Powell Is Wrong. More Stimulus Won’t Create Employment

Authored by Lance Roberts via RealInvestmentAdvice.com,

As discussed in Friday’s #Macroview, stimulus, mainly when it comes from debt, does not create organic economic growth. In the second part of this analysis, we delve into why Powell is wrong when he says more stimulus will solve the employment problem.

Let’s start with the two most essential snippets from Fed Chair Jerome Powell’s speech last week:

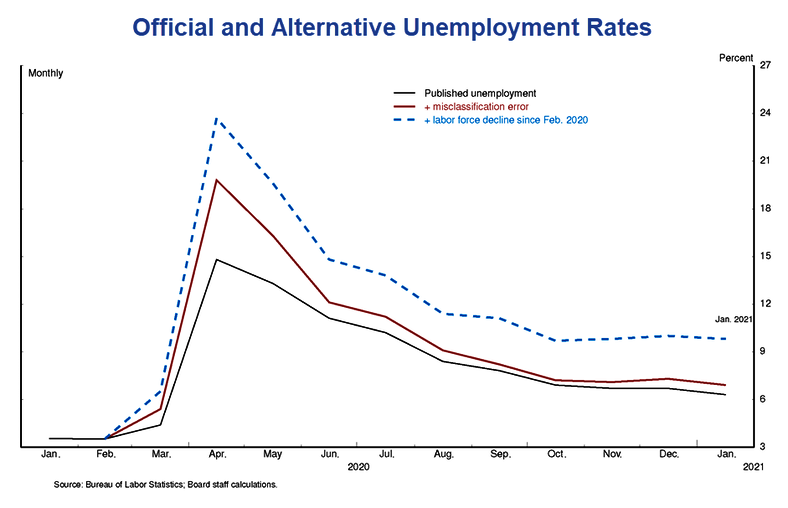

“Correcting this misclassification and counting those who have left the labor force since last February as unemployed would boost the unemployment rate to close to 10 percent in January.”

“It will require a society-wide commitment, with contributions from across government and the private sector.”

I agree with his first point. If you account for those no longer counted as part of the labor force, the real unemployment rate (more commonly known as the U-6 rate) is near 10%.

However, where I disagree, as we exposed in part one of this discussion, monetary and fiscal supports when they are non-productive, do not create the confidence required for economic growth.

The Confidence Problem

To understand why confidence is necessary, we need to go back to 2010 when then-Fed Chairman Ben Bernanke revealed the Fed’s “Third Mandate.” To wit:

“This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose and long-term interest rates fell when investors began to anticipate the most recent action. Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending.”

For the Fed, “confidence” is the key to economic growth, given the economy is roughly 70% comprised of personal consumption. Unfortunately, the Fed believed inflating asset prices would “trickle-down” to the rest of the economy. Such would lead to more consumption and economic growth.

That didn’t occur.

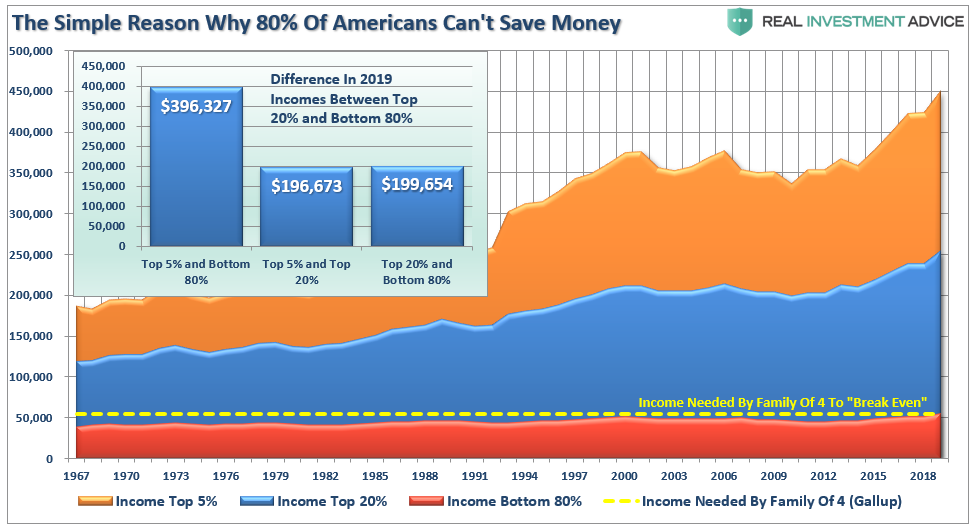

The Rich Got Richer

Confidence is about an individual being able to sustain their standard of living. Unfortunately, as we addressed previously, the differential between incomes and maintaining a standard of living has not been sufficient.

