Sunday Collum: 2021 Year In Review, Part 1 – Crisis Of Authority & The Age Of Narratives

Authored by David B. Collum, Betty R. Miller Professor of Chemistry and Chemical Biology – Cornell University (Email: [email protected], Twitter: @DavidBCollum),

Dave: You do lack self control, but I learned and laughed making my way thru this.

~ Larry Summers (@LHSummers), former Secretary of the Treasury

Every year, David Collum writes a detailed “Year in Review” synopsis full of keen perspective and plenty of wit. This year’s is no exception.

Introduction

I’ve been trying to reach you about your car’s extended warranty. What began more than a dozen years ago as a synopsis of the year’s events in markets and finance for a few friends morphed beyond my control into a Year in Review (YIR)—an attempt to chronicle human folly and world events for the entire year. It captures key moments before they slip into the brain fog. The process of trying to write a coherent narrative helps me better understand WTF just happened and seminal moments that catch my eye.

By far my favorite end-of-year recap for the last ten years. Finished it yesterday. Once again David hasn’t disappointed. He’s on my I want to go to dinner with list.

~ Jim Pallotta (@jimpallotta13), money manager and former owner of Boston Celtics

I’m game, Jim, even if it’s just a pretzel, nachos, and a brewski. The title, “Crisis of Authorities,” is a double entendre. On the one hand, previously trusted authorities that we relied on to better understand the world are long gone. Edward R. Murrow, Walter Cronkite, and Tim Russert have been replaced with Chris Cuomo, Don Lemon, and Brian Stelter. Oops. Scratch Chris Cuomo. Ponder the following: which acronymed organization do you still trust? FBI? CIA? FEMA? DOJ? CBS? ABC? Fox? CNN? At one point I would have comfortably offered up the CDC, FDA, and NIH. Portions of those three should be razed. Social media offered up one acceptable answer: KFC. The second, more deeply disturbing meaning is that smoldering socialism has veered toward authoritarianism, a seismic shift that is global and quite possibly unstoppable.

2021: The year liberals threw eggs at black politicians, republicans pushed to legalize pot, conservatives declared “my body, my choice”, and libertarians muttered, “just shoot me now.”

I am suffering future shock—the struggle to adapt to an abruptly changing world. Topics that seemed farcical not long ago are less entertaining now. Silly events in public schools and college campuses loosely defined as political correctness have morphed into religious wars. Progress was made in the Cancel Culture Wars. They tried to get Joe Rogan and couldn’t put a glove on him. The populace and the workers at Netflix went after Dave Chappelle and learned that not everybody kowtows:

If this is what being canceled is like, I love it… To the transgender community, I am more than willing to give you an audience, but you will not summon me. I am not bending to anybody’s demands.

~ Dave Chappelle, wisdom

Politicians groping for their vig—10% for the Big Guy—have mutated into total MAC (Mutually Assured Corruption). Social contagions are more virulent than biological pathogens. Attempts to stem the movements are emblematic of proto-authoritarianism of the past. I am unable to keep up—unable to even catch my breath on some days. Following up after listening to a widely distributed QTR podcast, a friend and long-time YIR reader asked, “Are you OK?” I said I was fine, but on further reflection realized I was not so sure.

You will never reach your destination if you stop and throw stones at every dog that barks.

~ Winston Churchill (@DeadGuy)

I have lost friends and made new ones all because of the Great Partisan Divide. (Please excuse the caps throughout; everything now seems to demand a proper name and acronym.) My colleagues have put to rest doubts about whether I am nuts, noting that I am contrarian on all topics. Of course, they don’t hear about the ones for which I have no gripe, but their assertions are not entirely wrong. Friends let me be me, but there is something isolating about it. By contrast, I have many friends in the digital world for which the Venn Diagram of Ideas has a much greater overlap. You can have friends without ever seeing them in the flesh, but these digital pals become bucket-listers for me to meet. Some accept my invitation to have dinner on my deck overseeing Cayuga Lake. Try explaining to your wife that you are having dinner with some guy you met on the internet. This has included famous people like David Einhorn, Tony Deden, Cate Long, and Doug Noland as well as walk-ins whom I knew nothing about until they showed up with a bottle of wine. They have, without fail, brought rewarding evenings of lively chat.

Disclaimer:

Opinions and ideas expressed herein are not my own. I also don’t use asterisks, so you are just going to have to grow a f*cking pair. If this message is lost because you have sh*t for brains, my advice is to stop reading now.

Philosophy. I have let go of the belief that I know truth, because I am relentlessly doubting the veracity of the data from which my narrative derives. In the Age of Narratives, all I can offer is Dave’s Narrative. There is also no topic in the Year of Our Lord 2021 in which my opinion is non-partisan because all opinions are now partisan. Consequently, I may come off as a right-wing white supremacist who moonlights as a Russian operative while serving up nostrums characteristic of an anti-war ex-hippie.

This guy is so left wing that he doesn’t even understand his own bias.

~ Rich Weatherford, commenter on a podcast

The surest way to make a monkey of a man is to quote him.

~ Richard Benchley

My attempt to create a Unified Theory of Everything is very much like building a jumbo jet in mid-flight. In science, when your model is right, it starts playing like the tail end of a game of Solitaire or a jigsaw puzzle—the cards and pieces naturally fall into place. If the nothing makes sense no matter how hard you try, it may be time to tear down that Rube Goldberg structure and start from a fresh perspective. My greatest strength and weakness are an ability to entertain almost any idea—entertain conspiracy theories and scamper down rabbit holes—until I hit paydirt or hardpan. Feel free to call me a conspiracy theorist; it helps me identify narrow-minded boneheads. What baffles me is why “conspiracy” is so pejorative. Men and women of wealth and power conspire. Anybody who cannot concede that point is an intellectual dingleberry (or works for the Deep State!)

Alex Jones got more right than CNN.

~ Dave Smith, comic and possible presidential candidate

Conspiracy theorists of the world, believers in the hidden hands of the Rothschilds and the Masons and the Illuminati, we skeptics owe you an apology. You were right. The players may be a little different, but your basic premise is correct: The world is a rigged game.

~ Matt Taibbi

I am an openly white, right-leaning, closeted hand-sexual male with audacious opinions. I promise, however, that I will sling barbs without regard to race, creed, or color. If I think you are a douche bag, I will say so. When anger consumes me, however, it gives way to angst because somebody may have suckered me into playing a role in some higher authority’s master plan to disrupt the American Dream. As we are being dazzled by the Harlem Globe Trotters, recognize that we are the Washington Generals.

Remember the olden days when the wealthy and powerful nefariously assaulted the unsuspecting populace? If caught, scandal followed, heads rolled, and we moved on, leaving us plebes with the sense that justice was served. Since the government was small relative to GDP, the systemic corruption represented a few percent of the system. It’s now growing like a tumor and devoid of consequences for the powerful. In the Age of Narratives, we snarf down platters of propaganda served by powerful media empires. This bread and circuses is free but leaves us marinating in ignorance.

It’s a trap Mickey: the cheese is not free!

The Western media is now the arm of the State, no better than Pravda. Failed business model led the media into the oldest profession. How many narratives have we fallen for? How many have you fallen for? I think you owe it to yourselves to replay the tape from years past and ask whether you were duped. Malcolm Gladwell’s latest (see Books) suggests we are hard-wired to trust. As social animals, we cannot function if we don’t. It’s difficult to push back but push back we must. The more highly politicized the topic—climate change, pandemics, vaccines, elections, central banking, foreign wars—the greater the urgency to repel. I offer up one of several quotes from Gore Vidal, a thought-leader canted profoundly left whom I have come to view as the intellectuals’ George Carlin:

Our rulers for more than half a century have made sure that we are never to be told the truth about anything that our government has done to other people, not to mention our own.

