For The Bulls, It’s Now Or Never

Authored by Lance Roberts via RealInvestmentAdvice.com,

It’s Now Or Never For The Bulls

In April of this year, I wrote an article discussing the 10-reasons the bull market had ended.

“The backdrop of the market currently is vastly different than it was during the ‘taper tantrum’ in 2015-2016, or during the corrections following the end of QE1 and QE2. In those previous cases, the Federal Reserve was directly injecting liquidity and managing expectations of long-term accommodative support. Valuations had been through a fairly significant reversion, and expectations had been extinguished. None of that support exists currently.”

It mostly fell on “deaf ears” as the market rallied back to highs. Since then, the market has continued to “cling” to a “wall of worries” as noted in Tuesday’s missive by Doug Kass:

-

Untenable Debt Loads In The Private And Public Sectors.

-

An Unresolved Trade War With China.

-

The Global Manufacturing Recession Is Seeping Into The Services Sector.

-

The Market Structure Is Frightening.

-

We Are At An All-Time Low In Global Cooperation And Coordination.

-

We Are Already In An “Earnings Recession.”

-

Front Runner Status of Senator Warren (Market Unfriendly)

-

Valuations On Traditional Metrics (e.g., stock capitalizations to GDP) Are Sky High.

-

Few Expect That The Market Can Undergo A Meaningful Drawdown.

-

The Private Equity Market (For Unicorns) Crashes And Burns.

-

WeWork’s Problems Are Contagious

The reason I said “cling,” rather than “climb,” a “Wall of Worries” is that over the last 22-months the market really has not made much progress. With the market only marginally higher than it was in January of 2018, it has been mostly the ability for investors to withstand a heightened level of volatility.

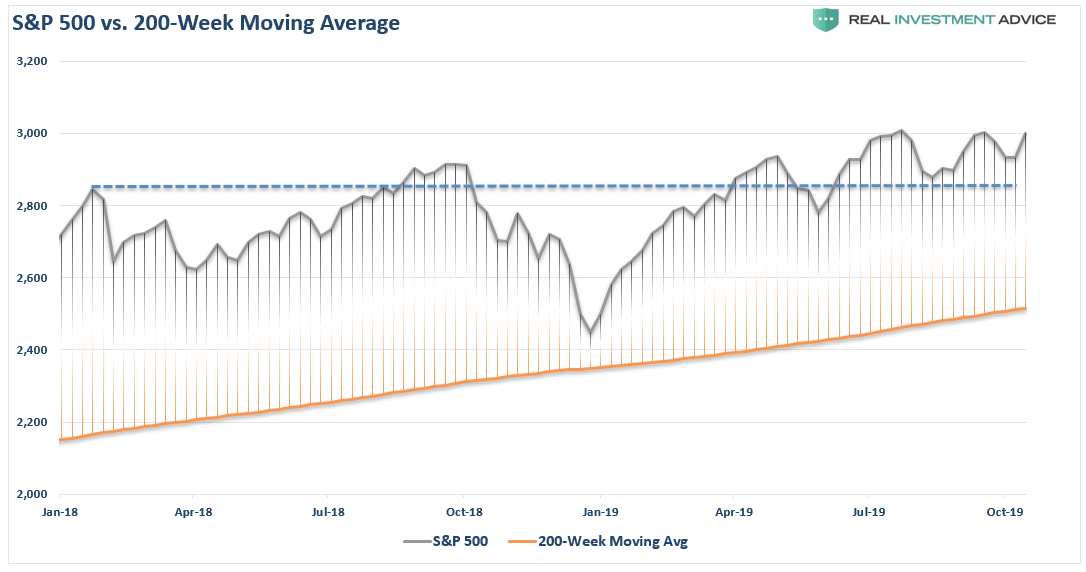

The following is a WEEKLY chart of the S&P 500 as compared to its 4-year (200-week) moving average.

