The Bear Case For Stocks

We’ve outlined pretty much the entire bull case for US/global stocks over the last few days. It comes down to:

- Easing of US-China trade tensions going into an American election year.

- The resultant rebound from lackluster corporate earnings growth this year, led by increasing business confidence and investment.

- Global central banks remaining more inclined to stimulate than constrain their local economies.

- Yes, there will be bumps in the road, and this year’s Q4 rally is stealing some of 2020’s thunder, but history shows US equity markets do tend to add to gains after a strong year.

Today we will play devil’s advocate and consider 3 issues that could derail that upbeat story.

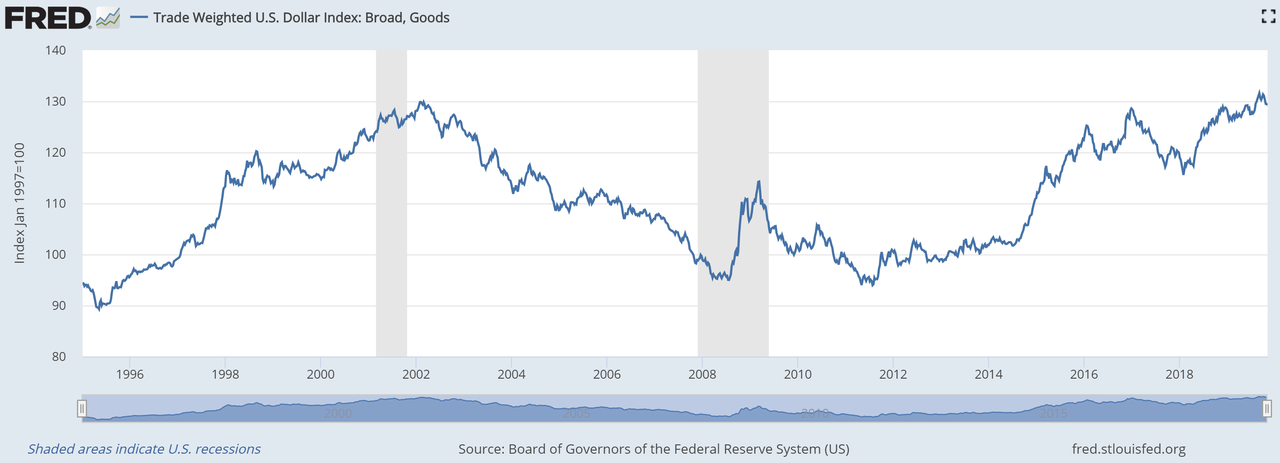

#1: Continued dollar strength.

- The Fed’s Trade Weighted Dollar Index remains stubbornly near all-time highs. We use the Broad/Goods version of the index (chart below) because it’s more inclusive than other measures.

- As much as other capital markets have embraced an optimistic view of the world of late, the dollar’s continued strength does not fit that framework. Not only is the trade-weighted dollar index still strong, but even the narrower DXY Index is still only 1% off its multiyear highs of September 30th.

- A stronger dollar in 2020 would not only cast doubt on the global recovery story, but it would also crimp 2020 US corporate earnings. The S&P 500 derives 38% of its revenues from non-dollar markets.

Bottom line: a weaker dollar is an important (but still missing) link in the current 2020 recovery story. It helps turbo charge global growth by making export-driven economies/companies more profitable and also makes energy (oil is priced in dollars) cheaper for those markets. If the dollar continues to strengthen next year, that will certainly slow any global recovery.

#2: US Corporate leverage in a rising rate environment:

- US corporate debt currently sits at all-time high levels: 46% of GDP.

- However, because interest rates are low and corporate profit margins are high, cash flow coverage ratios remain within normal ranges.

- But if interest rates begin to rise as global economies recover in 2020, then it will be quite a horse race to see if incremental corporate cash flows will grow as quickly as interest expense.

Bottom line: so far the only real sign of trouble here is in the US collateralized loan obligation (CLO) market, where managers bundle subprime loans into risk tranches, but this could spread to traditional corporate debt markets in 2020. The Wall Street Journal had a good piece on the CLO market’s troubles just yesterday (link below), pointing out that these buyers have been over half of the demand for leveraged loans in recent years. Our best source in the leveraged loan market also reports real stress in many credits.

That makes single B and CCC corporate spreads the indicators to watch. Single B spreads are still fairly tight to Treasuries just now (418 basis points, at the lower end of the 1-year range). But as you can see in the 5-year chart below, CCC spreads are certainly moving higher.

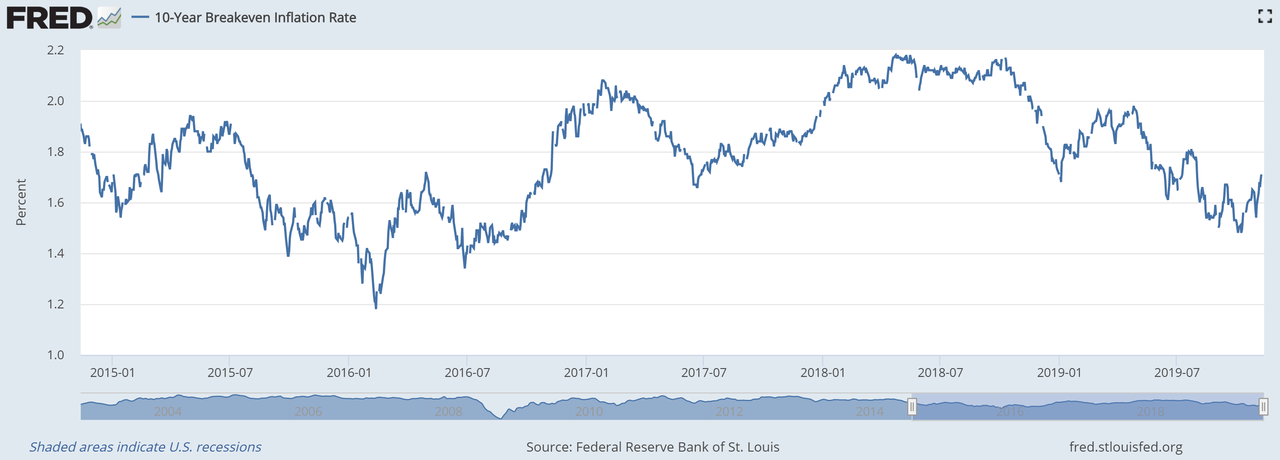

#3) Structural inflation expectations:

- Treasury Inflation Protected securities are another market that hasn’t really signed off on the current bullishness over 2020 economic and business conditions.

- 10-year TIPS spreads are currently 171 basis points, closer to their 1-year lows (148 bp) than their 1-year highs (207 bp).

- Over the last 5 years, the only time TIPS spreads have expressed confidence that expected future inflation similar to the Fed’s target of 2% was in 2018.

- If fixed income markets do fully embrace the notion of a hotter US economy in 2020, then inflation expectations will rise and long term interest rates will follow along.

Here is the chart of the 10-year TIPS inflation breakeven over the last 5 years for reference:

Bottom line: a piece of the bull case relies on a stealth-dove Fed, worried as they are about inflation expectations (Powell highlighted this at his last presser). But in the sort of faster-growth economy that equity markets are increasingly discounting, that could flip to a stealth-hawk Fed fairly quickly.

Final thought: bullish as we may be, we see the merits of each of these points. At the very least, they are three large bricks in the wall of worry markets will have to climb.

Tyler Durden

Thu, 11/14/2019 – 14:55

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com