Nomura Warns Of Market “Reversal Risk” As FedSpeak Walks Back ‘Bullard Bomb’

After last week’s market fireworks on the Fed’s “hawkish surprise” and Jim Bullard’s “you think that’s hawkish, hold my beer” moment on Friday morning, which has many market participants screaming “policy error”, Nomura’s Charlie McElligott warns traders now need to be ready for some potential “reversal of the rhetoric” this week – especially as we are looking at an astounding sixteen (!) Fed speakers on the calendar ahead…

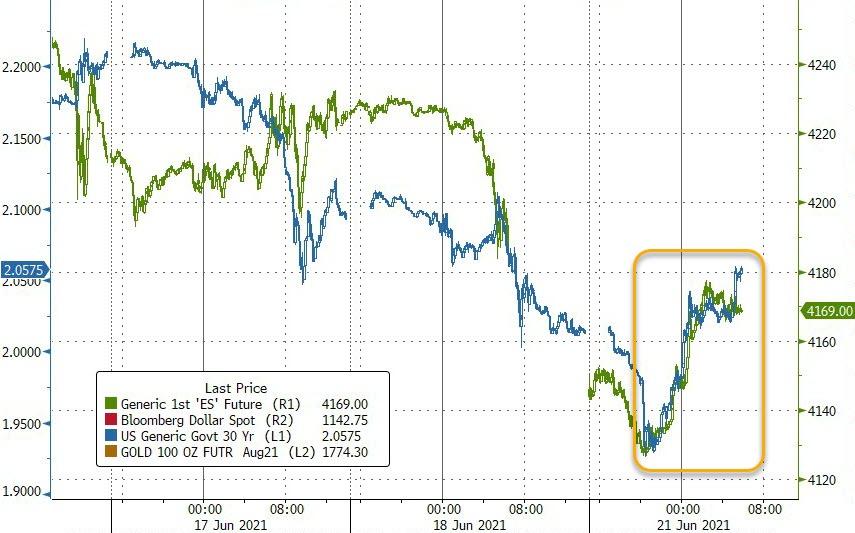

…which is notable in that both Treasury Yields and Equities are already substantially higher versus Asian reopening lows…

Which McElligott warns, risks creating a counter-trend reversal which could catch many flat-footed again as tactically, any semblance of walking-back from the Fed could then elicit an optic of “Reflation,” particularly if USD were to weaken further from here, Real Yields were to again tilt more negative and UST curves then again “bear-steepen” after their eye-water liquidations / stop-out last week—which too would then likely trigger a concurrent bounceback of the prior “Cyclical Value over Secular Growth” trend in US Equities, after said expressions were powerfully de-grossed last week (Nasdaq +0.4% last wk vs Russell -4.1%)

-

Equities “Reflation” last week: Nomura 10 Yr Yield Sensitive Factor -4.6%; Cyclical Value Factor -3.5%; Growth Nowcast -3.1%; LT Momentum -3.1%; Wolfe AVID Value -2.7%; Defensive Value -2.4%

-

Equities “Duration” last week: IG Credit Sensitive Factor +2.7%; HF Crowding +2.2%; Low Risk +2.0%; Size (Big-Small) +1.3%; Dividend +1.0%