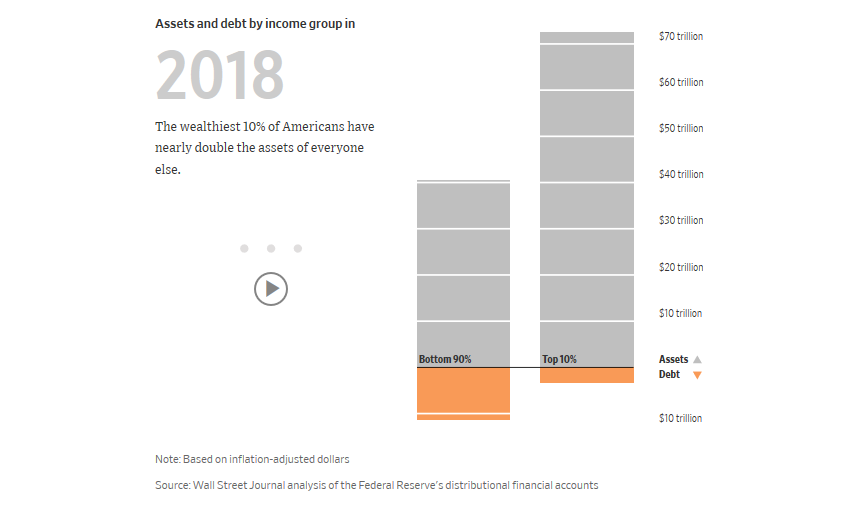

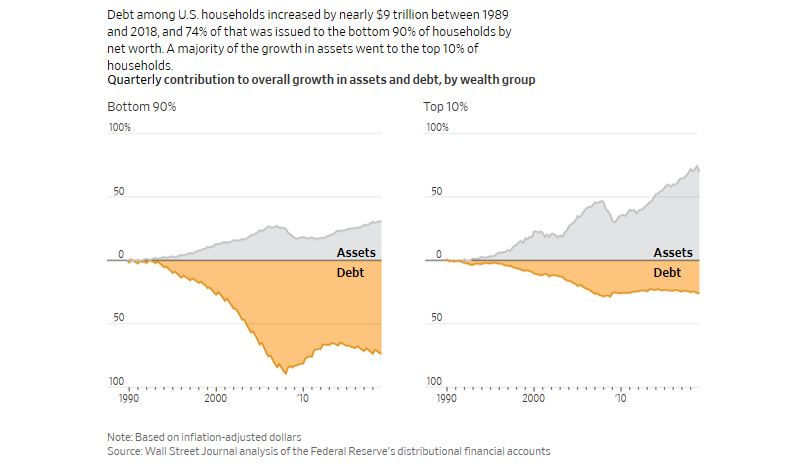

Unless, of course, you are in the top 20% of the economy, where there is plenty of disposable income to invest into the stock market. Given the Fed’s ongoing accommodation over the last decade, the “wealth gap” between the top 10% of the economy owns nearly 90% of the stock market, and the rest has exploded.

Such was a point we noted in our previous report entitled “The Fed’s Only Choice.”

“The median net worth of households in the middle 20% of income rose 4% in inflation-adjusted terms to $81,900 between 1989 and 2016, the latest available data. For households in the top 20%, median net worth more than doubled to $811,860. And for the top 1%, the increase was 178% to $11,206,000.” – WSJ

“Put differently, the value of assets for all U.S. households increased from 1989 through 2016 by an inflation-adjusted $58 trillion. A full 33% of that gain—$19 trillion—went to the wealthiest 1%, according to a Journal analysis of Fed data.”