~ Gore Vidal

Sources and Social Media. I am a Twitter long hauler with 70,000 followers but haven’t yet figured out how to monetize the micro-fame enough to buy a mocha Frappuccino. I do, however, find it a useful sounding board. One tweeter—probably a Twitter bot—captured the essence:

If you need something researched for free and you don’t feel like doing it just post a tweet about it that’s mildly incorrect and wait.

~ @InternetHippo

My Twitter long hauling has occasionally been interrupted by Twitter time-outs. They range from 12 hours to ponder the err in my ways for posting an inappropriate link to Bichute or The Lancet, to a full week for calling Tony Fauci “a skanky whore.” A permanent ban would (will) be painful because I have old and new friends there—Rudy: I love ya man!—who enrich my life with their wisdom. New posse members joining the already eclectic mix include @JonNajarian (getting me closer to winning CNBC Twitter Bingo), scholar and author @BretWeinstein (see Books), actor @AdamBaldwin, polymath rapper @ZubyMusic, and waves of bitcoin hodlers. Favorite news sources include podcasts—I am an audiophile—as well as blogs and newsletters by Tony Greer, James Grant, Jesse Felder, Bill Fleckenstein, Automatic Earth, Grant Williams, Ron Griess of The Chart Store, Chris Martenson, emails from a woman named Denise, and the 500 lb. gorilla of the internet—Zerohedge. I know I’ve missed many more. Apologies.

The trouble is, you think you have time.

~ Buddha

Figure 1. Toddler hacks the US Strategic Air Command; nuclear war was averted.

Topics Untouched. As usual, I am up to my ass in debris on the cutting room floor writing this beast. Some topics simply proved unworthy; others were not ready yet. One of the great merits of blogging is that blogs stand alone; write them when you wish. A once-a-year narrative, by contrast, demands some sort of theme or glue, and, frankly, you can’t write The Wealth of Nations in November. By December the tank read “Empty”, but there were topics I had to finish. I actually started getting minor migraines. What follows are thumbnail sketches of a few stories that were left largely untold.

There are decades where nothing happens, and there are weeks where decades happen.

~ Vladimir Lenin

By late 2020, it was clear that I had overlooked China as the global provocateur. They are Orwell’s hole in the air—the blurry schlieren in the jungle as the Predator arrives to tear out Arnie’s organs. The Chinese have infiltrated all aspects of the West’s geopolitical and economic system. Josh Rogin’s Chaos Under Heaven (see Books) is an excellent primer. I’ve heard second hand that the military top brass believes we are already at war but just don’t realize it yet. I regret punting the most important story, but they invented the punt for a reason.

I’ve taken a pass on campus politics, cancel culture, and all things politically correct. I know how much joy it brought many of you to find out how much you wasted sending your children to college, but this was an off-year. Cancel culture may be fading because, to put it bluntly, nobody likes a bunch of clueless douche bags. Critical race theory (CRT) with its deeply Marxist underpinnings and intentions is a bad idea whose time has come. In a law school, there are scholarly components. As it seeps into the K–12 zone it becomes a steaming load of crap. If you have kids, you should go to school board meetings and get arrested for speaking up or, what is now called, being a domestic terrorist.

It masquerades as objective science but was written as—all right, I’ll use the word—propaganda.

~ Steven Koonin (@SteveKoonin), former Cal Tech physicist, Obama Science Advisor, and author of Unsettled?

The 2019 YIR tackled climate change.ref 1 I thought I might be augmenting it this year, but I will simply leave it by noting a few high-water marks. Steve Koonin, former Cal Tech physicist, expert modeler of complex systems, and Obama chief science advisor wrote the book Settled?. (See Books.) Like many other “climate deniers” his creds are beyond reproach. Steve had chaired the American Physical Society’s committee of 12 elite scientists that examined the state of climate science. After paying some lip service to Mankind’s contributions, Steve eviscerated the models and absurdities comprising the Climate Change Narrative. This, of course, caused a seismic shift in the scientific community’s view of our global climate initiatives. Just kidding. Nobody gave a shit because trillions of dollars have already been spent on it and an estimated $150 trillion more will be handed out to anybody willing to feign belief in the Scriptures. I also had a long talk with a Stanford University psychologist and media expert who went down that rabbit hole and became a denier. Nothing will get in the way of this $150-trillion-dollar juggernaut. All hail Greta! By the way, Michael Moore’s Planet of the Humans appears to have snuck back on YouTube after being banned for truthiness. It is a good documentary.ref 2

Despite numerous podcasts with Holy Rolling Bitcoin Hodlers with their Scriptures under arm trying to sell me currency warranties, I remain on the sidelines (a no-coiner, pejoratively speaking). I cannot add much to this heated debate except to congratulate them for riding Metcalf’s Law to riches. I suspect their next test will be a Tether insolvency or a good ol’ fashioned credit crunch, prefacing the final Battle of the Bastards pitting the Hodlers versus The State unwilling to forfeit control of the money supply. All of this presumes cryptos aren’t just a fad. I wish you laser-eyed crazies well.

Dude –you deserve a Pulitzer for your coverage of the George Floyd Story, and I’m going to tweet that out.

~ Tony Greer (@TgMacro), TGMacro

In the 2020 YIR I wrote extensively on why Chauvin would be a tricky conviction.ref 3 At least two of us thought it worthy. The trial went off without a hitch. The media’s minor lipservice given to why angry mobs in the street would make it hard for the jury to remain unbiased while obsessing over why he should be convicted no matter what. The jury did their job. The part that was missed was the witness nullification. I must confess to not watching much, but nobody—as in not a single person in court—wanted to provide the testimony that got Chauvin acquitted. You could hear witnesses choose their words carefully. I’m not even sure the defense team wanted the win. Oh well, I wouldn’t underwrite Derek’s life insurance policy.

Prosecutor: But you decided you needed to run because of the fire of [inaudible]: why? What was so urgent?

Kyle Rittenhouse: There was a fire.

Enter the Kyle Rittenhouse trial. In shades of the Covington Scandal, even the President of the United States fondled the scales of justice to ensure the right outcome. The talking heads served up narratives that were fact-free clickbait to pay the bills. The prosecution was so comically bad—moments of great levityref 4a,b,c—that I began to wonder if they were tossing the case intentionally. Both the judge and the prosecution appeared to be intentionally setting up a mistrial. Kyle is gonna have a college essay to die for. Good luck getting it past all but Liberty University’s admissions committee.ref 5 In a related story, Nick Sandmann of Covington fame got his third quarter of a billion dollar settlement for defamation of character. Early negotiations are rumored to involve a 50:50 split of CNN by Sandmann and Rittenhouse.

Figure 2. Judge David Collum and Kyle Rittenhouse playing Call of Duty-Modern Warfare.

And now to bullet a few drive-by shootings:

-

The Epstein story could have been resurrected from the 2019 YIRref 6 with the arrest of Head Pimp, Gishlaine “Gizz” Maxwell, caught hiding in a New Hampshire mansion already surveilled by the FBI, but it is just starting. I’m guessing she will be convicted of a 1997 minor traffic(king) violation, punished with time served, and retire comfortably on the MPP (Mossad Pension Plan) to live out her days in seclusion with her manly girlfriend, Jessica Schlepstein.

-

Durham’s investigation of the Steele Dossier could heat up but hasn’t yet. Indictments are working their way from the bottom up. I won’t believe that plot has legs till I see it running. Nobody in power ever pays for their misdeeds.

-

The Pandora Papers showed galaxy-class criminality of the global elite socking over $11 trillion dollars away in off-shore accounts, but prominent Americans were notably absent.ref 7 The media assured us that there are no crooks of such sociopathy in America.ref 8 The story had the shelf life of a souffle.

-

John McAfee offed himself (or not). There were rumors that he had a kill switch that would hew vast stands of powerful people including voter fraudsters.ref 9 Well, McDeadGuy, we’re waiting. It won’t matter anyway because…oh never mind.

