PBOC Has Explaining To Do With Mysterious Yuan Data

Tyler Durden

Wed, 12/16/2020 – 19:10

By Ye Xie, Bloomberg macro commentator and analyst

Beijing has avoided being named a currency manipulator by the Trump administration. But the conclusion comes with a big yellow flag that may come back to haunt China.

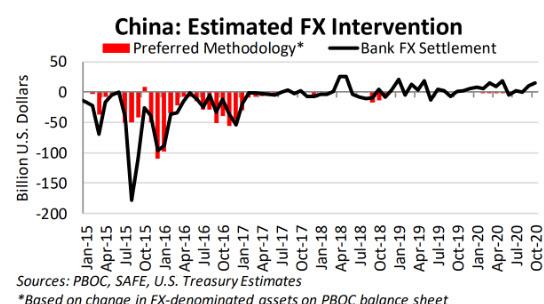

The U.S. Treasury Department on Wednesday kept China on the watch list in the last currency report of the Trump administration, while slapping the manipulator tag on Vietnam and Switzerland. It urged Beijing to “improve transparency” in its currency management – in particular the role state-owned banks play in the foreign exchange market. It noted state-owned banks have sold the yuan, even as the PBOC appears to have refrained from intervening.

The Treasury pointed out that China’s balance-of-payments number doesn’t seem to add up. China’s goods and service surplus surged to a record $132 billion in the second quarter, and the country also attracted stock and bond inflows. But its foreign reserves added only $18 billion during the period.

“While intervention proxies do not provide definitive evidence that the PBOC intervened in foreign exchange markets over the review period, this issue warrants further investigation,” said the report. “In particular, the small scale of foreign reserve accumulation relative to China’s substantial trade and portfolio inflows in the second quarter of 2020, coupled with the RMB’s relative stability over the same time period, raises concerns.”

It’s not just the Trump administration. The apparent mismatch also caught the eye of Brad Setser, a senior fellow at the Council on Foreign Relations, who was tapped to work on Joe Biden’s transition team last month.

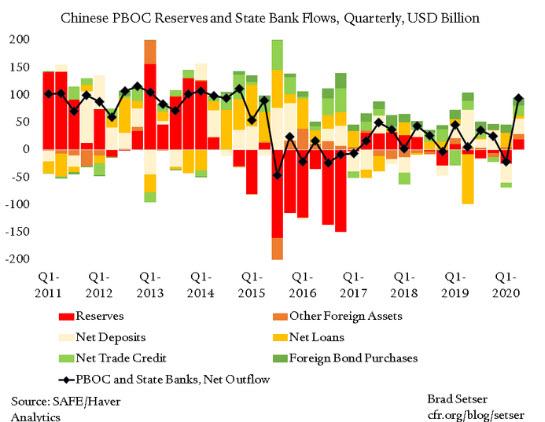

In a report on the CFR website in September, Setser noted that the pace of foreign asset accumulation of China’s state banking system increased “dramatically” in the second quarter.

“The signs of possible hidden intervention are still mostly whispers that speak most loudly only to those who have spent a long time with the data,” Setser wrote. “But if current trends continue, I would expect that they will start to shout when the data for the full year becomes available – as the both the rising Chinese surplus and ongoing bond inflows will raise the size of the offsetting outflow to a level that is going to be hard to hide.”

To be sure, there may be some other explanation for the balance-of-payment puzzle. For instance, Chinese exporters may have parked their dollar revenue overseas, so not all of the trade surplus translates into foreign-currency inflows. The so-called “errors and omissions” also point to capital flight from illegal channels, offsetting the trade surplus.

But the bottom line is that “China’s balance of payments data raise more questions than answers at the moment,” as Mark Williams of Capital Economics puts it. There needs to be a bit more transparency on state banks’ activities in the currency market. On that point, the Trump administration may have a valid argument.

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com