The Importance Of Consumer Confidence

Importantly, this all circles back to confidence. Economic growth is dependent on confidence.

- Individuals need confidence that a regular paycheck will allow them to consume as needed to support their families.

- Businesses, primarily small business owners, need confidence that consumption (i.e., sales) will remain at levels to sustain their business and generate a profit.

These two dependencies are crucial to the economy. If consumers aren’t confident in their income, they cut back on spending. When consumers cut back spending, business owners become concerned about demand. Therefore, they make decisions to curtail employment, wages, production, investment, and capital expenditures.

The risk was well explained by Treasury&Risk previously:

“It is hard to overstate the degree to which psychology drives an economy’s shift to deflation. When the prevailing economic mood in a nation changes from optimism to pessimism, participants change. Creditors, debtors, investors, producers, and consumers all change their primary orientation from expansion to conservation.

Creditors become more conservative, and slow their lending.

Potential debtors become more conservative, and borrow less or not at all.

Investors become more conservative, they commit less money to debt investments.

Producers become more conservative and reduce expansion plans.

Consumers become more conservative, and save more and spend less.

These behaviors reduce the velocity of money, which puts downward pressure on prices. Money velocity has already been slowing for years, a classic warning sign that deflation is impending. Now, thanks to the virus-related lockdowns, money velocity has begun to collapse. As widespread pessimism takes hold, expect it to fall even further.”

Such is why Powell is incorrect in his views on how to “fix” the economy. Such should be apparent after a decade of monetary policy not working. Artificial stimulus payments, and ongoing monetary accommodations that only benefit the wealthy, do not improve confidence.

Jobs do.

Consumer Confidence In The Economy Declines

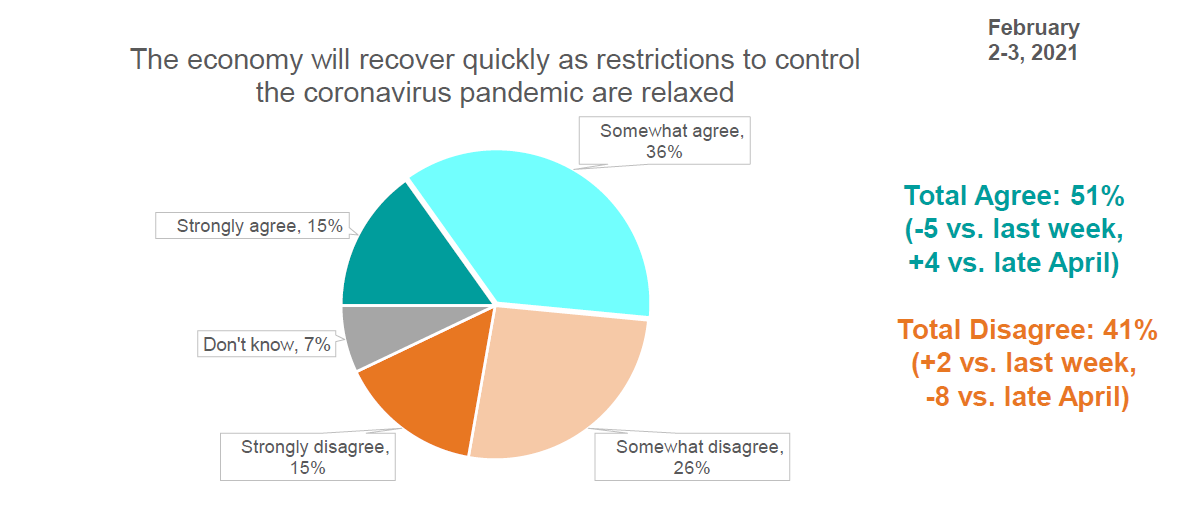

How do we know such is the case? Because after two massive stimulus packages, with a third on the way, consumer confidence in the economy has weakened. A recent Ipsos Poll of Americans showed:

“Fewer Americans this week believe that the economy will pick up quickly once pandemic restrictions are relaxed. The percentage who agree fell 5 points from last week to 51% now.”