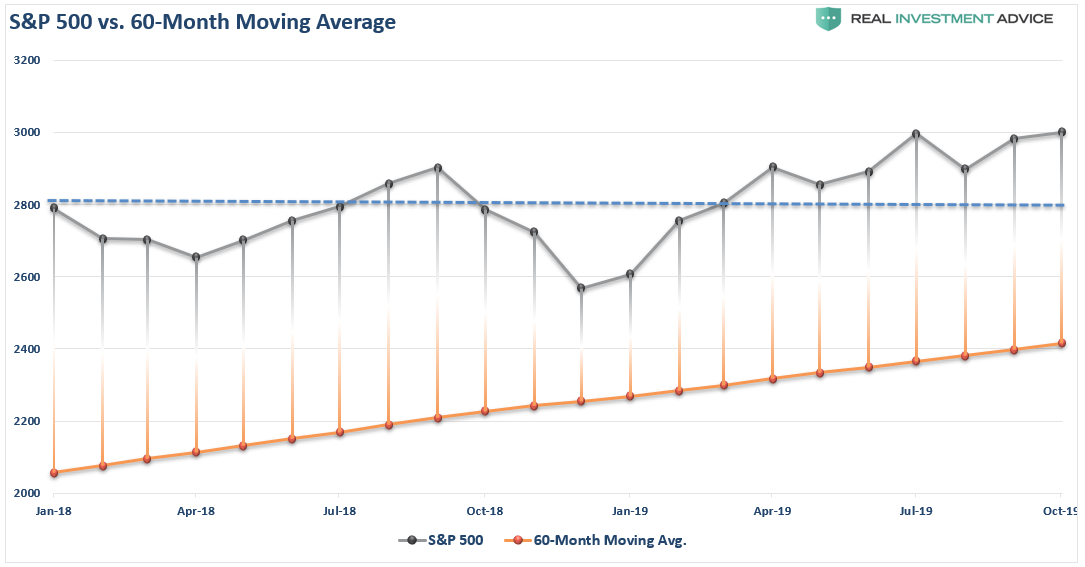

Here is the same chart on a MONTHLY basis as compared to its 5-year moving average.

Note the extremely long time frames of the underlying moving averages. We will revisit these in a moment.

For investors, it is important to understand the “bulls” maintain control of the market narrative for the moment, and, as noted last week, the “bullish wish list” was fulfilled over the last several weeks. To wit:

-

The ECB announced more QE and reduced capital constraints on foreign banks.

-

The Fed also reduced capital requirements on banks; and,

-

Initiated QE of $60 billion in monthly treasury purchases. (But it’s not QE)

-

The Fed is cutting rates as concerns over economic growth remain.

-

A “Brexit Deal” has been reached. (Just don’t read the subtext that says it likely won’t pass Parliament.)

-

Trump, as expected, caved into China and sets up an exit from the “trade deal” nightmare he got himself into.

-

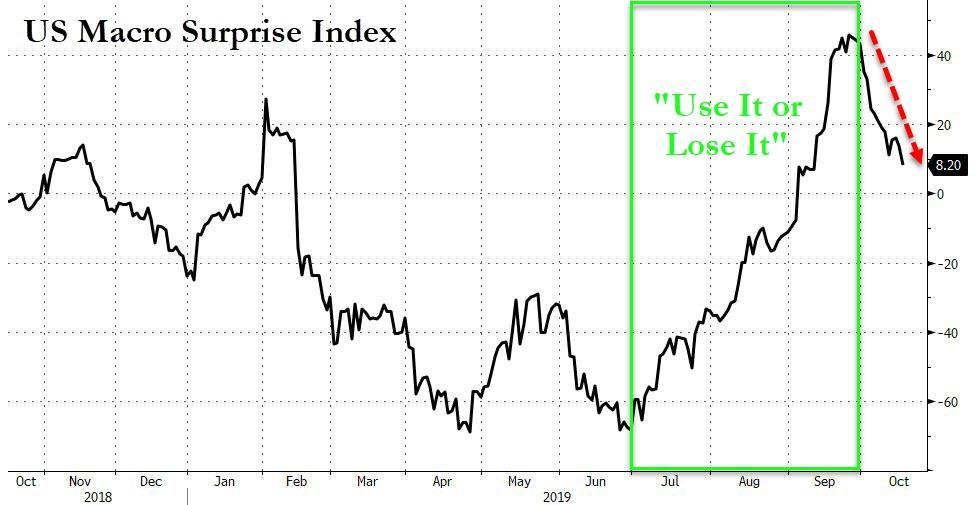

Economic data is improving on a comparative basis in the short-term.

