DoJ Launches Criminal Investigation Into Archegos Blowup

Following earlier reports that investigators had been sniffing around the prime brokerages that extended credit to Archegos, along with some critical comments from top market regulators, Bloomberg reported late Wednesday that federal prosecutors in Manhattan have officially launched a criminal investigation into the Archegos blowup.

But according to Bloomberg, it appears the DoJ is now taking over after the SEC launched a preliminary investigation into Bill Hwang, the owner of Archegos, which operated as Hwang’s family office, back in March.

The Department of Justice is investigating the market-rattling meltdown of Bill Hwang’s Archegos Capital Management in March, a debacle that left big banks in Europe, Asia and the U.S. nursing more than $10 billion in losses.

Federal prosecutors in Manhattan sent requests for information to at least some of the banks that dealt with the firm, according to people with knowledge of the matter, who asked not to be identified discussing the confidential probe. It’s unclear what potential violations or entities authorities are examining.

A spokesperson for prosecutors declined to comment, a spokesperson for Archegos didn’t immediately respond to a request for comment.

Archegos’ prime brokers initially attempted to try and avoid a market panic by coordinating their sales of the massive blocks of shares their had accumulated on behalf of Archegos via a complicated series of swap arrangements. But when Goldman Sachs and Morgan Stanley broke ranks and opted to be the first out the door, Credit Suisse, which had the biggest exposure to Archegos, was ultimately left with more than half of the $10 billion+ in losses that banks were stuck with (while Hwang reportedly lost his entire 11-figure fortune).

Right now, it’s not exactly clear what laws prosecutors suspect Archegos and the prime brokers of breaking.

While authorities haven’t accused Archegos or its banks of breaking any laws in their dealings, the episode has drawn public criticism from regulators, as well as some inquiries behind the scenes from watchdogs around the world. The implosion shows Wall Street has grown too complacent about potential threats building up in the economy, Michael Hsu, the new acting chief of the Office of the Comptroller of the Currency, said last week.

But the DoJ isn’t the only agency poking around: Investigations are ongoing across the globe.

The Securities and Exchange Commission launched a preliminary investigation into Hwang in March, a person familiar with the matter said at the time. The agency has since explored how to increase transparency for the types of derivative bets that sank the firm.

And in the U.K., the Prudential Regulation Authority has been asking firms including Credit Suisse, Nomura and UBS Group AG to hand over information related to their lending to Archegos, people familiar with the matter have said.

While investigators will undoubtedly focus on what happened, some believe that the real concerns lie in current vulnerabilities in the world of equity finance. The team at Risky Finance recently calculated that some $3 trillion in hidden Archegos-style exposure is out there in the market, just waiting to explode if stocks sell off.

When the family office Archegos Capital abruptly imploded in late March, prompting $50 billion in block trades and $10 billion in losses at Credit Suisse, Nomura, UBS and Morgan Stanley, many bank analysts were taken by surprise. Last week, many of these analysts sounded frustrated listening to Credit Suisse’s earnings call in which senior management skirted round without giving any real detail about the disaster.

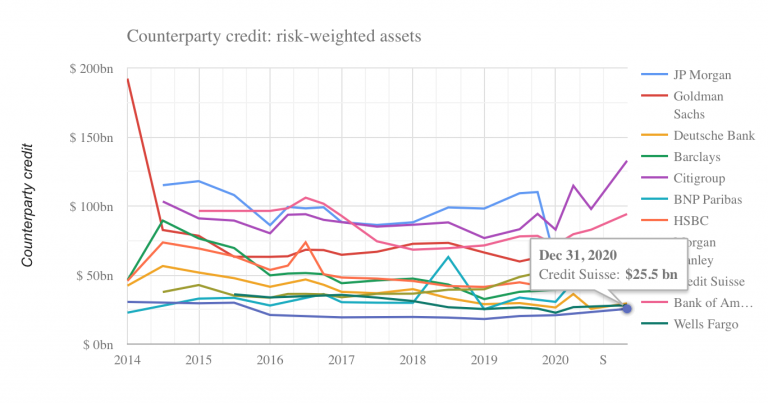

“Do you think it’s possible that this could produce a very fundamental reset in how your IRB credit risk models work?” wondered Stefan Stalmann of Autonomous Research. “I mean you have only CHF20 billion to CHF25 billion of counterparty credit risk-weighted assets on literally hundreds of billions of equity swaps and repos”.

Risky Finance shares Stalmann’s bewilderment. Expressed as a capital requirement, Credit Suisse was able to satisfy regulators with just $2 billion of capital for counterparty credit losses – the lowest among the G-SIFI banks tracked by Risky Finance. Months later it reported a loss of $4.7 billion.

It should serve as a warning. 14 years ago, obscure corners of banking businesses became hotbeds of regulatory arbitrage, speculation and leverage. The contagion of US subprime brought the financial system to its knees. Now, after years of low or negative interest rates, equity finance may have become a similar hotbed.

The business is much larger than published estimates – Risky Finance believes there are more than $3 trillion of exposures. And the pressure to grow equity finance is leading banks to exploit loopholes in Basel rules. As in 2007, this is masked by the complexity of the models that Credit Suisse and other banks used to allocate capital to their prime brokerage business.

In following articles we will try to unpick the way Archegos was so damaging, and we will give a broad brush picture of how the risk models are supposed to work. And we will showcase some new data that reveals why this business is bigger and riskier than many imagined. Lastly we will identify a list of fixes for regulators to work on.

Tyler Durden

Thu, 05/27/2021 – 12:20![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com