Major Themes of 2021. Enough already: what are you going to talk about? I cover the usual topics on the economy and investing and take a bat to market valuations again. Broken Markets are a prominent because they’ve never been more broken. Covid-19 and the vaccine get serious facetime as the opening act of a much bigger drama. The events at the January Insurrection offers more plot thickener as one of the most important single days in American history. That anagnorisis arrives when the voice says, “The call is coming from inside the house!” The final scene will be the rise of global authoritarianism—total global domination—and you squeal…

I did nazi that coming. WTF just happened?

Figure 3. Change comes with little warning.

Contents

Part 1

-

Introduction

-

My Year

-

Investing – Gold, Energy, and Materials

-

Gold and Silver

-

The Economy

-

Inflation

-

The Fed

-

Valuations

-

Broken Markets

Part 2 (Coming Soon)

-

Covid-19 – The Disease

-

Covid-19 – The Response

-

Vaccine – The Risks

-

Vaccine – The Rollout

Part 3 (Coming Soon)

-

Biden – Freshman Year One Scorecard

-

Capitol Insurrection

-

Rising Authoritarianism

-

Conclusion

-

Acknowledgment

-

Books

My Year

This report, by its very length, defends itself against the risk of being read.

~ Winston Churchill

I read a book on narcissism. Although I flunked yet another test having checked a paucity of the boxes, there were a couple of categories demanding a big Sharpie. Narcissistic tendencies underly all achievement so there’s that too. This section is where I wander through the last calendar year of my life looking for college-essay material. It can be skipped by all but the most loyal readers (three at last count).

That isn’t writing at all, it’s typing.

~ Truman Capote

Self-Improvement. OK. Let’s call it attenuated personal decay. I had dropped 26 pounds of comorbidity in 2020 and another 10 pounds in 2021. I am by no means emaciated yet. I was pestered by London money manager Mitch Feierstein into playing a seminal round of golf after decades of neglect and was hooked. While watching the final hole of the FedEx Open, Cantalay hits a 371-yard drive, a 217-yard 6 iron 10 ft from the cup and two-putts for a birdie and $15 million. I’m thinkin’, “Hey: I can birdie a par 5 with a few Mulligans!” A couple of lessons from two guys gunning for the PGA tour got me jump-started and eliminated the Cuomo and McConnell (duck hook left and shank right). My swing is still good, now if only I could hit the ball with it. Chipping is a soul-ripping experience after all these years. I’ve started peeling the 30 points that snuck into my handicap since bailing on the sport in college. I may never shoot my age, but I am shooting my weight and outdriving my eyesight.

The family morphed from three Labradors down to one Lab and two Boston Terriers. That bigger chunky one is Charley B; he was grabbed during the 2020 lockdown. The little one is Fiona. If you have never owned a Boston Terrier, you have work to do. They are amazing critters with fascinating personalities. They’re not beagles, but I’m not letting Fauci near those two guys.

Triggering Moments. This year the Klan of the Kancel Kulture was quiet but not without a few skirmishes. Cornell’s Team Reddit tried to give me guff twice but each lacked oxygen to ignite.ref 1,2 One was because I opposed double masking. (Evidence aside, Cornell kids are typically really bright.) On Twitter what clinicians call a “covert narcissist”—losers who lament that everybody undervalues them—tried to stir up trouble by creating a cancel moment.ref 3 He was met by hundreds from the Twittersphere who schooled him on why he is undervalued. Following up on my 2020 cancellation for supporting the police who knocked over the old geezer in Buffalo, a grand jury exonerated the police, and Legal Insurrection called for an apology from the Cornell administration for criticizing me.ref 4 Still having my job is adequate compensation (although I had to jab to keep it.) The Cornell Daily Sun wrote yet another “Daily Collum”, this time suggesting that my view on cops shoving wrinkly old white guys was racist, which illustrates that school newspapers are black holes for critical thinking.ref 5 Somebody filed a bias report at Cornell for retweeting an Ed Dowd tweet comparing Mitch McConnell to the Assistant Secretary of Health. I wouldn’t tap either one, to be frank. I am told six signatures were required to put that complaint to rest. Your tuition dollars at work.

I’ve read through his 2020 year in review. I heavily disagree with 95% of his views. That being said, I’m frustrated that I can understand how he came to his views, and that pisses me off. If I was a massive libertarian, I would hail him as our Lord and Savior.

~ Cornell Team Reddit

New Orleans Investment Conference. Over the last decade, I’ve participated in a few investment conferences over the years. Figure 4 shows the promo for the New Orleans Investment Conference: let’s play Name the Outlier. It was a blast, meeting up with old friends like Jim Rickards and Daniele-Dimartino Booth as well as old digital friends who finally got checked off my bucket including Jim Iourio, George Gammon, Adam Taggart, Brien Lundin, Byron King, Larry Lepard, David Tice, Brent Johnson, and Mike Larson. Chats with Jon Najarian, who gave me shit for not having wheels on my suitcase, and the legendary James Grant were to die for. I attempted to topple the $150 trillion climate-industrial complex in 20 minutes.ref 6 (I snuck jokes about Greta Thunberg and vaginal itch in the same talk.) A panel discussion with Peter Boockvar, Jim Iourio, and Grant Williams on Booms and Busts was borderline unruly. Name the outlier again. A wrap-up of Jay Martin interviews (Figure 5) finishes the Outlier Hat Trick.

Figure 4. New Orleans Investment Conference.

Figure 5. Jay Martin annual roundup. I need a professional photographer.

Podcasts. I can see the runway lights of my chemistry career dead ahead, hoping to drop into a smooth landing in four years at the ripe old age of 70 just as my last student gets his Ph.D. I’ve shaken more than a few gremlins off the wing en route. As a right-leaning libertarian academic organic chemist with a penchant for ranting unfiltered about all things political, social, and financial, my role in the podcast circuit has a different feel. There is nothing like shooting the shit with smart people. If they want to record it and put it on the internet, I’m game. I’ve done enough to realize that there are few subjects for which I lack an opinion. My reach as a nouveau pundit (ranting loon) has grown larger than my reach as an organic chemist (ranting loon).

I painted the living room today. I binged listened to your most recent podcasts and laughed my ass off while painting. You, sir, are a national treasure.

~ Robert Holmes

That was nice of you, Robert. I think the podcast host is every bit as important as the guest, and they are all different (like snowflakes). QTR podcasts with Chris Irons are always raucous because we both use F-bombs like writers use their space bars. Podcast #260 went off the rails, getting a bit more press than expected.

George Gammon and I did one after that QTR punk bailed on a putative threesome. We bonded on the idea of wealth creation versus creating fake shit from inflation. I started to lose my shit. I was in a dark place in my podcast with Kenneth Amaduri; I started to lose my shit while Kenneth found himself in the splash zone. The bitcoin hodlers seem to view me as a target of opportunity and smacked me around quite a few times. Against all logic, I read the comments section in all the podcasts (like game films) and am amazed at how listeners find one statement as an excuse to stop listening and go right to commenting. I am sure they could have found many, many more disagreeable ideas if they had hung tough. Before this document ends, I will have given everybody something to be PO’d about.