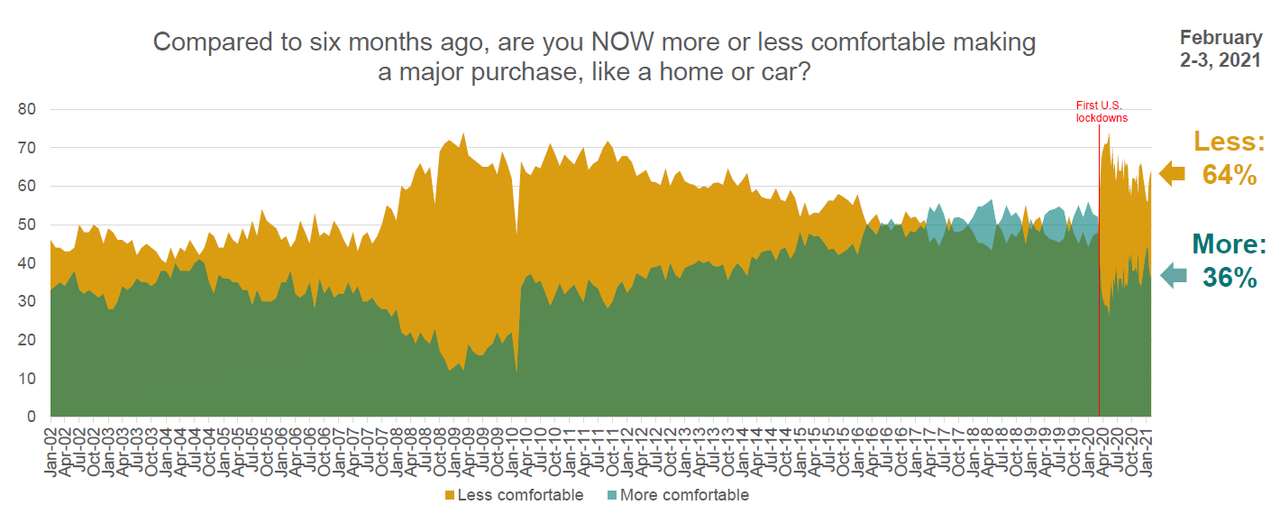

“Purchasing confidence for both major items and other household items is still weak relative to the more confident readings of early to mid-January.”

This poll’s importance is that despite stimulus payments, a new Administration, a vaccine, and a surging stock market, confidence has deteriorated.

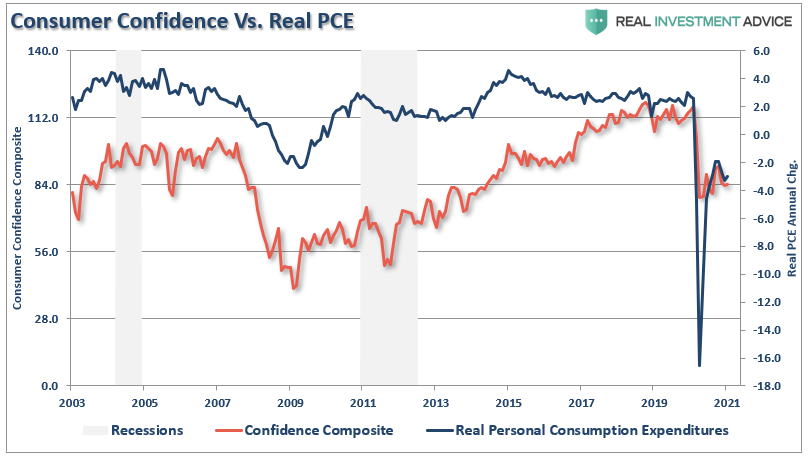

We also see the same problem in our composite consumer confidence index verse real personal consumption expenditures. (PCE comprises roughly 70% of the GDP calculation.)

Not surprisingly, the lack of confidence is rolling over into small businesses as well.

