10 Grey Swans For 2020

Authored by Bilal Hafeez via MacroHive.com,

Black swan events are the unknown unknowns that no one can even envisage, let alone predict.

But their close cousin – grey swans – can enter our imaginations. These are low probability, high impact events that few expect. They aren’t even our base cases. But by imagining these risk scenarios, we can at least prepare for them should they erupt. Here are ten to think about for 2020:

1. US Introduces Capital Controls

2. Markets Are Shut For A Long Bank Holiday

3. Euro-area Inflation Surge

4. Japan Intervenes in FX Markets

5. Apple Buys Disney

6. Fed Disintermediates Banks Through Digital Currency

7. Tesla Partners with Hyundai

8. Drone Attacks on US installations in Middle East

9. Virtual Reality (VR) Kills Auto Sector

10. England Win the Euro 2020

Grey Swan #1: US Introduces Capital Controls

While everyone has been talking about trade wars, the next battle may be fought over capital flows. Under President Trump, the US has battled very publicly to advantage US goods in international trade, especially with China. We’ve now got new tariffs being introduced that have the effect of throwing sand into the gears of global trade. But why stop there?

The US’s real strength is its intellectual property and corporate prowess. Foreign companies have forever been trying to acquire US companies to leapfrog an internal development process. Notably, in recent years, China has been an active investor in Silicon Valley and an acquirer of US companies. But we are seeing signs that the US may try to put a stop to that.

The Foreign Investment Risk Review Modernization Act (FIRRMA) was signed into law by President Trump in 2018. It gives the Committee on Foreign Investment in the United States (CFIUS) – the body that approves foreign takeovers of US companies – sweeping new powers. For example, the body can now stop certain real estate transactions and even acquisitions of minority stakes in companies.

Recent deals being blocked include Singapore-based Broadcom acquiring US Qualcomm. And Chinese gaming company Beijing Kunlun Tech had to reverse its purchase of dating app Grindr. All were blocked on national security grounds.

But this could just be the beginning. A lack of progress by the Chinese to open up its markets, a failure to protect US intellectual property in China and any CNY weakness could see the US ratchet up the pressure in 2020. On top of using CFIUS, the US could also delist Chinese companies from US exchanges – currently over 150 companies are listed including Alibaba and PetroChina, and the US could stop US investors buying Chinese securities. Both Peter Navarro, trade advisor to Trump, and Senator Marco Rubio have advocated such moves.

Together these measures would amount to capital controls. So why not go all the way and introduce formal capital controls against all countries? Remember that from after the Second World War until the early 1970s the US had formal capital controls under the Bretton Woods system. You heard it here first.

Market implication: Chinese stocks underperform, US VC markets come under pressure.

Grey Swan #2: Markets Are Shut For A Long Bank Holiday

The festive season seems to arrive sooner every year. And yes, I do realise that each year represents a dwindling percentage of my mortal whole (long may it continue!); but it’s not just me who’s complaining this year. Christmas 2019 has come early for almost everybody who invests in everything – it’s been truly an annus mirabilis.

But as we look forward to 2020, surely we should look back, too. Even in a ‘fake news’, MMT, post-QE financial world, context is a rather important lens when considering long term investment cycles.

Let us just compare 2019 to its predecessor, when according to DB research the percentage of assets with negative total returns in terms of USD was… 93%. So, I’d wait and see where we end 2019. But why just look back one year?

Yes, yes. I agree. The past is a different country; they do things differently there. But we mustn’t forget our history lessons, nor the ghosts of our past. For me, I love a macabre story around this time of year. A creepy tale of horror, a bit of a fright. And sometimes a thing in plain sight is source of such a ghoulish frisson.

When I read the latest sage observations from the CIO of PIMCO (paragons of logic and thoughtful investment) that ‘year-end volatility is possible, not probable’. I know it’s a reasonable and fair assessment. I want a fright for Christmas. Not even statements like ‘volatility is going to treble’, ‘equities are going down 20%’, or ‘PE is a roach motel and going down 25%’ have the slightest effect on me anymore. My fear muscle is jaded. The market has climbed the wall of worry too many times, both with and without ropes. But like the evil in the ghost stories of M.R. James, there is a dark shape at the very corner of my eye.