With no further ado, here is the 2021 podcast archive:

-

Max Keiser and Stacy Herbert (Keiser Report, @maxkeiser and @stacyherbert)

-

Lee Justo (Risk, @LeeJusto1)

-

Kenneth Ameduri (Crush the Street)

-

Anthony “Pomp” Pompliano (@APompliano), Spotify

-

Preston Pysh and Greg Foss (The Investor’s Podcast Network, @PrestonPysh and @FossGregfoss)

-

Jim Kunstler (Kunstlercast; @Jhkunstler)

-

Adam Taggart (Wealthion, @menlobear)

-

Phil Bak (Phil Bak Podcast, @philbak1)

-

Tom Bodrovics, (Palisades Radio, @PalisadesRadio), YouTube

-

TradeKatKnight (several behind a paywall)

-

Chris Irons (QTR Podcast, @QTRResearch) #247, #260, (YouTube #247)

-

Jason Hartman (Hartman Media parts 1651/1652, @JasonHartmanROI)

-

Tom Luongo (Gold, Goats, and Guns, @TFL1728)

-

Keyvan Davani (The Keyvan Davani Connection #155, @keyvandavani)

-

Keyvan Davani with Dylan Le Claire (The Keyvan Davani Connection #155, @keyvandavani, @DylanLeClair_)

-

Paul Eberhart (Silver Doctors, @SilverDoctors)

-

Daniela Cambone-Taub (Stansberry Research, @DanielaCambone) 1/19/21, 8/4/21

-

Tim Price and Paul Rodriguez (State of the Markets #117, @timfprice and @PRodr1guez)

-

Chris Martenson (Peak Prosperity, @chrismartenson), 12/30/20, 11/8/21

-

Sam McCullough (End of Chain; @traders_insight)

-

Tom Pochari (Destructive Capital)

-

Craig Hemke (TFMetals Podcast, @TFMetals)

-

Marty Bent (Tales from the Crypt, @MartyBent)

-

Dan Ferris (Stansberry Research, @dferris1961)

-

WallStreetSilver (@WallStreetSilv)

-

Jay Martin (Cambridge House Podcast, @JayMartinBC) 4/24/21, 7/24/21

-

George Gammon (Rebel Capitalist, @GeorgeGammon)

-

Elijah Johnson (Liberty and Finance) (copy)

-

Michael St-Pierre (Stand-Easy)

-

Justin OConnell (GoldSilverBitcoin Show, @GldSlvBtc)

-

Jaymie Icke (Ickonic, @chatwithjaymie)

-

Logan Moody (The Contrarian, @realLoganMoody)

-

Alison Morrow (@AlisonMorrowTV) (YouTube)

-

Keith McCullough (Hedgeye, @Hedgeye, @KeithMcCullough)

2021 witnessed the authorities and their media minions ball-gag those who challenged The Narrative. Ideas should be confronted, discussed, and then dealt with, not just buried. They cannot be “debunked”, because that implies they were silly at the outset. Shallow explanations for complex ideas—drought is caused by lack of rain, inflation is caused by too much money, and our response to Covid-19 is about social control—lack nuance. Shockingly, 2021 proved more depressing and disturbing than 2020, but I am still able to derive great joy in the little things in life, like imagining cutting The Most Trusted Fraud in America’s balls off with a rusty butter knife. I am reminded of the young girl in Poltergeist with otherworldly shit spewing out every window of her house, yelling “WTF is happening?” Here are few ideas that may cause you to wonder the same.

2021 was so baffling to me that I have been forced to structure this Year in Review (YIR) somewhat differently by breaking it into three parts. You are reading part 1 of the module, as they say, which focuses on the world of finance organized in relatively predictable topics. It establishes yet again my belief that the financial world is poised for a global financial crisis that will shake foundations. The then begins to grow darker. Part 2 establishes the foundations of our future that were built on the Covid Pandemic. Neither the pandemic nor our response to it is about healthcare or even getting back to normal. That section will be upload on New Year’s Eve. The grand finale to arrive in the Year of Our Lord 2022 describes the unstoppable rise of a global authoritarian state. I sure as hell hope I can finish it in time to sit back and watch. Enjoy.

Investing–Gold, Energy, and Materials

It’s batshit crazy…buy commodities, buy crypto, buy gold.

~ Paul Tudor Jones

I am a low-frequency trader, going years without marked changes in my portfolio. I camped in the ‘80s in bonds and partied like it was 1999 in the ‘90s heavily in equities with lots of tech stocks. It was my best decade for absolute returns. An abrupt and aggressive switch to cash, gold, silver, and even a small net equity short position by mid-1999 was soon followed up with a push into energy and tobacco equities in 2001. The first decade of the 2000s was, relative to the world, my best decade, compounding 13% annually from 01/01/00 through 12/31/09. Think about that one. From 01/01/10 to the present a 4% annualized return was dwarfed by the ‘roid rage of the generic equity markets. I completely failed to anticipate that the Fed would have sex with barnyard animals, and the animals would love it and gold would hate it.

I understand why I got it wrong, and I’m willing to live with that mistake.

~ Mohamed El-Erian

Although my returns integrated over the last two decades beat the S&P by a 1–2% margin annualized, it has not felt like a win for a long time. A credible 11% return in 2020 (approximately 3 annual salaries) was “consolidated” as the losers like to say with a total return of 1% in 2021. That would be OK with me if not for that awkward inflation thingie that turns it into a big loss. I am still 30%-ish precious metals, a smattering of equities, and >50% cash waiting for a rainy day during the biggest drought on record.

The supply and demand story for commodities is still superb in our work, incorporating the key elements of ESG and governmental focus on inequality, these are the early innings of a secular bull market.

~ Tony Pasquariello, Goldman Sachs

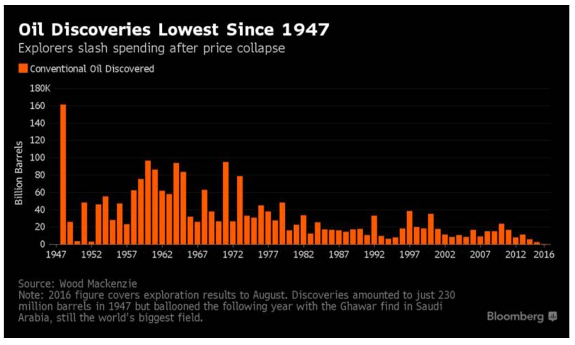

I will retire in comfort provided I don’t screw any pooches, but inflation has the pooches looking skittish. It was precisely this time last year while writing the 2020 YIR that I started to see opportunities in the old economy (energy and materials). Exxon being replaced by Salesforce.com was a bottom call (buy signal) for Exxon. That Exxon got pressured into putting two activists (wokies) on their board may be a sell signalref 1 but probably not. Jesse Felder’s howling that energy equities had dropped from 16% of the S&P 500 market cap to 2% in less than a decade was another bottom call (Figure 1).ref 2 Analyses by many including David MacKay,ref 3a,b,c whose work came highly recommended by energy security analyst Iddo Wernick,ref 4 have convinced me alternative “green” energies cannot replace fossil fuels in the foreseeable future (possibly never). Fearing a secular bear market of epic proportions, however, I remain timid (see Valuations). Jesse cautioned me not to let my macro phobias impede a good idea. Just because the world is gonna end doesn’t mean you have to be a complete pussy: man up! (paraphrased) I did and took the positions listed below along with their net returns since the date of purchase:

- Fidelity Select Gold Portfolio (FSAGX): –18%

- Fidelity Natural Resources Fund (FNARX): +1%

- Fidelity Select Energy Portfolio (FSENX): +28%

- Goehring & Rozencwajg Resources Fund (GRHIX): +4%

- Impala Platinum (IMPUY): –22%

- Jaguar Mining (JAGGF): –31%

- Kirkland Lake (KL): –9%

- Palm Valley Capital Fund Investor Class (PVCMX): 0%

- Rio Tinto (RIO): –16%

- Sibanye Stillwater Limited (SBSW): –35%

- Sprott Physical Silver Trust (PSLV): –16%

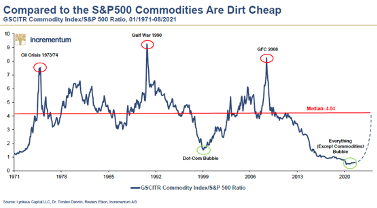

Figure 1. Relative price of commodities and the S&P 500.