-

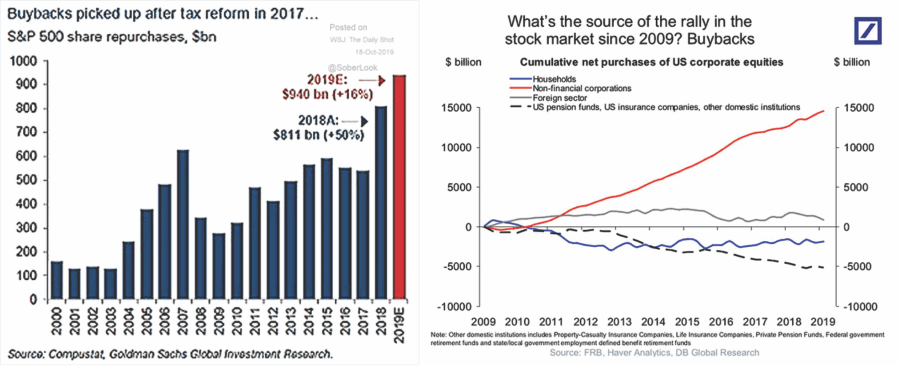

Stock buybacks are running on pace to be another record year. (As noted previously, stock buybacks have accounted for almost 100% of all net purchases over the last couple of years. See chart below.)

If you are a bull, what is there not to love?

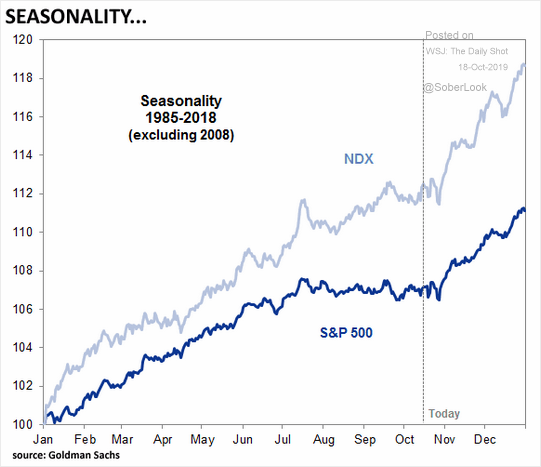

This is a critical point. Given the fact we are now moving into the “seasonally strong” period of the year, the “bulls” clearly have the advantage, for now.

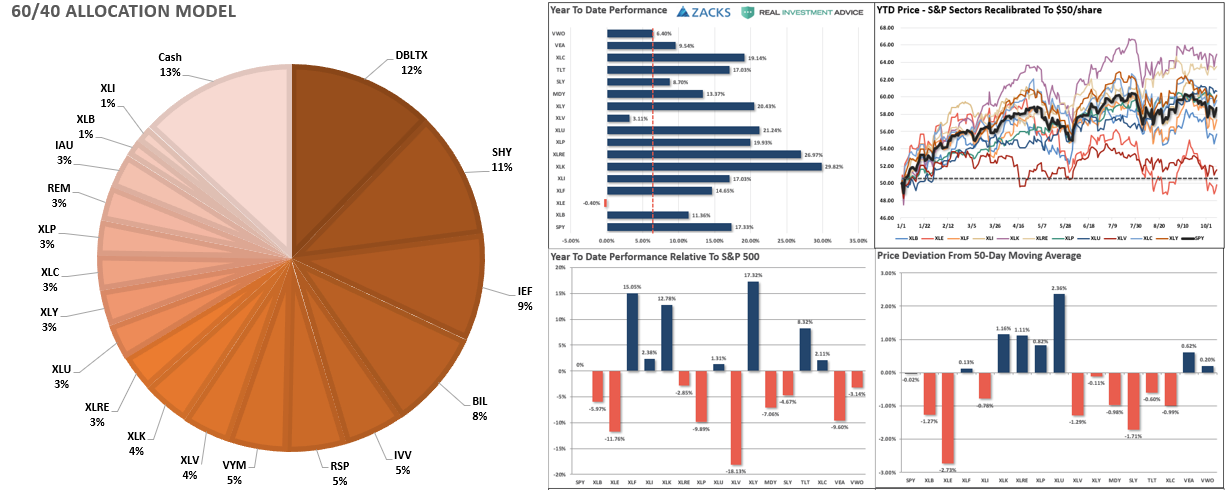

This is why we continue to maintain a long-equity bias in our portfolios currently. We also recently slightly reduced our hedges, along with some of our more defensive positioning. We are still maintaining slightly higher than normal levels of cash.

