DiMartino Booth: “Remember, This Is A Confidence Game”

Authored by Danielle DiMartino Booth via QuillIntelligence.com,

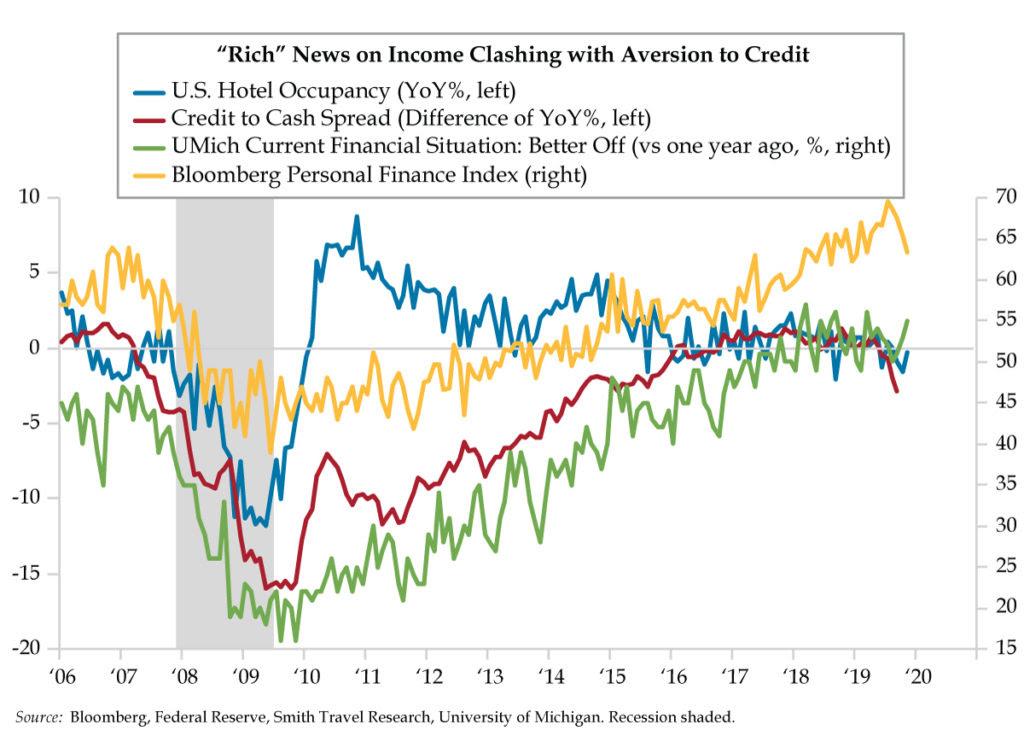

-

In the past two weeks, led by those in the Midwest, renters, part-timers and those making $50,000 or less, the Bloomberg Consumer Comfort Index has declined 4.3 points, its steepest decline since 2011; its Personal Finance Index sunk to a 10-month low despite peak stocks

-

Since June, households have built more cash than credit, a.k.a. de-levered; this coincides with three of the last four months’ declines in revolving credit with the two months through September marking the first back-to-back declines in more than seven years

-

The Bloomberg Consumer Comfort Index’s two-week fall led by those making $50,000 or less occurred alongside two weeks of continuing claims rising over the prior 12 months, the first of the cycle; a third week of deterioration in these two indicators would establish a trend

It helps to be familiar with your source of inspiration. Suffice it to say Hugh Cregg III qualified on this count despite a well-to-do upbringing in San Francisco’s Bay Area and being carted off to a private prep school in New Jersey. As artists tend to, Hugh forged a different path than pedigree suggested of the bookish student athlete who earned a baseball scholarship. Somehow, he ended up working as a truck driver, a carpenter, a short order cook, a partner in a landscaping business and even a street corner singer in Europe before finally making a name for himself. Though it wasn’t his first hit, with a breadth of experience as inspiration, Huey Lewis would one day hit it big with “Workin’ for a Livin’.”

Working men and women have been among the most content Americans in recent years. As we’ve written extensively in recent months, CEO confidence has been cascading downwards while that of the lowest income earners has held at some of the highest levels. In fact, September’s consumer sentiment for the lower third of income earners was stronger than all but one month of that go-go decade – September 1988; only the late-1990s internet bubble was better.

With that as a backdrop, we couldn’t help but notice the high-frequency Bloomberg Consumer Comfort Index sliding by the most in eight years two weeks back. But what’s one week? And then it fell again when reported this past Thursday, reinforcing the 4.3-point two-week decline as the steepest since 2011. But it was the internals that inspired today’s chart. Absolute confidence levels were at one-year lows for those in the Midwest, renters, part-time workers and those with annual incomes under $50,000. More curiously yet, the Bloomberg Personal Finance Index (yellow line) slid to a 10-month low…with stocks at all-time highs.

Any worries surrounding the Bloomberg series were dismissed the minute the University of Michigan’s preliminary November sentiment data hit the wires Friday morning. Instead of falling to 95.0, the index rose to 95.7 from 95.5 in October. Moreover, 55% reported improved financial conditions (green line) prompting survey director Richard Curtin to enthuse, “A higher proportion has been recorded in only four other surveys in over a half century. Moreover, the all-time peak was barely higher at 57%.” Some 43% pointed to income gains while 19% cited lower debt and improved financial assets.

Could the emergent trend come down to those who do and don’t own stocks? It’s no secret that those who make $50,000 or less are not typically among the 52% of Americans who own stocks. This cohort is more likely living paycheck-to-paycheck and making decisions about how to make ends meet as opposed to how to spend their stock riches.

That brings us to the red line above, a pictorial of those who are preoccupied with paying bills via current income or credit. In what may twist the brain, economists like to see this Credit-to-Cash spread stay above the ‘0’ line demarking credit card debt growing faster than cash equivalents.

Remember, this is a confidence game. The more confidence you have in your finances, the more willing you are to go out on a limb and take on credit with the requisite certainty you can pay it back in the future. Starting in 2017, lower income’s happy heyday, leveraging-up was indeed taking place. But the spread moved into negative territory in June as households began to de-lever; since then, the spread has fallen deeper into the red.

Household budget fatigue would theoretically go hand in hand with depressed discretionary spending. We’d venture that more families will be occupying relatives’ guest rooms rather than adjoining hotel rooms this holiday season reflecting the last 18 of 22 weeks that have seen declining year-on-year hotel occupancy. As is the case with household deleveraging, the hotel downturn also started in June. As a rule, “transient,” or consumer, hotel rates are the first to adjust ahead of “group,” rates, as in businesses that book far out in advance.

Rounding out the retrenchment thesis, June also marked the first of the past three-in-four months revolving credit growth – the Federal Reserve’s term for credit cards – has slowed. September also marked the first back-to-back monthly declines we’ve seen in more than seven years.

While we are not yet at the third-week point which establishes a trend, we did note a parallel in this past week’s data. The second straight week of declines in Bloomberg Comfort, led as such by those making $50,000 or less, coincided with the second consecutive week of continuing claims – Americans collecting unemployment insurance – increasing by 2% or more over the prior 12-month period. Yes, we’ll be following both releases closely this Thursday to see if those less comfortable with their finances continues to rise alongside those who’d rather be Workin’ for a Livin’.

Tyler Durden

Mon, 11/11/2019 – 13:30

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com