With 39 Trading Days Left, BofA Tears Up Its Old Forecast And Now Expects A “Beta-Driven” Melt Up

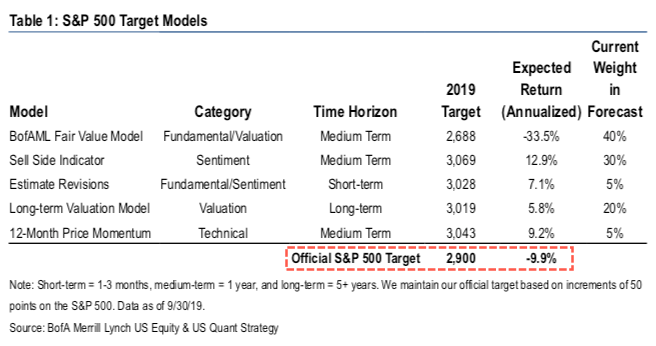

It may seems that it was just yesterday when Bank of America called the market for the year, when the bank’s chief equity strategist Savita Subramanian, said that with the S&P trading at 2,884, she saw the S&P rising no more than a few bps higher, and closing the year at 2,900.

Well, no, it wasn’t yesterday, it was an entire entire month ago, and as we all know, so much can change in a month. Like the Fed can inject about $250 billion in liquidity in the market, inciting a massive risk rally, and forcing those strategists who thought they would have a peaceful end to the year to completely revise their most recent predictions.

That’s precisely what Subramanian has done, and in a note released overnight, the equity strategist no longer expects the S&P to close at 2,900, but rather anticipates a full-blown meltup in the last few remaining days of 2019.

Of course, it wouldn’t look prudent to just throw out some random price target number, nor would it look very professional to admit that the recent move is entirely the Fed’s doing, so instead Subramanian writes that “with 39 more business days in 2019, just 29% of large cap active funds are ahead of their Russell benchmarks.” The implication is clear: anyone who believed BofA’s most recent forecast is now underwater, and has no choice but to scramble to buy, buy, buy. This in turn goalseeks BofA’s new target, which is, well… higher.

Then again, some may see through the thin veneer of such revisionism, so BofA had to throw in a kicker, and it did: the bank now expects value stocks to rip higher, to wit:

The recent market rotation from Momentum into Value should continue if macro data stabilizes – note that valuation dispersion is the highest we have seen since the financial crisis: we are seeing cycle-lows in relative multiples for Value stocks. Moreover, the fact that only 29% of funds are outperforming benchmarks could amplify the rotation if funds chase the Value rally. Active funds are still underweight Value at 0.89x.

Moreover, Subramanian continues, since “Value = Beta right now, and given the hit rate of active funds at this point in time, history suggests we could see a beta-chase into year-end if fund managers essentially “shoot for the moon“.

Of course, they wouldn’t have to “shoot for the moon” if BofA had said on October 2 that the market was going to close at 3,100 or above, which incidentally is a level above any of the “fair values” noted by the bank’s models as of a month ago, but we digress: this is not about being accurate or having credibility, it’s all about covering your ass and justifying a move driven entirely by a massive liquidity injection by the Fed.

The last point of Savita’s “thesis”:

Historically, when 60-80% of active funds were lagging as of October, High Beta stocks led Low Beta stocks by 2.6ppt in Nov-Dec, potentially driven by institutional managers adding Beta exposure into year-end.

In other words, whereas a month ago all the year end S&P “fair values” cited by BofA were below where the market is now, it’s time to throw all that away and come up with an entirely new forecast, one driven purely by FOMO.

There is one small problem: even if one assumes that this time BofA will be right, for most hedge funds it just may be too late to try and scramble to catch up to the market. The reason, as Subramanian points out, is that small cap funds, the best performing size group for the year (52% hit rate), “posted the worst month since June 2017 in October” as only 20% of managers beat the Russell 2000 benchmarks, with all styles underperforming by big margins:

- Core (24% hit rate; -77bps vs. benchmark),

- Growth (17% hit rate, -105 bps),

- Value (17% hit rate, -89bps).

And while mid cap managers fared better, they too underperformed the benchmark by 30bps and posted a 38% hit rate.

Finally, while BofA just may be correct that value stocks will outperform in the last 7 weeks of the year, it is pretty safe to bury one group of investors: momo funds, traditionally the dumbest of smart money, having entered October just modestly down for the year, it is this group that suffered a spectacular meltdown in the last days of October and early November, and at last check, the Pure Momentum index has cratered, plunging to the lowest level in over two years.

Tyler Durden

Tue, 11/05/2019 – 14:50

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com