Much of our enjoyment around 25 December is due to the Bank Holiday(s). We all look forward to them. So I am sure it would come as a huge surprise to practically all market participants that there is something much worse than lower prices. It’s no prices. No market at all. No liquidity. Zero.

Don’t believe it’s possible? Let me just share this with you as a creepy Christmas present, a treat, a gift wrapped in shimmering goodwill.

For one whole week in March of 1933, every single banking transaction in the US was suspended by President Roosevelt issuing Proclamation 2039 in an attempt to stem a tide of bank failures and restore a semblance of confidence in the financial system.

So, the next time somebody asks, ‘what is the worst that could happen?’, remind them of Bank Holidays. Remind them of March 1933. And try not to lose too much sleep, but ask yourself this question: if it can happen for one week, why not one month?

As much as I hate to unwind the thread of this ghostly narrative, I’m afraid I must. Because anybody is entitled to ask: ‘but how?’ In other words, you’ve loaded the weapon, now explain how the trigger gets pulled.

The usual way is to try to imagine a sequence of events that could cause the triggering of unseen market tripwires; classic, logical path dependency. I think the best places to look are, in no particular order:

-

Passive participants becoming forced liquidators following an aligned rapid momentum shift.

-

Funding channels, i.e. CB plumbing springs a leak.

-

Any significantly out-of-sample, rapid rise in inflation in US & Europe (etc., etc.).

We all have our favourites, from China shadow banking to rising credit default, or even collapsing recovery rates. All are valid. And in extremis they might be capable of triggering generalised carnage.

There is another way to explain how the trigger might come to be pulled – but I’ll leave that to another note. It involves understanding quantum phase transitions and complexity. It would be too much to digest here. But don’t be surprised if you get an early Christmas gift of quantum proportions.

Grey Swan #3: Euro-area Inflation Surge

Following the election of left-wingers as its leaders in November 2019, the Social Democratic Party (SDP), could end its coalition with the Christian Democratic Union (CDU). With the economy sliding, waiting out the full Bundestag term until 2021 seems unlikely to arrest the SPD’s own slide in the polls. Germany could go to the polls in 2020.

Just like voters in other countries facing income stagnation and large immigration, those in Germany reject mainstream parties. The main beneficiaries of this anti-establishment feeling however have been the Greens rather than the extreme right. While the latter has made some gains, these have been limited to the states of what was formerly East Germany. As a result, the CDU and Greens could each win about a third of the votes.

The CDU and the Greens would then enter a coalition government as equal partners. If so, the Greens would likely launch a wide-ranging investment program targeting infrastructure and environment. These moves could prove much more popular than commonly assumed as the environment has become the number one concern of German voters. If the coalition was not able to overturn Germany’s constitutional limit on budget deficits, it could rely on issuance of debt not included in the debt break. Germany’s budget balance could swing to for instance a deficit of 1% of GDP in 2020 from a surplus of 1% of GDP in 2019 with larger deficits expected over the medium term.

Emboldened by Germany’s example, France, Italy, Spain, and the more profligate smaller Euro area countries would launch their own fiscal expansions. Without German support, the European Commission would be powerless to stop the breach of fiscal discipline. The average Euro area budget deficit could rise to for instance 3% of GDP in 2020 from less than 1% of GDP in 2019.

In addition 2020 would see a further intensification of union activism. In 2019 labor strikes took place across Europe, but mainly in sectors such as transportation where workers’ ability to paralyze the economy gives them more bargaining power. In 2020, with the economy supported by expansionary fiscal policy, strikes could broaden to the whole European economy and bring about a further acceleration of wage growth.

With less austerity and faster wage growth, the Euro area would boom and inflation would make a come back. For instance, growth could climb to 2.5% in 2020, up from 1% in 2019, and core inflation could move close to 2%, from 1% in 2019. That scenario could see the EUR appreciate to 1.40, the yield curve steepen, and the ECB starts normalizing policy. Euro area equity markets would outperform the US, where a split Congress in the runup to the 2020 elections is unlikely to bring about supportive policies.

Market implication: euro yield curve steepens, euro higher, euro stocks outperform.