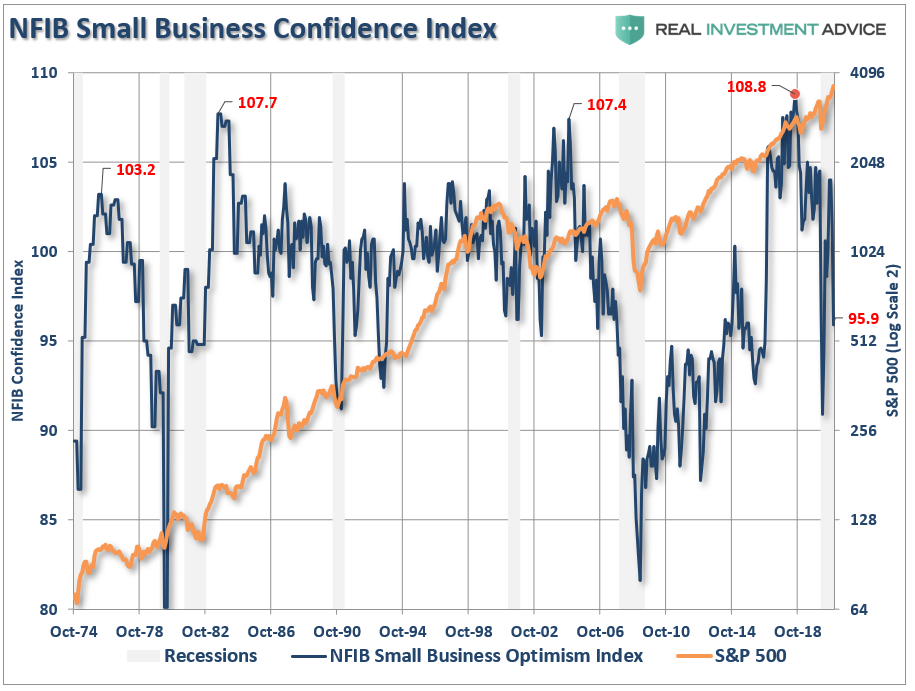

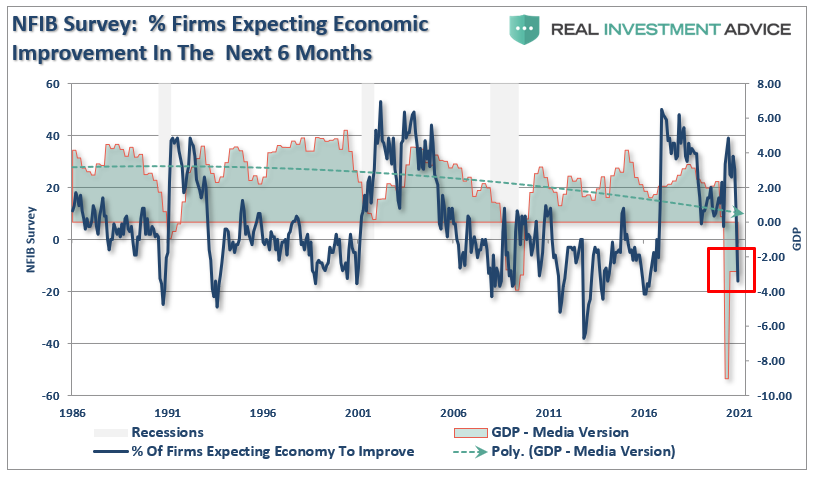

Small Businesses Are Less Confident As Well

As we discussed in January, the small business survey put out by the National Federation of Independent Business showed a sharp drop in confidence despite a supposedly improving economy, roaring stock market, and low rates.

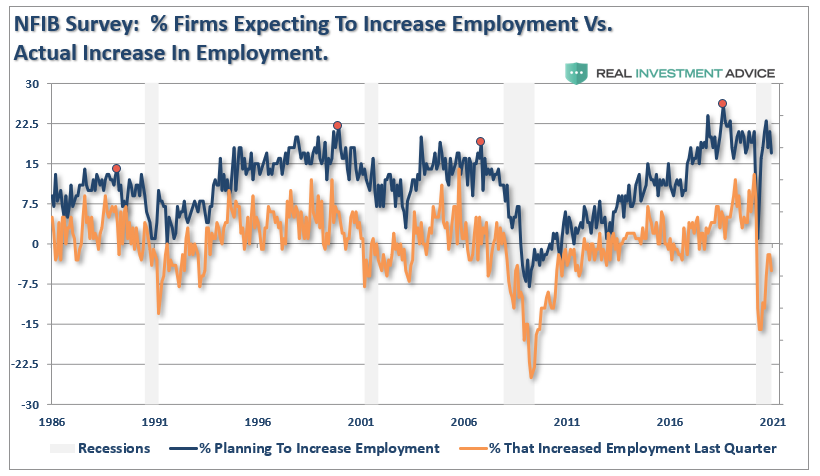

As noted above, if small businesses believe the economy is “actually” improving over the longer term, they would be increasing employment. Given business owners are always optimistic, over-estimating hiring plans is not surprising. However, reality occurs when actual “demand” meets its operating cash flows.