The common theme of the lot is that they are all characterized by strong cash flows, decent valuations on an absolute scale, little or no debt, large dividends, and represent a commodity supercycle-inflation hedging combo platter. The large dividends render them consistent with Michael Burry’s worst-case scenario dredged up from a 20-year-old chat board post:ref 5

I generally don’t buy stocks unless I feel very comfortable coming out well in the end by just holding if all else fails.

So far so good, but did I size the bets well? Fortunately, yes. I only pushed about an annual salary’s worth of chips onto the table. For every Stan Druckenmiller able to press a good idea aggressively when it begins to move there are a thousand Dave Collums who succumb to Gambler’s Ruin with Stan’s Ford F150 tread marks across their backs. I ease into positions over months, even years. More to the point and Felder’s wisdom aside, if my macro thesis is correct (see Valuations and Broken Markets), those recent gains will be given back with room to spare. My cash position awaits prowling the battlefield, cutting rings off fingers and prying gold fillings from teeth. Greed, not fear, kept me from buying aggressively in the ’08–’09 Great Financial Crisis (GFC); the markets never got dirt cheap. I repeat: they fell a lot, but they never got cheap. I have some new strategies for grabbing the falling knife next time.

Energy stocks, specifically, haven’t been as cheap as they are today relative to the rest of the market for quite a long time.

~ Jesse Felder (@jessefelder), The Felder Reportref 6

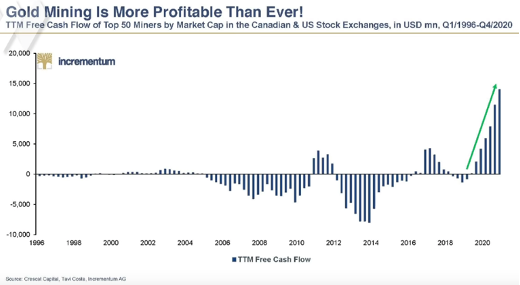

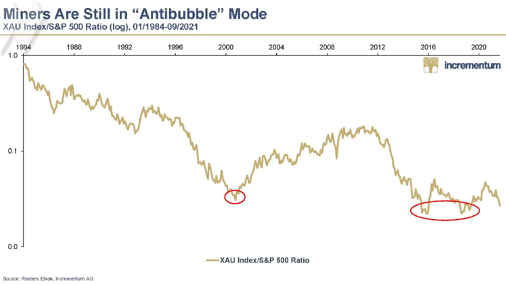

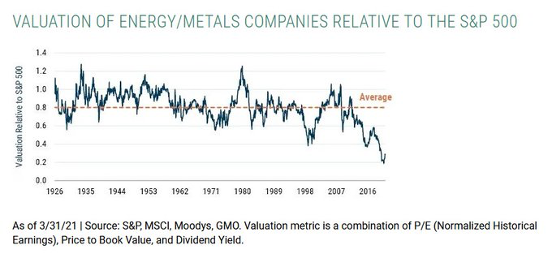

There are details beyond valuation metrics that have guided my subtle change in investing. For example, although I owned the FSAGX fund from the early 2000s until the mid-teens, I didn’t trust the gold miners: they never seemed to make money no matter how pricy gold got. Managements boned the previous bull market (Figure 2). For the intervening half-decade, I had no interest and no exposure. Squeals of miners offering optionality on gold fell on deaf ears. While I was in a slumber, however, the companies shored up their balance sheets and tightened up their management. A Fred Hickey interview convinced me they’re making good money at current gold prices (Figure 3), and they’re still hated or, as they say, under-owned (Figures 4 and 5). Kirkland Lake was a great call. Jaguar Mining, owned by Eric Sprott and recommended by James Grant, was a cheap stock with a strong balance sheet and a wholesome dividend. That one got cheaper. Maybe Brazil’s geopolitical risk is the problem. The two platinum miners (SBSW and IMPUY) also seemed like good value plays using the same meat and potato metrics while selling a commodity that has been almost entirely forgotten. They got cheaper as did platinum, but I am optimistic and have at least one smart friend providing much-needed confirmation bias.

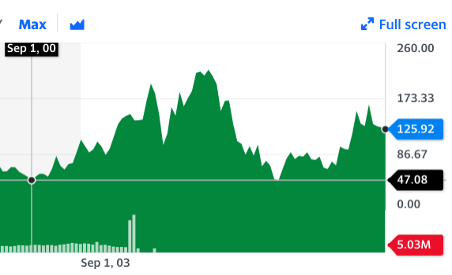

Figure 2. Philadelphia Gold and Silver Index (XAU) from 1999–2021.

Figure 3. Gold miners are making money right now.

Figure 4. Market cap of gold miners relative to the S&P 500.

Figure 5. Energy and metal company valuations. That is a factor of four off the multi-decade mean.

Figure 6. Relative performance of S&P versus commodities.

I’ll believe that oil is dead when the US military leaves the Middle East.

~ Luke Gromen (@LukeGromen), Founder of Forest for the Trees

It is difficult to understand the consequences of many near-term fossil fuel disruptions. Some were self-inflicted, such as statutory restrictions on fossil fuel production with legislators lacking any clue how to replace them (sort of like pulling the military out of Kabul first.) Detractors of fossil fuels will change their tune when their houses go cold and dark, and Teslas won’t charge. Their energy bills will be unaffordable anyway.

There is some weird stuff going on globally that is worth watching:

-

The UK shut down electric vehicle chargers over grid conflicts.ref 7 Electricity supplies are said to be heading for 4% of demand.ref 8 Headlines say the gas stations are all running out—up to 90% sold out in several major cities.ref 9 A lack of truck drivers to deliver the fuel may be temporary but not necessarily brief.

-

India’s coal plants, which normally carry 15 to 30 days’ reserves, are down to two-day supplies.ref 10

-

Saudi Arabia is aiming for 30% electric vehicles by 2030: “We want to make sure that we reduce our carbon footprint, and that’s the best way to do it.”ref 11 We know how they will generate the electricity.

-

US coal stockpiles are at 24-year lows while consumption is projected to rise 19% with output growing 10%.ref 12

-

At least one of Germany’s coal-fired plants has already run out of coal.ref 13

-

Coal is used to make solar panels. Do solar panels put out enough energy to make more solar panels?ref 14

Today, Canada moves to cap oil and gas sector emissions and ensure they decline at a pace and scale needed to achieve net-zero by 2050.

~Justin Trudeau, Prime Minister of Canada

-

China is already shutting down coal production facilities and experiencing rolling blackouts from inadequate supplies, impacting provinces representing >60% of their GDP.ref 15

-

The world’s largest coal miner, Cameco, is up 70% in 2021 riding on the back of a 150% rise in the price of coal, which may not hold. My small and antiquated Cameco position could be just getting started.

-

The Dutch intend to hold Royal Dutch Shell legally responsible for causing climate change by requiring them to reduce their carbon footprint by 45% over eight years.ref 16 The fine print leads to simple math: they are to produce 45% less oil. The nitwit activists are thrilled while screwing themselves.

The issue for oil is not demand. The supply situation is quite concerning. We’ve gone from 15 years of reserves to 10 years. We’ve seen capital expenditure go from five years ago at $400 billion a year to just $100 billion a year.

~ Jeremy Weir, Executive Chair of one of the world’s largest independent oil traders

-

There are discussions of rolling blackouts in the US. Ernie Thrasher, CEO of Xcoal Energy & Resources LLC., says that utilities “simply will have to implement blackouts this winter.” They don’t see where the fuel is coming from to meet demand, suggesting coal will be brought back into favor as natural gas prices spike.ref 17Meanwhile, coal supplies are at record lows because of statutes banning coal. “It’s going to be a challenging winter for us here in the United States.” I bought more firewood at 2.5 times the price from two years ago.

-

California’s Governor Nuisance has signed a law banning all off-road gas-powered vehicles by 2024 or whenever “feasible.”ref 18 I hope that doesn’t include diesel for the farmers’ sake.

