Platts: 6 Commodity Charts To Watch This Week

Via S&P Global Platts Insight blog,

Nuclear generation in the US and France faces contrasting challenges of power market prices and safety concerns, as this week’s graphics show. Other top trends picked by S&P Global Platts editors include China’s falling LNG imports, stuttering gold prices, refinery margins and coking coal prices.

1. US nuclear sector struggles amid weak power prices…

![]()

What’s happening? Across the US Northeast, largely in states with deregulated power markets, nuclear power plants are being slated for retirement. Their owners are contending with low to flat power demand and depressed wholesale power prices, partly as a result of robust shale gas supply that has lowered gas prices. In deregulated markets, power generators compete to sell electricity in wholesale markets, as opposed to earning a guaranteed rate of return negotiated with utility regulators in regulated markets.

What’s next? S&P Global Platts Analytics estimates that roughly 16 GW of nuclear generation is at risk of retiring before their licenses expire across the US between now and 2025. Assuming this nuclear generation were to be replaced by gas-fired generation, an incremental 2.7 Bcf/d of gas demand from power generation would be required to replace these retiring generators, Platts Analytics estimates.

2. … while France faces winter with a curtailed nuclear fleet

![]()

What’s happening? An earthquake in the Rhone Valley has taken EDF’s huge Cruas nuclear plant (3.66 GW) out of service, forcing the French utility to cut its 2019 nuclear output target, and removing a big chunk of generation capacity at a time when French nuclear availability is normally ramping up to meet rising winter electric heating demand.

What’s next? While EDF plans to bring the Cruas reactors back through the first half of December, it is regulator ASN’s decision to make. With restart clearances prone to bureaucratic delay, the current volatility in prompt prices could intensify as winter deepens. For every degree fall in winter temperatures, French power demand ratchets up 2.2 GW.

3. Europe is LNG market of last resort as China’s appetite wanes…

What’s happening? Chinese imports of LNG continue to trend downward on weaker demand, with the year-on-year decline taking the market by surprise following several years of double-digit growth.

What’s next? A fall in Chinese LNG imports — considered key to maintaining a global LNG market balance — will likely see more cargoes headed for Europe, which acts as a market of last resort for surplus LNG cargoes. This in turn could put more bearish pressure on European gas prices, which are already low due to full storage stocks.

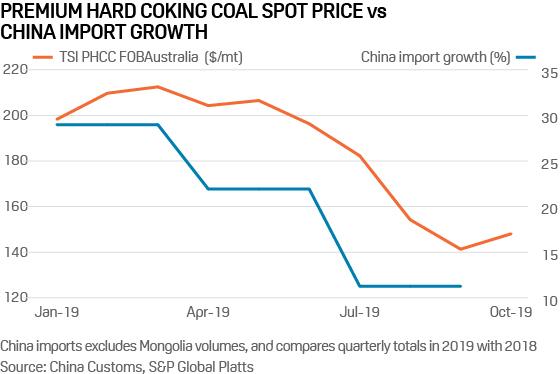

4. … and coking coal pressured by lower Chinese demand

What’s happening? Coking coal benchmark prices have fallen as China’s imports slowed down in the third quarter, and demand for steel in Japan, South Korea, India, Europe and South America was weaker than earlier expected. China’s coking coal imports are expected to rise from 2018, but growth rates through 2019 have fallen as annual quotas get used up.

What’s next? The industry is meeting in Warsaw next week, and US coal miners have already started to slash higher-cost production and shipment targets for the reminder of the year and for 2020. Progress on US and China trade tariffs may help build expectations of stronger global steel demand, supporting raw materials, while the effect of IMO 2020 fuel regulations on shipping costs may affect tradeflow if rates deter longer voyages.

5. Gold loses shine as investors rediscover taste for risk

What’s happening? Gold is under pressure, falling from $1,520/oz to $1,450/oz in recent weeks, dashing talk earlier this year that it had the potential to touch its all-time high of more than $1,900/oz. The drop has occurred even without signs of an early resolution in the US-China and US-EU trade spats. ING Bank strategists report that investors have been liquidating gold as risk appetite returns in the market and demand for safe-haven assets slows down. Exchange-traded fund investors have sold significant positions in gold and physical demand faces pressure due to high prices and a pause by China on gold buying for forex reserves.

What’s next? Gold’s close link to geopolitics makes its fortunes hard to foresee. However, some pundits see a downside trend, due to market resistance to inflated gold prices. “With the Christmas period approaching, there is evidence that gold investors are taking money off the table after a pretty decent job[s] 17% year-to-date gain,” said analyst Ross Norman said in his Metals Daily publication in recent days. “As such, gold looks vulnerable to a deeper short-term correction.”

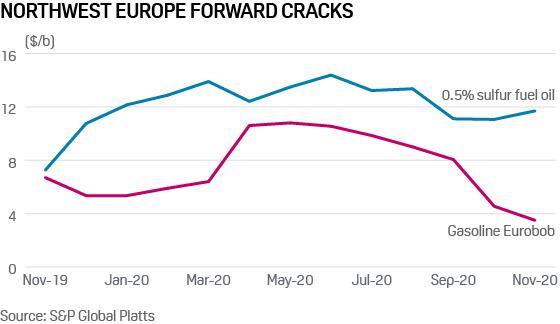

6. Refiners eye lucrative low-sulfur fuel oil ahead of IMO 2020

What’s happening? Rising demand for 0.5% sulfur fuel oil is leading to cracks for the new fuel outstripping those of gasoline. Crack spreads reflect the difference in price between a refined product and crude oil. Current cracks make production of the very low sulfur marine fuel (VLSFO) an attractive proposition for refiners as the IMO 2020 deadline on cleaner shipping fuel approaches. The growing attraction of 0.5% sulfur fuel oil production is causing some refiners to reduce run rates at fluid catalytic cracking units.

What’s next? Historically, a refinery would always look to maximize gasoline at its fluid catalytic cracker, using the vast majority of vacuum gasoil for gasoline cracking. However, sources have noted that the longer than historic maintenance periods across Europe could indicate the intent to limit gasoline production in favor of the new, more attractive 0.5% fuel oil crack.

Tyler Durden

Mon, 11/18/2019 – 13:25

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com