Grey Swan #4: Japan Intervenes in FX Markets

Japanese growth is fast losing steam. In 2019, GDP growth was just under 1%, and in 2020 it is projected to fall to a meagre 0.3%.The US-China trade war and associated global decline in manufacturing has clearly impacted Japan. But Japan hiking sales tax in late 2019 hasn’t helped, either. Indeed, previous sale tax hikes in 1997 and 2014 saw significant declines in growth (3.1% to 1.1% in 1997; 2% to 0.4% in 2014). So what’s their plan of action?

The Japanese government has announced a fiscal stimulus package to arrest the decline, but much of it appears to be rehashed versions of existing promises. Perhaps for this reason, markets have shrugged off the announcement.

Meanwhile, the Bank of Japan has hit the limits of monetary policy. They have negative policy rates, they are holding long-term interest down through yield-curve control, they are buying bonds, equities, and real estate, and they altered their inflation target to allow an overshoot.

That leaves Japan with one option: currency intervention, an action it has taken in almost every decade since the beginning of the free float period in the 1970s. Most recently it engaged in its largest intervention ever in 2011. So Japanese policymakers could dust off this well-tested tool and intervene heavily to weaken the yen. This would certainly help boost Japanese exports, which have plunged of late.

Of course, the move may well draw criticism from other countries, notably from President Trump. But with the US failing to reward Japan many additional benefits for being conciliatory, Japan may be willing to take a more aggressive path. Moreover, the US needs a reliable ally in its attempts to contain China.

Get ready for the return of the BoJ in FX markets.

Market implication: USD/JPY rises

Grey Swan #5: Apple buys Disney

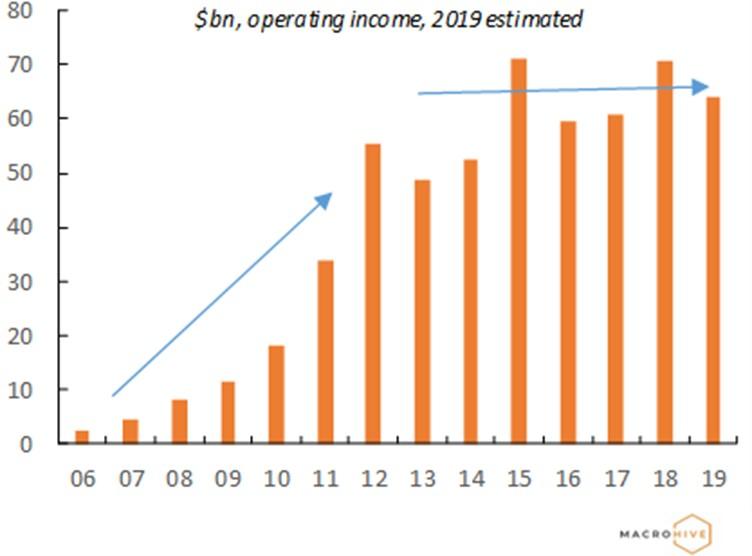

Apple’s earnings have been stagnating in recent years (Chart 1). They are reliant on iPhone sales and upgrades in a maturing smartphone market, and a slowdown in China hasn’t helped. It’s no wonder Apple has focused on expanding its Services and Wearables, Home and Accessories revenues. The trouble is that this will take time and comes with risks.

The clearest case of this has been Apple’s continued forays into TV – whether as a platform (Apple TV), or more recently into content (Apple TV+). Its strategy on the content side was to work with well-known actors and directors to produce a small set of high-quality shows that would signal Apple’s intent. The trouble is that rival streaming services such as Netflix and Disney+ already have a comparable quality; but they also have the quantity.

While Apple has famously been reluctant to make large acquisitions, perhaps 2020 could see them lose patience and take that path instead. And what better target than Disney? The financials could work. Apple’s market cap of $1.2 trillion dwarves that of Disney ($265bn). In fact, Apple has over $200bn in cash on its balance sheet, which alone could almost fund the purchase. The acquisition would give a large library of high-quality content including the Marvel, Star Wars, and Pixar properties. It would also give Apple another entry point into the Chinese consumer market.