-

California also banned high-end computers for residents.ref 19 Even in Silicon Valley? You CA voters could have solved this problem, but you left the nuisance in office.

-

The western US is suffering through what is called a catastrophic drought. Climatologists with a knowledge of history have noted that this is a regression to the mean weather of the last millennium.ref 20 No matter: Water in Lakes Powell and Mead is so low that it will force the turbines to be shut off as soon as 2023,ref 21 leading to a disastrous loss of electricity to the West. What are the global warming catastrophists doing to stop the draught and save Lakes Mead and Powell? Buying electric cars.

-

Lebanon was plunged into darkness, with the electricity grid shut down completely after the small Mediterranean country’s two main power stations ran out of fuel…in the Middle East.ref 22

-

Energy supply mishaps seem oddly common this year, including explosions in Iranian oil fields, refinery fires, and oil tanker explosions in Dubai. Nine serious oil production problems appeared in 8 days in 2021.ref 23 WTF is happening?

We’re going to end up with a real shortage of energy. And when you have a shortage; it’s just going to cost more, and it’s probably going to cost a lot more. And when that happens, you’re going to get very unhappy people around the world, in the emerging markets in particular.

~ Steve Schwarzman, Blackstone founder

My baby steps toward uranium miners are a long-term bet that we must go nuclear. The existing utilities appear to be employing a just-in-time model, depleting uranium stockpiles.ref 24 Uranium is 80% off its all-time high. The new and well-capitalized Sprott Physical Uranium Trust (URA) could change that fast by sucking up supply; they supposedly take possession, although I wouldn’t be shocked if storage fees erode returns. You can’t just put that in a safe-deposit box.

No sooner did I begin to tiptoe into the uranium miners than I noticed others were salivating. Uranium is being referred to as “the most asymmetric trade for the coming years.”ref 25 Some are claiming there could be a uranium squeeze given that the consumers are completely price-insensitive; they must buy the yellowcake. China has continued to build many new plants and is projecting to build 150.ref 26 Macron announced France would start building again,ref 27 and Finland is finishing up its fifth plant.ref 28 Japan appears to be warming to nukesref 29 years after the Fukushima disaster sent uranium miners via express elevator to the sub-basement. With little fanfare, the US Department of Energy plans to build two prototype reactors in seven years.ref 30 Note: I am 66 years old. I am supposed to be clipping coupon from bonds.

I’ve never lost a game. I’ve just run out of time.

~ Michael Jordan

My bet on nuclear and fossil fuels is, in part, a high value–low sentiment contrarian play. Low valuations and high dividends are being forfeited by Harvard’s endowment to show they are virtuous.ref 31 I am not sure how these ESG funds work, but they will eventually declare uranium green since they have long since run out of good ideas. Maybe even clean coal will get the ESG bid.

It’s necessary to some extent to restart nuclear plants that are confirmed to be safe, as we aim for carbon neutrality.

~ Taro Kano, Japan’s regulatory reform minister

Greta can squeal all she wants, but 17th-century technology (windmills) and nouveau solar technologies simply cannot put fossil fuels out of business. Period. Automakers can go fully EV if they wish, but that will not reduce the demand for fossil fuels. Fossil fuels Þ kinetic energy seems more direct than fossil fuels Þ electricity Þ kinetic energy. The 350kw generator pictured below uses 36 gallons of diesel fuel to charge a car for a 200-mile trip—5.6 miles per gallon.ref 32 The source may be loose with some of the numbers, but I checked: such a generator does indeed use that much diesel per hour. A Jefferies analysis looked at EVs under optimal conditions and noted they don’t become green until they’ve traveled 124,000 miles.ref 33

From deep within my conspiratorial mind emerged a theory about these contemporaneous supply constraints. No. Let’s call it a narrative. If I was an Overlord and needed to sell a reluctant world on nuclear power, rather than patiently waiting for the plebes to get the memo, I would engineer a fossil fuel crisis—a cataclysmic one—to usher in the New Nuclear Age. I can imagine everybody squealing, “We need nuclear power to save us!” It worked for the vaccines. Mark my words—it’s coming.

People are always asking me where the outlook is good, but that’s the wrong question. The right question is, ‘Where is the outlook most miserable?’

~ John Templeton

Gold and Silver

Europe had been suffering a shortage of gold and silver for nearly a century; mines and mints had closed down all across the continent, triggering what economic historians call ‘The Great Bullion Famine’ in the mid-1400s. To the supply of money, i.e. gold and silver, was essentially stagnant. Technically European money supply was falling, because most European kingdoms ran a trade deficit with Asia and the Middle East.

~ Wikipedia on the Great Bullion Famine

Wiki’s last line is the money shot: they had a trade-balance problem, not a money problem. The Fed governors are too preoccupied with jumping from chair-to-chair to avoid the lava on the floor to get that stuff. Inflation yearned for by the Fed has finally made landfall and will be discussed below. But first, let’s ignore the price of gold and all those Tanya-Harding moments and gander at the guts of the gold market this year. The Hulbert news service metric for interest in the subject suggests there is none, except for maybe Ronald Stoeferle, Mark Vale, and the other Eurowizzes at Incrementum, who do a brilliant job of analyzing the gold market.ref 1

White House economists are assuming negative real interest rates all the way through the end of the 10-year budget window in 2031.

~ The Wall Street Journal editorial board

If this is the case, then none of us own enough gold.

~ Jesse Felder (@jessefelder), The Felder Report

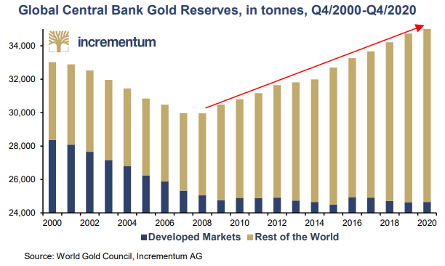

Central Bank Accumulation. The bullies at the central banks net buyers for quite a few years (Figure 1). China upped the allocation allowable to be held by domestic banks tenfold.ref 2a,b Russia’s gold reserves surpassed its dollar reserves for the first time in history,ref 3 and they authorized their National Wealth Fund (NWF) to buy gold.ref 4Hungary tripled its sovereign stash to 94.5 tonnes,ref 5 which is a ton(ne) of gold given it had only three in 2018. (Iowa joined in with the other third-world guys to allow their state treasury to buy gold too.)ref 6 In a funny WTF moment, the New York Fed discovered 1,731 bars of Afghan gold that had been stuffed in some dark corner since 1939.ref 7 The bars are “a bit irregular and not up to specs” with “cracks, fissures, and holes”, so they generously offered to hang onto them until they can be cleaned up for the Taliban or until hell freezes over. There may come a time when the accumulation of gold migrating to Asia becomes a black-swan-level plot thickener—the Great Bullion Famine 2.0.

Figure 1. Central bank gold accumulation.

If gold is gonna move East somebody has to sell it. Macron announced a sale of bullion to help finance aid for Africa.ref 8 That kind of thinking worked so well for the Bank of England, and, by the way, does he think we are that stupid to buy a narrative about aid for Africa? Do these guys ever stop lying?

The OTC market is where truth and transparency went to die, and scheming, front-running, and price-fixing options (forwards, swaps, and credits) went to the moon.

~ Matthew Piepenburg

Chaos at the COMEX. The Commodity Exchange (COMEX) is the paper gold market where monkeys go to get hammered. Forget about price suppression. It is about getting shitfaced around the campfire and skinning your retail captives alive. There are times, however, when there is a sense of bailout in the air, like when a $55 three-day price rise was met with a wall of 45,858 newly minted COMEX gold contracts worth billions in the air-pocket-rich wee hours of the morning, all to make sure supply and demand meet at a much lower price.ref 9 Somebody referred to it as selling precious gems on eBay at 3:00 AM. In the equity markets, the common practice of naked shorting is at least illegal in the abstract. Without the help from overnight sellers, there might have been a lot of chalk outlines. The longstanding court case against Bank of America and Morgan Stanley for manipulating the metal futures market got dismissed. I’m shocked.

