Although tomorrow’s U.K. Parliamentary vote is a monumental occasion for the U.K. and Europe, DB have argued this week that the actual signing of the agreement (finalised yesterday) was always going to more important over the medium term than whether it passes tomorrow. We became bullish on the pound after the U.K./Irish meeting last week but this call was at risk if a deal didn’t materialise. It was clearly in the balance until the news yesterday. The reason we think that tomorrow’s vote is less important to the pound than the striking of the deal itself is that all the major UK parties now support either a second referendum which is unlikely to have no deal on the ballot paper (Liberal Democrats, Labour, SNP), or a concrete deal with the EU (Conservatives). See DB’s Oliver Harvey latest piece On Brexit here .

Markets were a bit more nervous than we were yesterday and the initial euphoria that we witnessed as the deal headlines broke all but evaporated as the DUP negative stance quickly became apparent and made the parliamentary math for tomorrow’s vote a lot more difficult. Most respected sources I’ve seen over the last 12 hours suggest Mr Johnson will be 0-20 short with momentum slightly going in his favour as time progresses. He still might have a few rabbits up his sleeve to win friends and foes (workers rights?) over but it’s going to need a Herculean effort to get it over the line. As we said last week, the best case scenario for Mr Johnson is that the EU say it’s this deal or no deal. This would mean that those most opposed to no deal would essentially be voting for such an outcome if they rejected the deal tomorrow. A big irony. However I suspect the EU won’t want to take this hard line option. I suspect they’ll keep it vague about whether they’ll grant an extension or not before the vote to try to encourage the swing voters to back the agreement out of fear they won’t extend. But nothing beyond that. There could also be an amendment voted on that ensures that if the deal fails, the Benn Act is watertight. This might encourage a few of the Tories who recently lost the whip to vote in favour.

The big question though is if the deal is not ratified tomorrow, what happens next. A general election in November appears most likely especially as well sourced journalists suggested yesterday that those desperate for a second referendum have decided not to try to amend the bill tomorrow to attach one. This might suggest they don’t have the votes for it. The PM could request an extension to A50 from the EU and table a motion under the Fixed Term Parliament Act to hold an election in November. If opposition parties refused to vote for an election, he could resign and instruct his cabinet to do the same. The political pressure to hold such an election would be high, as a caretaker government formed under these circumstances would be seen as politically illegitimate. It’s worth noting that the Conservatives have polled better since Johnson became PM, and a snap ComRes poll last night shows that the public supports the deal by a 40% to 31% margin, with 29% of respondents unsure. The initial public reaction to ex-PM May’s deal was relatively negative. Importantly, only one scenario would reintroduce the risk of a no deal Brexit – that of the Conservatives forming a minority government with the support of the Brexit Party/DUP. What will therefore be interesting is the opinion polls over the next few days if he loses the vote. Will he be blamed for not leaving on October 31st and see support leaking to the Brexit Party?

So expect headlines aplenty over the next 24/48 hours. Speaking of headlines it’s worth jumping straight to Asia this morning where we’ve had some important data with China’s Q3 GDP printing at +6.0% yoy a touch below expectations of +6.1% yoy, marking the slowest pace of expansion since the early 1990s. However, in details, the contribution of consumption to GDP growth increased to 60.5% from 55.3% in the previous quarter while investment’s contribution slowed to 19.8% from 25.9%. National Bureau of Statistics spokesman Mao Shengyong said post the release that there is “ample space for monetary policy,” with the recent acceleration in consumer prices largely confined to commodities and especially pork prices –- which should start returning to a “normal” range. There was also hints of some consumption stimulus as they said “there is room and potentials for China to boost auto sales”.

We also got a slew of other economic data for China with September industrial production printing at +5.8% yoy (vs. +4.9% yoy expected), retail sales expanding in line with consensus at +7.8% yoy, while YtD fixed asset investments came in at +5.4% yoy (vs. 5.5% yoy expected). The surveyed jobless rate remained at 5.2%. In other data releases, Japan’s September CPI, core CPI and core-core CPI all printed in line with consensus at +0.2% yoy, +0.3% yoy and +0.5% yoy respectively.