Chart 1: Apple Earnings are Stagnating

Source: Macro Hive, Apple

We should also remember that Apple founder Steve Jobs was the majority shareholder of Pixar, which was later acquired by Disney. That resulted in Jobs becoming Disney’s largest shareholder. And until recently, Disney’s CEO, Bob Iger, was on the board of Apple. He stepped down just as Apple was launching a TV streaming product. In fact, Iger writes in his autobiography that ‘if Steve were still alive, we would have combined our companies, or at least discussed the possibility very seriously.’

And if the above arguments are not enough, was it a coincidence that both Apple and Disney ended their streaming service products with a plus: Apple TV+ and Disney+?!

Market implication: Disney shares would rise

Grey Swan #6: Fed Disintermediates Banks Through Digital Currency

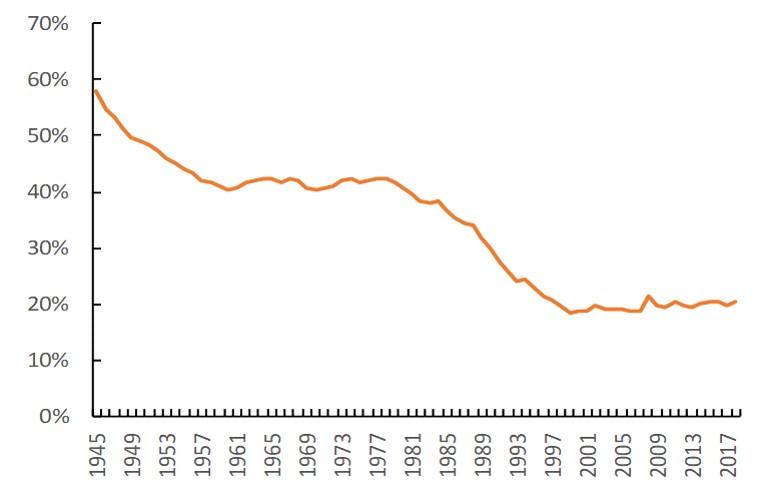

The financialization of the US economy, which started in the early 1980s, massively increased the size of the financial sector relative to the size of the banking industry upon which it depends for funding/passing liquidity from the Fed.

The first cracks in the credit/money transmission mechanism already showed up in the late 1980s with the S&L crisis. The Basel I banking regulations, which came as a response to that crisis, were to severely restrict the use of depository institutions’ balance sheets. The problem was that the financial sector kept growing and needed financing so the shadow banking system (off-balance sheet financing) sprang up in the mid-1990s and quickly overtook traditional bank financing. Basel II, which was first enacted in 2004, eventually contributed to putting a spectacular end to this activity with the crisis of 2008.

Chart 2: Banks as Share of Financial Sector (ex Fed)

Source: Fed Flow of Funds Accounts, BeyondOverton

The total assets of depository institutions now comprise about 20% of total assets of the US financial sector, which is half of what it was before the 1980s (Chart 1). On top of that, a side effect of Basel III over-reach in response to the 2008 financial crisis is further restricting banks’ ability to put their balance sheets to use for the economy as a whole.

The bottom line is that the credit transmission mechanism is even more clogged up now than it has been at any point in the past. That is becoming obvious with repo rates staying elevated despite plentiful Fed liquidity: banks cannot expand their balance sheet after being placed in regulatory fetters by Basel III.

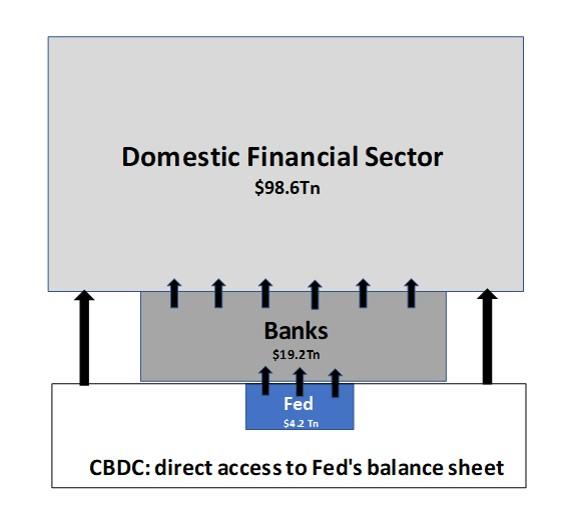

Figure 1

It’s not negative rates or fintech that the banks should be scared of; it’s what comes after.

