Rabobank: Welcome To The Mismatch Economy, The Implications Are Huge

By Elwin de Groot, head of macro strategy at Rabobank

Welcome to the Mismatch Economy! A scan of the latest news stories clearly rams home the message that mismatches (or imbalances) are all but ubiquitous. In fact, they seem to be entirely running the show at the moment. The implications of this are – obviously – huge as, such mismatches not only make it very hard to interpret the data and establish whether something is temporary or permanent, it will almost surely lead to new policy errors (which themselves are likely to create new future imbalances). Even traditional (aggregate) demand versus supply analysis misses the point, especially if such imbalances are of a sectoral or regional nature.

Let’s start with financial markets where all these things come together and we are supposed to be able to read the ‘true and actual’ state of affairs on a minute-by-minute basis. For the most part of this year, equity and credit markets have been telling us that Covid no longer is a big issue. Although we had a bit of a dip in the first half of July (followed by a sharp recovery) and then again another dip in sentiment last week as investors fretted about the spread of the Delta variant, those concerns seem to have been put to rest again (as Bloomberg yesterday said: “investors are buying the dip!”). Yesterday’s news of the full approval of the Pfizer-BioNTech Covid shot by the US FDA gave markets another fillip, raising the prospect of an accelerated push for vaccination as it would give companies and governments the backing to put it up as a requirement for relaxation of social-distancing rules.

And, as always, investors are banking on continued (fiscal/monetary) policy support as long as Covid hasn’t been defeated. That switch in thinking was arguably ignited by comments from Dallas’ Fed’s Kaplan last Friday when he said that he was watching carefully the impact from the Delta variant and that he might need to adjust his view on policy “somewhat”. And so the expectation now is that the Fed Chair will NOT use the upcoming Jackson Hole meeting as an opportunity to pre-announce a taper of its asset purchase program. These expectations are taking place against a backdrop of a strong rebound in company revenues and earnings.

Zooming in on Europe (Eurostoxx 50 non-financial companies to be specific), we note that the four-quarter running average of both revenues as well as operating profits has nearly fully recovered to its 2019Q4 level. Indeed, gross operating margins almost hit 14% in Q2, which is the highest level in at least 15 years and almost double of the margins seen during 2020H1. So no mismatch between fundamentals and stock prices there? And how does that fit in with the (still) very low level of core inflation in the Eurozone (0.7% y/y in July) whilst input prices (PPI ex-energy +4.8% y/y in June) have been going through the roof? This either means that companies have not yet felt those cost pressures to the full extent (due to hedging and/or long-term contracts) or margin pressures have been masked by the supply-demand mismatches as the economy re-opened. In other words, the ‘return to normal’ may turn out to be not be so normal after all.