To increase employment, which is the single most considerable cost to any business, you need two things:

-

Confidence the economy is going to continue to grow in the future, which leads to;

-

Increased production of goods or services to meet growing demand.

Currently, there is little expectation for a strongly recovering economy. Such is the requirement for increasing employment and expanding capital expenditures.

Such also helps you understand the biggest problem with artificial stimulus. Yes, injecting stimulus into the economy will provide a short-term increase in demand for goods and services. When the funds are exhausted, the demand fades.

Small business owners understand the limited impact of artificial inputs. As such, they will not make long-term hiring decisions, an ongoing cost, against a short-term artificial increase in demand.

Also, given President Biden is focused on more government regulation and higher taxes (which falls squarely on the creators of employment), increased costs will further deter long-term hiring plans.

Stimulus Doesn’t Replace A Job.

When it comes to the economy and creating organic economic growth, it is the symbiotic relationship between businesses and consumers.

Such is the point that has eluded policymakers at the Fed and in Washington.

More importantly, the evidence is abundantly clear. After a decade of zero interest rates, more than $36 trillion in interventions and monetary accommodation, the economy collapses on the slightest reduction.

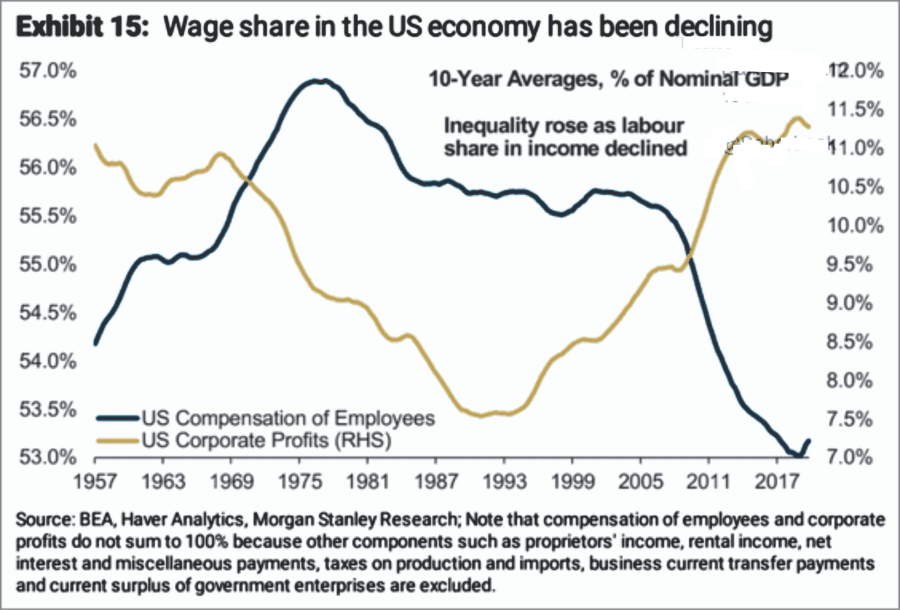

These interventions exacerbated the wealth gap and grossly inflated corporate profitability at the expense of worker’s wages.