The 2008 financial crisis was ultimately triggered by a broker-dealer which had no access to the Fed’s balance sheet for funding. The next financial crisis is likely to be similar but probably triggered by a financial institution higher up the inverted pyramid above (Chart 2). This could be an ETF or passive fund provider, for example. But the curve ball here is what is going to happen after the crisis. These events will force the Fed to open up its balance sheet to the whole economy, eventually even to retail through central bank digital currency (CBDC), thus overstepping the banking industry.

Losing their power of money creation may not provide the death knell for the banking industry, but it would be such a massive hit to their model that they may continue to exist only as mere ‘utilities’.

Market implications: US financials underperform

Grey Swan #7: Tesla Partners with Hyundai

The global auto industry is in the doldrums. Chinese growth is weaker and the shift towards electric cars is upending the traditional industry order. European manufacturers – notably German automakers like BMW and Volkswagen – are adapting their model ranges, while Japanese automakers like Toyota are already well advanced in their transition. Tesla, of course, is leading the charge on the US side.

The obvious laggard is Korean automaker Hyundai. Its valuations are among the lowest of the major manufacturers (Chart 1), and investors are clearly questioning the company’s long-term future. Therefore, it may need to find a partner. And fast. But what could it offer? Well, for a start its long experience in manufacturing and its healthy cashflows.

Meanwhile, the auto company that exemplifies the future, Tesla, has the mirror image of Hyundai’s problems. Investors love the vision and value the company at close to ten times book value, but Tesla struggles with production and cashflows. So perhaps a marriage made in heaven would be Tesla partnering with Hyundai.

Chart 3: Poor Valuation of Hyundai

Source: Macro Hive, Reuters

Admittedly, this could be an outlandish call – there’s been no indication from either side of any interest. But with Hyundai struggling to gain traction in the luxury car market and Tesla’s well-known cashflow issues, you never know.

Market implication: Hyundai and Tesla stock rises

Grey Swan #8: Drone Attacks on US installations in Middle East

The unmanned warfare capabilities of insurgents in the Middle East have increased markedly over the past few years:

-

During the battle against ISIS in Mosul in 2016, insurgents were able to use hobbyist drones carrying bomblets to disable Abrams tanks.

-

For the past 2 years, Houthi rebels in Yemen have been using suicide drones to attack UAE and Saudi Patriot missile batteries.

-

In January 2018, Russia reported an attack by a swarm of 13 improvised drones on its Syrian airbase of Tartus.

-

In December 2018, the US military reported than one of its Afghan bases was under regular observation by insurgent drones.

-

And in addition, the Iranian navy is believed to have developed unmanned fast speed boats for asymmetric naval warfare.

Unmanned warfare arguably reached a new level of threat with the September attack on Saudi oil facilities. The attack shattered the myth of impregnable air defence systems, no matter how costly or sophisticated. Saudi Arabia, after all, has access to the most advanced US military technology as well as to US intelligence and surveillance support.

But in fact, the sophisticated weaponry that advanced military powers typically deploy is largely helpless when it comes to very large numbers of unsophisticated, low cost weapons such as drones. In response, the US and other militaries are scrambling to develop counter measures. But these will take time to prepare and subsequently deploy.

Meanwhile, further high visibility targets in the Middle East remain vulnerable in 2020. The likely sponsor of these attacks, Iran, is unlikely to want an open conflict with the US; rather it will wish to demonstrate its retaliation capacity. This suggests that the most exposed targets could be the economic or military assets of US allies or non-military US assets as opposed to the US military itself. For instance, US Navy supply ships crewed by civilians and bringing supplies to the US aircraft carrier strike force deployed in the region could find themselves the target of swarms of unmanned high-speed boats and drones.

Markets quickly recovered from the September attack on Saudi facilities. The price of oil is now lower than before the September attack. But a new, high-visibility drone attack in the Middle East could see more oil supply risk priced in. It could also lead to a rethink of US military spending priorities as drones are changing the cost benefit analysis of traditional military hardware such as aircraft carriers and fighter jets.