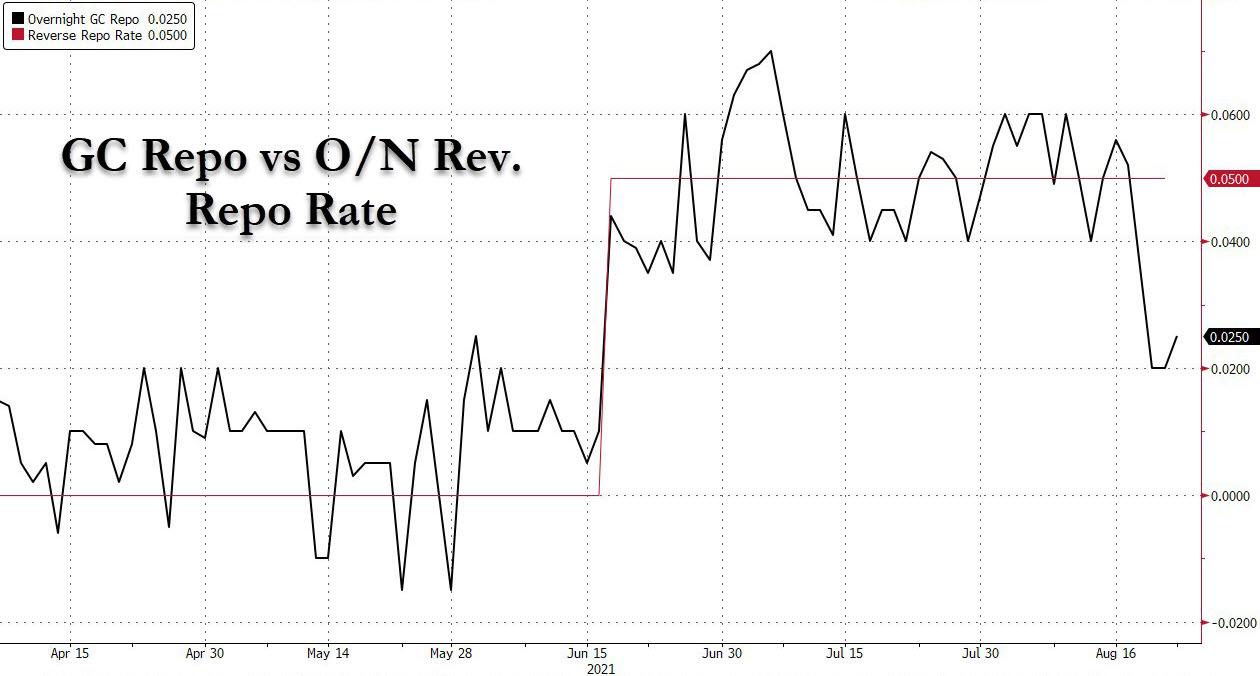

But there are definitely mismatches in corners of financial markets that are easier to pinpoint. Money markets are a point in case. The Fed appears to be outnumbered by the sheer amount of cash available in the system, rendering its floor for overnight funding rate ineffective. Despite record-high usage of the Fed’s reverse repo facility various money market instruments continue to trade below the rate offered on this facility.

The reverse repos, which allow institutions to deposit funds overnight at the Fed, are supposed to provide a floor on short-term rates, and back in June the FOMC decided to raise the rate on this overnight reverse repo facility to 5bp (from 0.00%) in order to safeguard the proper functioning of US money markets. Excess liquidity is a key element lowering the RRP’s impact on short-term market rates, but a tapering decision is unlikely to alleviate this issue quickly. After all, even under a tapering regime liquidity continues to be injected, albeit at a slower pace. In fact, in the short-term, it may be up to Congress to lessen this mismatch: lacking an agreement on raising the debt ceiling, the US Treasury has started to cut back on T-bill supply, leaving more money market funds chasing fewer assets.

Yet, central banks are not free from blame. Turning to the Bund curve, 10y yields have been trading in the -45 to -50bp range again since late July. At the same time, EUR inflation swaps have been recovering somewhat, with the 10y rising from around the 1.5% mark to 1.66% currently. In other words, recent moves in the Bund suggest slowing Eurozone growth expectations. While there are certainly still elements of uncertainty surrounding growth, that reaction seems a bit much. Another possible cause? PEPP. PEPP buying continues at a pretty rapid pace considering the quiet summer weeks. In past four weeks, the ECB amassed an average of EUR 15bn each week. Admittedly, that is less than the EUR 18bn per week since the Bank raised its purchase pace, but it again begs the question to what extent central banks have been distorting markets, causing mismatches with underlying developments in the real economy.

Turning back to the real economy, yesterday’s PMI surveys for August provided further evidence of the scale and pervasiveness of demand-supply mismatches. In Europe the surveys continued to point to a robust recovery in economic activity with the manufacturing PMI falling a bit but staying at historically high levels and activity in services continuing to recover at a high pace. Indeed, according to Markit, service sector output growth exceeded that of manufacturing for the first time since the pandemic. Whilst ‘re-opening’ and rising demand for labor was a key factor behind the strength in services, the slowdown in manufacturing was likely caused by supply constraints; as reflected in rising backlogs and ongoing input costs pressures. Similar conclusions could be drawn from the UK survey. In the US and Japan the data were clearly weaker on balance as services sector activity dropped more sharply in the US (index fell from 59.9 to 55.9) and in Japan services sector activity even fell to 43.5, its lowest level since May 2020. Recent (partial) port closings in China and the spread of Covid in many parts of Southeast Asia suggests we haven’t seen the end to supply disruptions. Indeed, mismatches may well be expected to increase in upcoming months. Taiwan and South Korea have recently been singled out as the main countries to watch when it comes to global chip shortages, but Malaysia should not be overlooked, as Bloomberg reports. The country has advanced its position as a major chip testing and packaging sector in recent years, but may – as a result – turn out to be another weak part in the chain given the rampant pace of delta, which has forced companies to cut back operations in the country.

The other, potentially even more sticky (longer-lasting), mismatch is currently playing out in European and US labor markets. On the one hand vacancies and job-openings are recovering sharply on the back of a re-opening economy, on the other are we still witnessing elevated unemployment and even more subdued employment levels (as compared to pre-Covid times). Discrepancies between the type of jobs companies are offering and the type of jobs people are willing or able to fulfill are a key factor in the short-term. As Philip Marey explains in this special, in the US this largely boils down to an asynchronous re-opening of businesses (earlier) and schools (later), aggravated by (temporarily) elevated benefit levels, giving people a reason to postpone their return to the labor market. These mismatches may progressively disappear, provided vaccination allows a broader reopening of the economy, but this may mask longer term trends such as population ageing that may prevent labor participation rates from returning to pre-Covid levels. Such distortion, of course, could be another recipe for policy errors.

Tyler Durden

Tue, 08/24/2021 – 10:15![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com