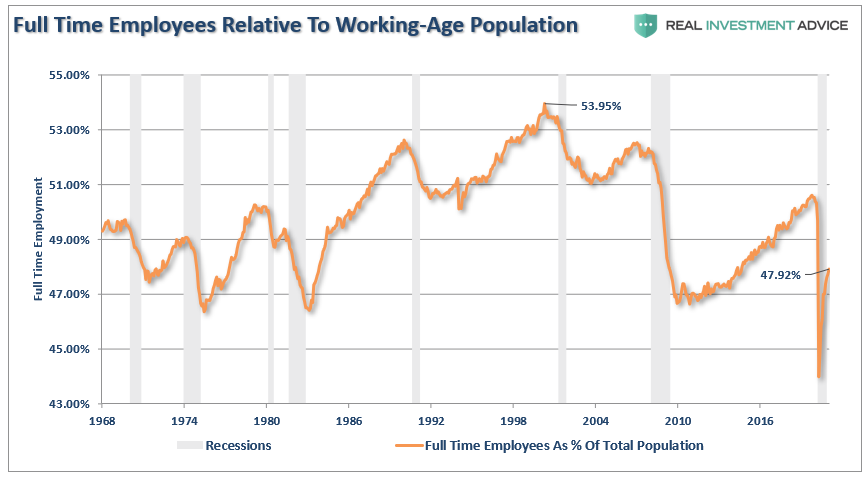

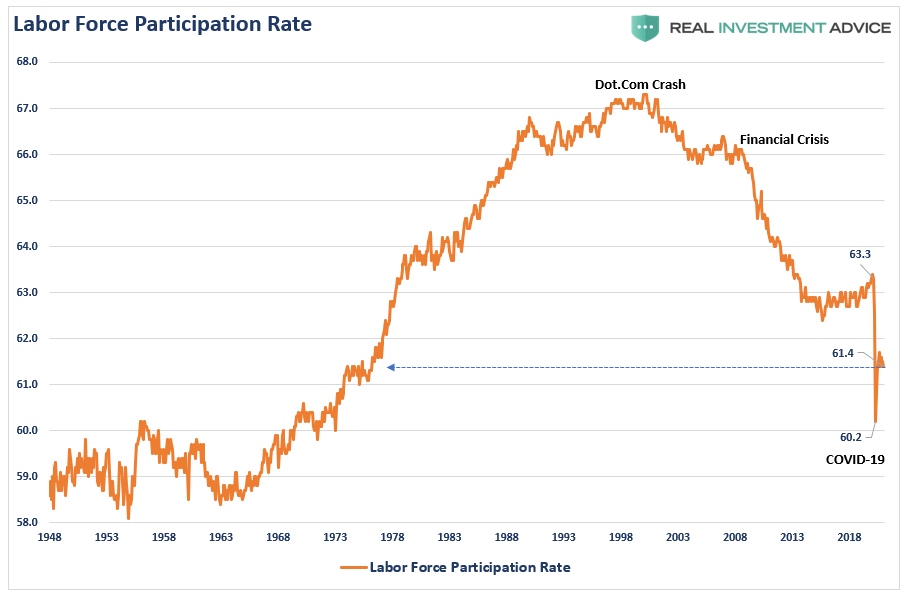

Furthermore, employment, which is the backbone of consumer confidence, has not increased strong enough to create sustainable economic growth above 2%. Notably, the number of full-time jobs, which are critical to sustaining a family, has continued to decline.

Notably, that number remains skewed due to the “labor force” calculation. Even though the economy may approach “full-employment,” much of that is an illusion created by the labor force’s shrinkage.

While a “stimulus” check may solve a short-term need, consumers are well aware such is a short-term benefit.

What would boost their confidence is a job.

The Wrong Vaccine

Following the CARES Act, many consumers spent their stimulus checks believing their job loss was only temporary. Today, many of those temporary job losses have now become permanent. That realization by consumers may well change how they spend the next round of stimulus payments. Rather than immediate consumption, the focus may well change to paying down debt or catching up on delinquent mortgage payments.

If such does turn out to be the case, the economy’s impact will be substantially less than anticipated, and confidence will likely erode further.

While Powell hopes that more stimulus will create an environment where more companies will hire, they will only do so when demand is growing organically. As noted previously, stimulus payments don’t inspire business owners’ confidence to increase capital expenditures, hire employees, or take on more risk.

If you want business owners to take on long-term risk and put employees to work, you have to allow capitalism to operate efficiently. Such would require letting “Darwinian” processes take root to clear the system.

As with any illness, the “cure” can often be painful at first, but the long-term benefits are often worth it.

Tyler Durden

Tue, 02/16/2021 – 06:30![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com