Asian markets are trading largely lower this morning on the weaker Chinese growth data with Chinese bourses leading the declines. The CSI (-0.65% ), Shanghai Comp (-0.59%) and Shenzhen Comp (-0.45%) are all down. The Hang Seng (-0.09%) and Kospi (-0.47%) are also lower while the Nikkei (+0.33%) is up but has erased part of its early gains. Elsewhere, futures on the S&P are down –0.17% while yields on 10y USTs are down -1.4bps.

Meanwhile Sterling is trading c. -0.30% this morning at $1.2853. That follows a 1.88% intraday range yesterday which saw the pound bottom out at $1.275 and top out at $1.299. For context the last time it went above $1.300 was back on May 13. Unsurprisingly there were big swings across other UK assets. For example 10y Gilts traded as high as 0.788% (+7.9bps) before closing -3.6bps lower at 0.677%. Similarly Bunds traded at -0.335% before closing at -0.408% and Treasuries at 1.797% before closing at 1.754%. The Brexit story has certainly made us appreciate how much risk premium there is in Bunds at the moment as they have been very sensitive to this newsflow over the past couple of weeks.

As for equities, last night the S&P 500 ended with a +0.28% gain after paring a big mover higher above 3,000 at the open with health care and industrials leading at the expense of tech. The NASDAQ finished +0.40% and DOW +0.09%. Earnings helped, especially Netflix (+2.47%) and Morgan Stanley (+1.54), though they did both retreat from their pre-open highs, by -7.98% and -3.10% respectively. In Europe the STOXX 600 closed -0.10% after being up as much as +0.86% while the FTSE 100 ended +0.20%. There wasn’t much to report in credit, though oil experienced some volatility after a mixed set of inventories data. Headline crude stockpiles rose 9.3mn barrels, more than forecast, but distillate and gasoline inventories were drawn down by more than expected. Ultimately Brent crude ended 0.81% higher.

Away from Brexit, the data in the US was a mixed bag, with industrial production falling -0.4% in September, worse than expected even with a slight upward revision to the prior months. Headline housing starts were also weaker than forecast, at 1.26mn versus an expected 1.32mn, though the miss was mostly driven by the volatile multi-family home series. The more forward-looking and important series, building permits, rose more than expected at 1.39mn. Elsewhere, the Philadelphia Fed’s business survey fell to 5.6 from 12.0, but it still remains a strong outlier compared to other regional surveys at 58.7 on an ISM-adjusted basis.

The Fedspeak calendar was light, with Chicago’s Evans and Governor Bowman both speaking at “Fed listens” events, but neither shed new light on their policy views. Evans reiterated his dovish rhetoric and his concern over low inflation, while Bowman did not discuss the economic outlook at all. The market continues to almost completely price in a rate cut for the Oct 30 meeting, with an 88% chance currently implied by futures.

In other US policy news, the evolving chances for US sanctions on Turkey caused a roundtrip in the lira. First, it weakened -0.77% after Senator Lindsey Graham announced that he will push for financial sanctions which would bar US residents from buying Turkish assets, including sovereign debt. It then completely reversed to trade +1.24% stronger when the Trump administration announced that it had reached a ceasefire deal to suspend hostilities between Turkey and the Kurds in northern Syria. Later, Senator Graham announced that he would still push “full steam ahead” to pass his sanctions bill, but the lira nevertheless held its gains, ending +1.00% stronger versus the dollar.

Finally to the day ahead, which other than the obvious Brexit developments, will likely to be focused on Fed Vice Chair Clarida’s comments at 4.30pm BST on the economic outlook and monetary policy. As a warm up to that we’ll also hear from the Fed’s Kaplan and George before. The BoE’s Carney and Cunliffe are also due to speak in Washington this evening around the big IMF summit. Meanwhile it’s very quiet for data releases with the September leading index in the US this afternoon the only print of any note. Coca-Cola and Schlumberger release earnings.

Tyler Durden

Fri, 10/18/2019 – 07:40

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com