There was a whiff excitement when Basel III banking regulations stepped up to become the cop in the gold market.ref 10Although not a universally held belief, some speculated the changes in the rules would put the London Bullion Metals Association (LBMA) out of business by putting a foot on the throat of the paper market.ref 11 The paper market is equivalent to the 8,500-ton US gold hoard, but without the gold, of course.ref 12 The Bank of International Settlements (BIS) introduced the “Net Stable Funding Requirement” that would prevent the creation of fictional gold, silver, and many other commodities through ledger entries and blaming it on the Americans for risking another Lehman Brothers-like collapse.ref 13 The new rules imply that gold must be fully allocated (not fake) to be classified as a zero-risk asset. It is designed to “prevent dealers and banks from simply saying they have the gold, or having more than one owner for the gold they have” by making banks hold reserves against their paper gold.ref 14 No more of this unsecured creditor crap and rehypothecation, guys. Groups like the London Precious Metals Clearing Limited created by the LBMA to clear and settle transactions are bloated with unallocated fake metal.ref 15 Will this lead to the collapse of the London derivatives market and cheers of good riddance? On the general principle that nothing impedes determined financiers made that unlikely, and the price of gold seemed to agree. Alas, the Brits bailed on the Basel III rules,ref 16 which I imagine mucks up any pressure on the LBMA. What did you expect?

My silver’s about to get squeezed

All physical owners are pleased

The autists on Reddit

Are starting to get it

Our fiat is flawed and diseased~ The Limerick King (@TheLimerickKing)

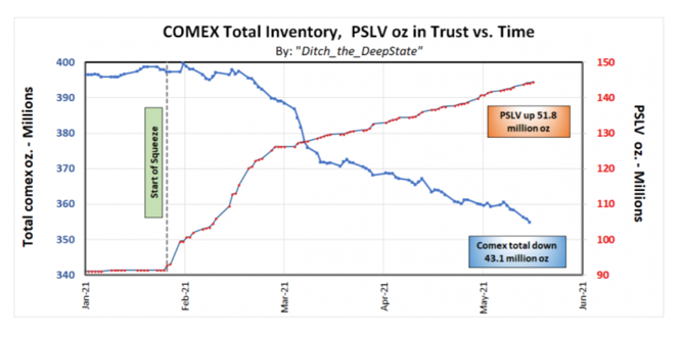

The Great Silver Squeeze. Some think the demise of the silver futures market is inevitable as the insolvency of the COMEX silver stash is revealed. The Perth Mint in Australia is also suggested to be both fractional reserve and insolvent.ref 17 It got exciting when the WallStreetBets Reddit crowd—a bunch of retail crazies referred to as a distributed hedge fund—got the scent and decided they would squeeze the silver shorts in the spirit of the meme stocks (see Broken Markets). In this case, the squeeze would occur by taking possession of the physical metal from highly leveraged, fractional-reserve silver at the COMEX. The Squeeze was to commence in January, which means well before that. Reports of coin shortages at the mints despite increased production suggested an elevated demand for physical metal.ref 18 The New York Times called it a global silver shortage,ref 19 but I suspect it was only a shortage of silver rounds used to produce one-ounce sovereigns. Huge (20%+) premiums were showing up at Apmex and the most retail sites like eBay. The Sprott Physical Silver Trust (PSLV) has witnessed large inflows this year (Figure 2). Unlike iShares Silver Trust (SLV), which seems to run a fractional silver reserve, PSLV removes silver from the marketplace by taking possession.ref 20 Some say the PSLV silver will never re-enter the marketplace. Forever is a long, long time.

Figure 2. PSLV holdings vs COMEX holdings

Of course, there was pushback. On Day 1 of the squeeze, the CME Group tamped down speculation by raising margins on silver futures 18%, declaring the decision was based on “the normal review of market volatility to ensure adequate collateral coverage.”ref 21 Silver immediately took a 2% hit from the still lofty $29 price tag. Mysterious Reddit outages occurred on Sunday night preceding the squeeze.ref 22 There was some suspiciously intense selling immediately into the squeeze,ref 23 but that could have been a “buy the rumor, sell the news” moment. A fat-finger error by the LBMA overcounted the total tonnage of silver in storage by 100 million ounces, representing a rise in the inventory that was five times the previous month-over-month record.ref 24 You had one job guys—no, not counting the ounces right—protecting big money. High five! A few weeks later they quietly announced, “We fucked up. Sorry about that. And, anyway, you all should know the adage, ‘there is no ‘f’ in silver.’”ref 25

The SLV prospectus states, “No shares are issued unless and until the Custodian has informed the Trustee that it has allocated to the Trust’s account the corresponding amount of silver.” Well they issued a bunch anyway, and they also changed the prospectus:ref 26

The demand for silver may temporarily exceed available supply that is acceptable for delivery to the Trust, which may adversely affect an investment in the Shares…Authorized Participants may not be able to readily acquire sufficient amounts of silver necessary for the creation of a Basket…In such circumstances, the Trust may suspend or restrict the issuance of Baskets. Such occurrence may lead to further volatility in Share price and deviations, which may be significant, in the market price of the Shares relative to the NAV.

SLV also came out with other warnings out of concern for the defenseless hedge funds:ref 27

As of the date of this prospectus, an online campaign intended to harm hedge funds and large banks is encouraging retail investors to purchase silver and shares of Silver ETPs to intentionally increase prices. This activity may result in temporarily high prices of silver…The campaign encourages retail investors to purchase shares of Silver ETPs as well as physical silver in order to intentionally create a short squeeze. This activity could result in temporarily inflated prices of Shares and the difference between trading price and NAV per share may widen.

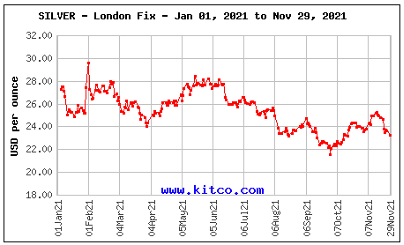

Given that silver in London was in the wrong legal form, there were pickles being shit that demand in markets remote from London would overwhelm the system. Not a problem. In a relatively obscure interview, Rostin Behnam, the US CFTC regulator, said that COMEX was able to “tamp down what could have been a much worse situation in the silver market.”ref 28 I did not know that was your job but thank God. Phew. Serious silver players say the squeeze is not over, just slowly grinding down the paper market to dysfunction.ref 29 What I can say is that the price is lower today than the day the squeeze began (Figure 3). That gentle drift downward conceals some stunning drive-by shootings. I was buying silver at $3.50/oz and am now waiting for the next bottle rocket to be lit.

Figure 3. 2021 silver price.

Next time you want to squeeze something, try cantaloupes. On a personal note, somebody made a meme of the The Great Silver Squeeze that included all the cool kids.ref 30 I made it into my first meme! Someday it will be like watching my first porn flick with my great grandchildren and saying, “Damn: The camera makes me look fat!”

The Economy

All the king’s horses and all the king’s men

couldn’t put Humpty together again.

Deferred GDP. A Harvard study estimated the Covid-19 lockdown cost the US $16 trillion.ref 1 Year-over-year (yoy) comparisons of 2021 to 2020 are nearly worthless because of the “base effect” (bad comps). To keep the math simple, imagine you collapsed the economy in 2020 by 50% relative to 2019—we did shut the whole thing down, FFS. You need a 100% growth from 2020–2021 just to return to normal. Some pundits claim we now have a strong economy—a Goldilocks economy!—with a tight labor market. With all disrespect, I see a fractured economy with a dysfunctional labor market.