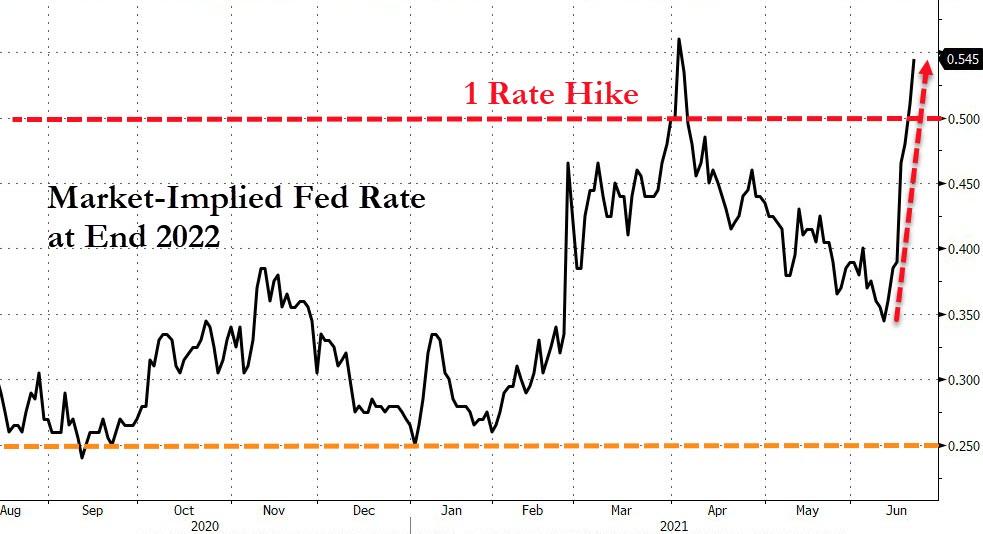

This is what the unspoken “third Fed mandate” of maintaining “easy financial conditions at all costs” hath wrought – an absurd cycle where Fed policy and the US economy actually works to a point where in “old” central banking, the Fed would accordingly pivot “hawkish” and begin tightening policy; but in the “Fed Put” world order, market forces now pull-ahead the negative economic slowdown implications of said “tightening” and have “taper tantrums” creating market volatility, ultimately forcing the Fed to walk-back hawkish tone shifts if the market.

In this case, the risk this week then becomes that some portion of the very active calendar of Fed speakers will now voice a “concern” that last week’s dot plot and SEP will work against their previously stated FAIT desire and impede future growth- and inflation- expectations, and could then message on just how “conditional” those forecasts are – i.e. downplaying their forecasting ability, in an attempt to reverse some of the market’s pull-forward of “tighter financial conditions” due to perceived “hawkish pivot” from Fed which nullifies their own prior efforts to reset future inflation expectations!

And as we have now seen countless times before, if the Fed then again “bends the knee” to market forces, the vol spike and forced deleveraging / hedging of risk-assets is then reversed with “rich vols” then sold into, which in standard lagging-fashion will mean that as trailing rVol then resets lower following the expected “Fed back-track,” a large covering of dynamic hedges (shorts) and / or mechancial re-leveraging of risk-asset exposure from “Target Volatility / Vol Control” universe will then see markets resume their rise, as vols are smashed – “Crash-down, then crash-up” rinse / repeat.

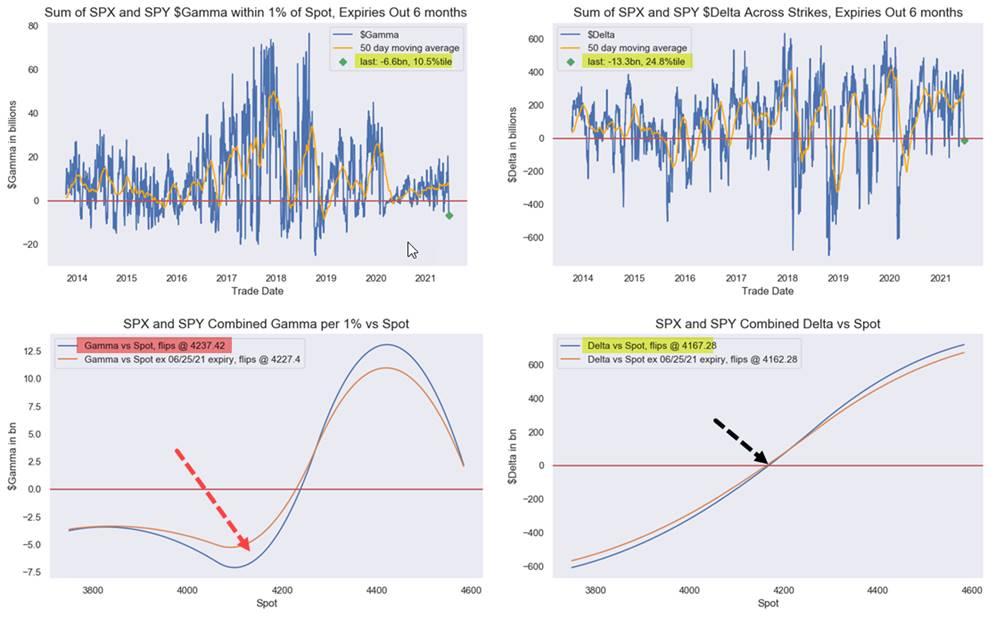

To further contribute to these potential “sling-shot” (crash-down, then crash-up) optics, we now inherently see much “cleaner” options positioning (current ES at 4167, which is the “Delta Neutral vs Spot” level) post last week’s abnormally outsized Op-Ex (although worth-noting that we are now in “short Gamma vs spot” territory at 4167 last vs 4237 “Gamma neutral” line).

And in the case that the incremental “hawkish Fed surprise” vol spike is sold into Dealers by the VRP crowd (particular with any semblance of “Fed walk-back” this wk), this impulse supply of Volatility- and Gamma- will again then perpetuate a more stable, insulated market thereafter, as Dealer “long Gamma” means hedging flows will further squelch the potential for market moves – hence, the virtuous cycle phase of the “vol selling” feedback loop.

Tyler Durden

Mon, 06/21/2021 – 09:33![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com