Morgan Stanley: This Is The Biggest Threat To The Red-Hot Global Recovery

By Chetan Ahya, Morgan Stanley’s Chief Economist and Global Head of Economics

A year ago, when the global economy was in the depths of the Great Covid-19 Recession, we argued for a V-shaped recovery and the return of inflation. 12 months on, deep scepticism has given way to broad agreement.

The debate now is whether the strong recovery and pick-up in inflation were just a spurt driven by policy support and reopening. If so, global growth could slow as it did in 2012 when policy-makers withdrew fiscal and monetary policy support. The resulting weak growth and lowflation environment raised fears of secular stagnation.

Our three-factor framework has shaped how we have been thinking about this cycle.

- First, COVID-19 was an exogenous shock, unlike the Great Financial Crisis, which resulted from excessive private sector leveraging.

- Second, in the absence of moral hazard issues, policy-makers responded actively and aggressively.

- Third, as the declining share of wages in GDP and rising income inequality came to the fore, an inclusive growth environment emerged as a goal of both monetary and fiscal policy. The bias will be to err on the side of keeping policies expansionary.

Against this policy backdrop, we foresee a sustained recovery.

The US is playing an outsized role in driving the strong global growth story in this cycle. We see global GDP rising above its pre-COVID-19 path from 3Q21, reaching 6.5%Y in 2021 and 4.8%Y in 2022, ~50bp above consensus for 2021-22. This amounts to the sharpest rebound in the last five cycles. US GDP overshoots its pre-recession path, an outcome not seen in the previous two cycles.

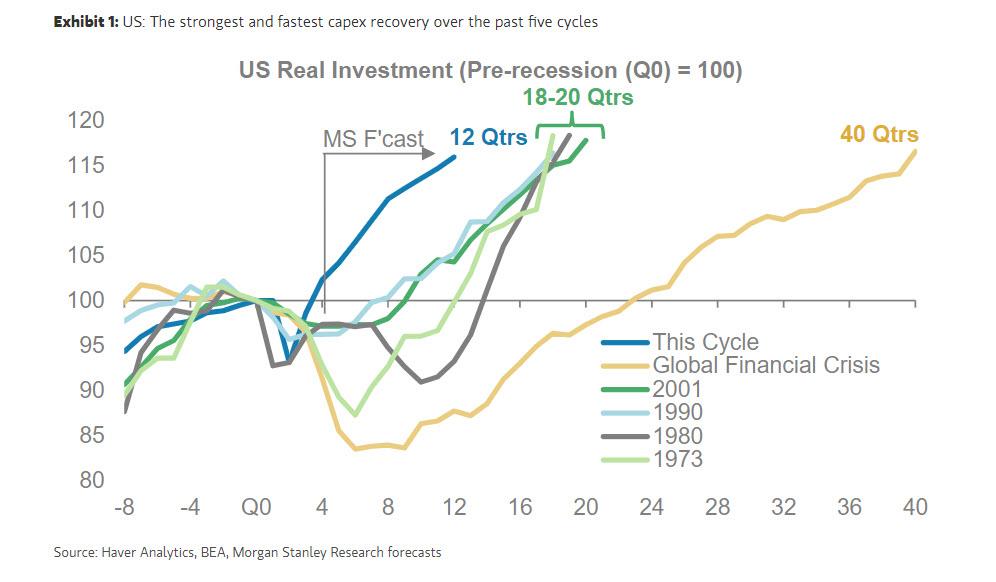

So far, the recovery has been led by a sharp rebound in consumption and an initial pick-up in capex. The ongoing recovery in personal incomes and the elevated excess saving stock suggest that consumption growth will be sustained. In the next leg, we believe that the strong recovery in aggregate demand will drive a red-hot capex cycle. Global investment will rise to 121% of pre-recession levels by end-2022, with US investment at 116% of pre-recession levels by the end of next year, a threshold that took 40 quarters to reach in the last cycle.

Indeed, if low growth and lowflation characterised the macro environment post-2010, this is emerging as an environment of high growth and higher inflation, diminishing the risk of secular stagnation.

In the US, this translates to a growth environment where GDP will be 3pp above its pre-COVID-19 path by end-2022 and underlying core PCE inflation (adjusted for base effects) rises above 2%Y from March 2022. The Fed, which is now aiming for inflation averaging 2%Y and maximum employment, should remain accommodative. Our chief US economist Ellen Zentner expects the Fed to signal its intention to taper asset purchases at the September FOMC meeting, to announce it in March 2022 and to start tapering from April 2022. On our forecasts, rate hikes begin in 3Q23, after inflation remains at or above 2%Y for some time and the labour market reaches maximum employment.

What are the risks to this story? Most obvious is the emergence of new COVID-19 variants that resist vaccines. However, I have argued that the biggest threat to this cycle is an overshoot in US core PCE inflation beyond the Fed’s implicit 2.5%Y threshold – a serious concern, in my view, which could emerge from mid-2022 onwards.

Transitory factors and base effects, which we are seeing now, should be ignored. Instead, sustainably higher inflation will be driven by tighter labor markets and a rise in aggregate wage costs. This dynamic has already begun to play out, notably with the employment cost index at 2.7%Y, just 20bp shy of its pre-pandemic high. We foresee wage cost pressures intensifying as the fast recovery in GDP brings a rapid improvement in the labor market.

Moreover, aggregate wage costs could rise even with considerably higher levels of headline unemployment. Job losses are concentrated in low-wage sectors, with a 68% share, almost double the level in the last recession. As policy-makers push for a high-pressure economy to bring jobs back, the strength in aggregate demand will lift unemployment rates for middle- and high-income sectors, which are already near pre-pandemic levels. The impact on wage costs from intense pressures on labor demand will be compounded by the labor supply side. The pandemic has accelerated the economic restructuring process, which is lifting the natural rate of unemployment.

What does the macro backdrop means for markets? Strong economic tailwinds create both risks and opportunities. Our chief cross-asset strategist Andrew Sheets sees higher inflation and richer valuations complicating the strong growth environment. A mid-cycle market leads our cross-asset strategists to recommend reducing exposure to credit and equities, and they are reducing their underweight in cash, a move supported by cycle-adjusted risk premiums.

While retaining a small overweight in global equities, they favor DM ex US equities, especially Europe. In the US, our equity strategists are tactically cautious on risk. However, after the correction has played out in the near term, they see a bull market resuming with better breadth and a reflationary tilt. They are overweight sectors most levered to reflation on a longer-term view (financials, materials and industrials) while favoring reasonably priced growth (healthcare) over more expensive growth (technology). In macro markets, stronger growth but ample liquidity should keep the rise in yields near forward rates, while we see USD modestly higher in a narrow range. Commodities should overshoot fair value.

Tyler Durden

Sun, 05/16/2021 – 15:06![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com