Note: If you want to track our portfolios “real time,” receive buy/sell alerts on holdings, and have access to all of our data and analysis tools, check out RIAPro.net today for a 30-day FREE Trial.

The Bearish Case Still Has Teeth

“So, IF the “bulls” do indeed have control of the market, then why are allocations still somewhat hedged for risk?”

Great question.

The simple reason we still remain cautious is due to several reasons:

-

Despite the “bullish case” suggesting higher prices into the end of the year, there is still a not-insignificant possibility of failure.

-

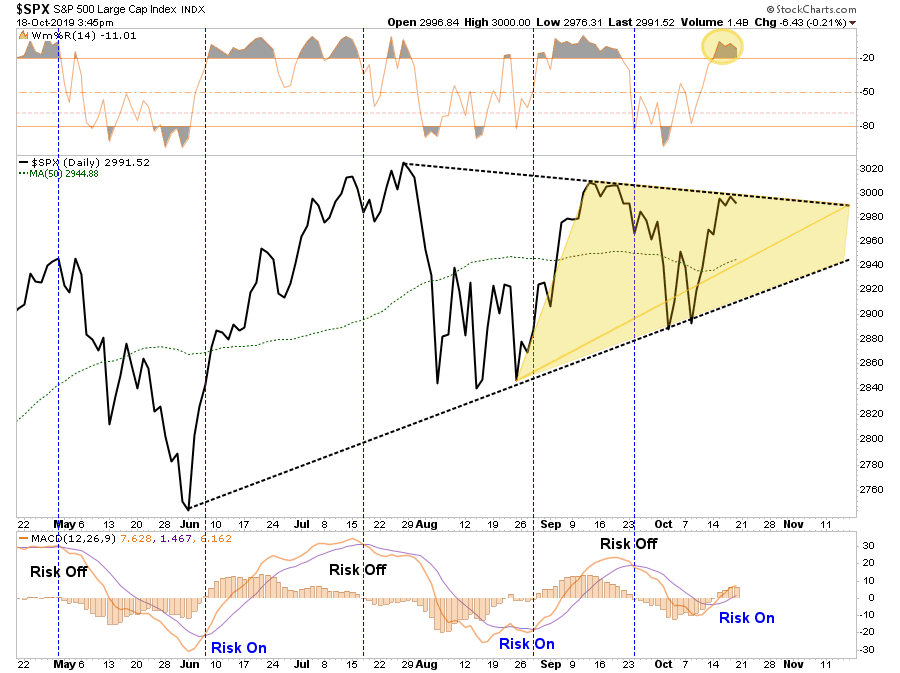

Even with the “bullish backdrop,” the markets have, at least for now, been unable to make, and sustain, new highs. (see chart)

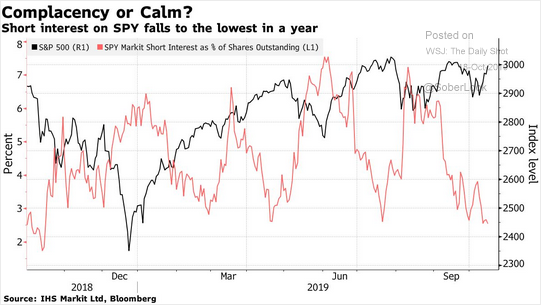

- The is a high level of complacency among speculators (see chart)

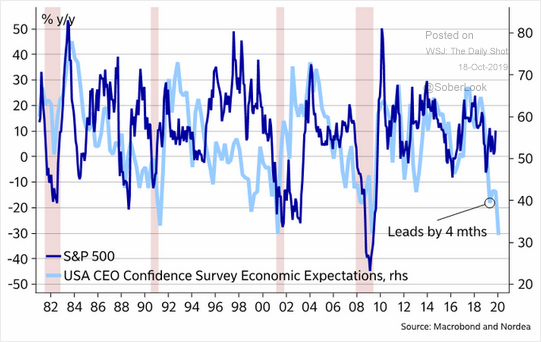

- CEO confidence in economic expectations has fallen sharply to levels which have denoted lower market returns in the past (see chart)