Market implication: oil prices move higher

Grey Swan #9: Virtual Reality Kills Auto Sector

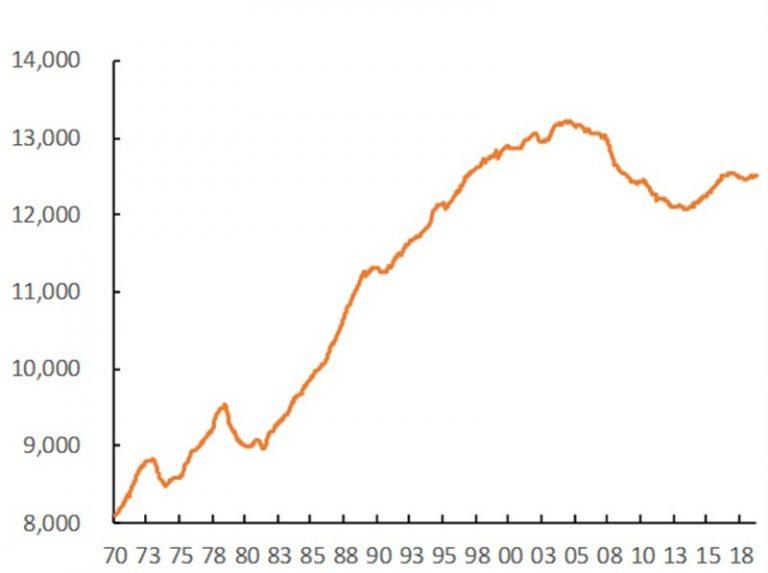

The history of humankind is one of gradually reducing mobility. We generally travel for three reasons: resources, work, and entertainment. And with advances in technology, the need to travel for each of these decreases. As we start to move into the digital medium through VR, the need to travel may completely disappear. With VR on the cusp of mass adoption, betting on the autonomous car – whether electric vehicles (EV) or solar powered – to be the next ‘big thing’ in mobility may not be the smartest idea.

-

We stopped travelling for resources after the Agricultural Revolution: when we first acquired a surplus of resources required survival. We moved from hunter-gathering to a more sedentary lifestyle.

-

The Industrial Revolution instigated a widespread need and ability to travel for work. But that need probably reached a peak sometime after WW2.

-

Mobility for entertainment picked up thereafter, but probably reached a peak in 2007 with the invention of the smartphone and the dawning of the Digital Society.

Chart 4: US Vehicle Miles Travelled Per Capita

Source: FRED

The wide adoption of VR will put the final nail in the coffin of human mobility. Until just a few years ago, at least we used to go ‘shopping for resources’ to our corner grocery store. Now, Amazon and a bunch of other companies bring food and necessities to our doorstep. Travelling for work is also decreasing as internet/network connectivity improves. VR brings the decline of ‘mobility for entertainment’: the need to go to a concert, the movies, etc., or even travelling across the world on vacation, is reduced.

It’s not the EV that will bring down the auto industry, but VR.

It’s only a question of how long it takes for ‘haptics’ to become more sophisticated. People will not, of course, stop travelling completely, but physical mobility will be confined to either a thing of absolute necessity or one of luxury. As such, the auto industry may not disappear, but looks likely to be pushed into the niche corner of luxury travel or transporting discretionary physical goods.

Market implication: global autos underperform

Grey Swan #10: England Win the Euro 2020

England reached the semi-finals of the Football World Cup in 2018. They reached the final of the Rugby World Cup in 2019. And they won the Cricket World Cup in 2019. Notice a pattern? I do, and I think the 2020 European Football Championships could be the next tournament for England to win.

The team topped their qualifying group to enter the tournament and scored the most goals per match of any group (almost five on average). Betting markets have England as favourites to win followed by some mix of Belgium, France, Spain, and the Netherlands.

The England squad is also unusually strong. ESPN recently released their rankings of the world’s best players by position. English players Trent Alexander-Arnold and Raheem Sterling were ranked world number one for the right back and wing positions, respectively. Meanwhile, Harry Kane was ranked as the second-best striker (after Sergio Aguero). And the estimated market value of the England squad at EUR1.25bn is the highest in the world (followed by Spain and France).

So, don’t let the haters talk England down. In 2020, football will be coming home.

Tyler Durden

Mon, 12/09/2019 – 20:20

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com