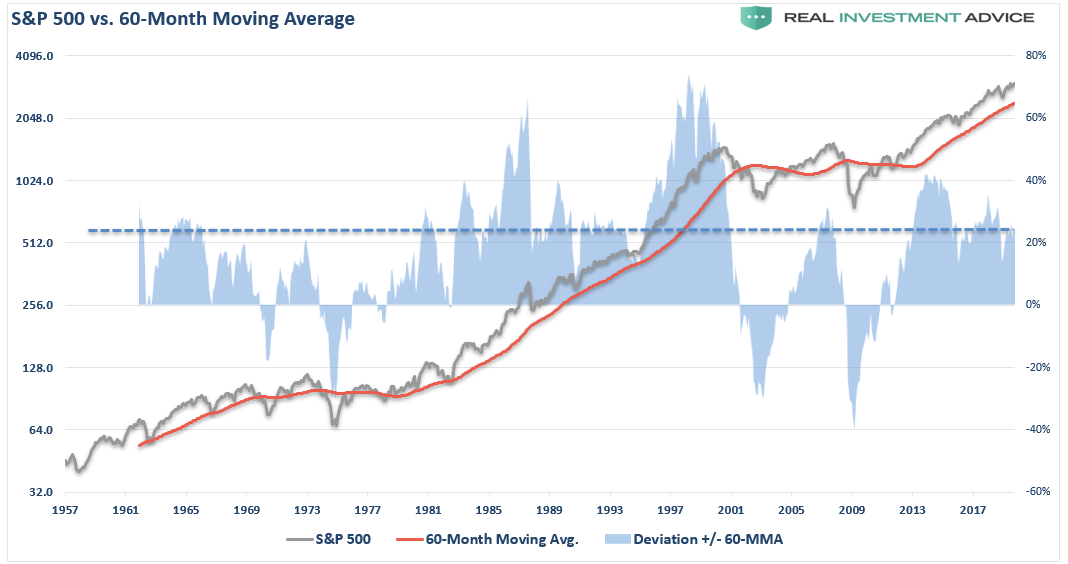

The chart below is the S&P 500 as compared to its 5-year MONTHLY, moving average. With the market currently pushing one of the highest deviations from the long-term average, investors would do well to remember that “reversions to the mean” occur with regularity.

As is always the case, historically speaking, the “bull case” ALWAYS appears to be “correct,” until it isn’t.

Unfortunately, for most investors, by the time they realize that something has going wrong, and they find out just how much “risk” they have layered into their portfolios, it is often too late to do much about it.

This is why “risk management” is always vastly more important than chasing returns.

What To Watch Out For

The one thing about long-term trending bull markets is that they cover up investment mistakes. Overpaying for value, taking on too much risk, leverage, etc. are all things that investors inherently know will have negative outcomes. However, during a bull market, those mistakes are “forgiven” as prices inherently rise. The longer they rise, the more mistakes that investors tend to make as they become assured they are “smarter than the market.”

Eventually, a bear market reveals those mistakes in the most brutal of fashions.

It is often said the religion is found in “foxholes.” It is also found in bear markets where investors begin to “pray” for relief.

Many investors have dismissed the lessons they learned in 2008. There are many more who have never actually seen a “bear market,” and understandably believe the current bull cycle will last indefinitely.

I can assure you it won’t, and “experience” is always a brutal teacher.

As I wrote in “The Exit Problem” last December:

“My job is to participate in the markets while keeping a measured approach to capital preservation. Since it is considered ‘bearish’ to point out the potential ‘risks’ which could lead to rapid capital destruction; then I guess you can call me a ‘bear.’

Just make sure you understand I am still in ‘theater,’ I am just moving much closer to the ‘exit.’”

After having trimmed out some of our gains in our equity holdings throughout the year, and having been a steady buyer of bonds (despite consistent calls for higher rates), we are well positioned to take advantage of a rally to new highs if it occurs.

The cash we hold also protects us against a sudden sharp decline.

For the bulls, it’s now or never to make a final stand.

Just remember, getting back to even is not the same as growing wealth.

Tyler Durden

Sun, 10/20/2019 – 10:30

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com