Despite progress the economy still sucks. We exited the recession in record time thanks to aggressive Fed policy, right? Tell a golfer they are out of the sandtrap because they are on the upslope and watch where they plant their sand wedge. If you are going to say it is over when you hit bottom, call it something like a “skid”, not a recession or depression. Occasionally somebody distinguishes “recovery” from “expansion”, but for the most part propagandists simply blow the all-clear whistle as the first derivative turns positive. Yay.

These are just jobs that are being restored. It’s not like we have this vibrant economy and we’re starting up all these new businesses. These are businesses that were ordered to close down, and now they’re reopening. So, that’s all we’re doing is getting back all these jobs that we lost. Nothing here is being created.

~ Peter Schiff (@PeterSchiff), Europacific Capital

This year’s debt buildup in the US has funded zero new productive investments. No roads, no airports, railroads, nothing.

~ Louis Gave (@Gavekal), Gavekal.

In comparison with the economy, the S&P is on fire. We will by definition give that back. (See Valuations.) Equity markets cannot sustainably outgrow the economy. Somebody noted that NYC is 8% of the US GDP. What does that little oasis of money velocity actually produce? China was the only major economy to grow in 2020 by producing what we called in the olden days ‘products’, the ‘P’ in GDP, and even those guys may be in a “skid.”

If people don’t make stuff, nobody has stuff.

~ Elon Musk (@elonmusk), Rocket Surgeon

According to the Annual Threat Assessment,ref 2 whose name alone sounds bad, the pandemic will bring 20 years of “humanitarian and economic crises, political unrest, and geopolitical competition [that will] strain governments and societies. The economic fallout from the pandemic is likely to create or worsen instability in at least a few—and perhaps many—countries, as people grow more desperate in the face of interlocking pressures that include sustained economic downturns, job losses, and disrupted supply chains.” That doesn’t sound like a booming economy. Somebody has been reading The Fourth Turning.

When the pandemic passes, and we are able to look back on the experience without fear or political bias, it will be clear that the lockdowns were one of the greatest economic blunders in history.

~ Jim Rickards (@JamesGRickards), prolific author and thought leader

Returning to the always-grounded Lacy Hunt, “the massive void in economic activity and destruction of wealth created by the virus and related shutdowns of businesses in the U.S. and abroad will take years to fill.”ref 3 From David “Rosie” Rosenberg we get, “Achieving the level of pre-crisis activity will, in fact, require years, owing to the wealth destruction.” But we have so many savings, Rosie! According to the Bureau of Economic Analysis (BEA), the excess savings accrued from government largesse—I bet Lacy wouldn’t call them savings—seeded only a bumper crop of couch potatoes and is almost gone.ref 4 A poll showed that 18 to 34-year-olds are now evenly split on negative and positive views of capitalism,ref 5 and the trend is global. A generation of Marxists ought to power wealth creation going forward, eh?

When one nets out all the assets and liabilities in the economy, the only thing left—the true basis of a society’s net worth—is the stock of real investment that it has accumulated as a result of prior saving, and its unused endowment of resources.

~ John Hussman, (@hussmanjp), Hussman Funds

Contrary to popular opinion inside the corridors of the Eccles Building, you cannot print real GDP. And you can’t destroy all those mom-and-pop businesses and still have a booming economy. It doesn’t pass the smell test. Just wait. The authorities haven’t even lifted all the arbitrarily imposed and largely unconstitutional rent controls and eviction moratoria yet.ref 6a,b We don’t know how many more failures are in the queue. More than 100,000 restaurants went belly up because of lockdowns, and 500,000 are said to be in “free-fall.”ref 7 Technically speaking, (Restaurants are more likely to “go up in flames.”) A documentary describes the plight of those who spent thousands to create an outdoor dining experience only to have the rules changed.ref 8

Sorry to keep interrupting here, but Hayek noted that the markets can deal with arbitary and even capricious rules but struggle with rule changes. The stage is still set for a commercial real estate disaster. I walked through our mall, not exactly mom-and-pop operations I hasten to add, and it was 20% occupancy. The only survivors were stores that could stand alone without foot traffic of a mall. Where are the hundreds of workers? Jingle mail is back: REITs are mailing in keys to malls. Simon Property Group walked from a $300 million mortgage on a commercial property.ref 9 At the auction, there was no interest with an opening bid of $130 million. Neither money printing nor bailouts nor all the king’s horses and all the king’s men will reassemble these broken pieces. I am not saying we will never recover—we will—but timing is everything. That post-Roman-Empire period often called the Dark Ages got a little old. (OK. That’shyperbolic.)

Here is a plot thickener:

After years of beating brick-and-mortar retailers black and blue, Amazon is ready to try and beat Macy’s, Target and Wal-Mart at their own game. According to WSJ, Amazon is reportedly planning to delve into the department store game by opening a flurry of 30,000-square-foot facilities, starting in “test” markets like Ohio and California.ref 10

~ Zerohedge channeling the Wall Street Journal

I knew this was coming. Ask yourself: Did Bezos and others with durable lockdown business models have a say in how the lockdowns were to be achieved? As wealth inequality continues to grow; we should just call it “economic distancing.”

I don’t want small businesses that are underpaying employees.

~ Representative Ro Khanna, Marxist Wing of the Democratic Party

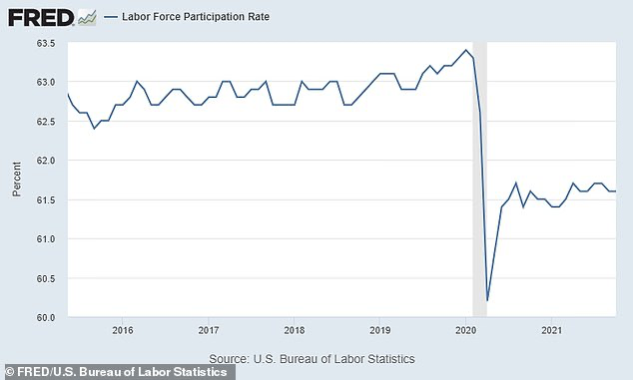

Broken Businesses. What about that data showing unemployment is in the 4% zone? Look at the labor participation rate (Figure 1). The number of Americans quitting their jobs has reached a 20-year high.ref 11 Nutcases like Janet Yellen call these “quits” and consider them emblematic of a healthy job market with lots of choices. To blame it on the generous payouts in the US is also a shallow analysis: A survey of 45,000 employers in 43 countries showed 69 percent had hiring problems.ref 12 Something else is at play. I asked the Twitter-sphere if anybody had immediate family members working before but not after the lockdown and to explain. The reasoning covered a wide, generally dark, swath: “fuck this”, “not paid enough”, “got fired because of jab mandates”, “job sucked”, and “stayed home because of the locked-down rug rats and never went back.”) Some described doing with less. That could start trending.

Figure 1. Labor force participation rate.

Over the past 20 years, the US had no net job creation for folks aged 16–59. The 10 million net increase in US payrolls from 2000–2020 was due to folks aged 60 and older. Unintuitive fact of the day.

~ Lyn Alden (@LynAldenContact), Founder of Lyn Alden Investment Strategy

A poll claimed that Americans are more optimistic than they’ve been in many years.ref 13 That is some magical polling. Pew Research Center reports a chronic lack of motivation by remote workers, especially young adults.ref 14 They are phoning it in. Analyst Peter Saleh sees the job market as severely destructive, keeping an entire generation away from the workforce for too long while they live under their parents’ floor (in the basement.) I’ve alluded in the past to studies showing irreparable financial and professional damage done when young entrants to the workforce confront an economic downturn during those formative years.

That BK tweet predictably bombed. Meanwhile, you have barkeaters in Portland, OR considering a ban on goods and services from Texas to stand firm against their abortion law.ref 15 I understand you have virtue to be signaled for all the world to see. The rest of the country will buy ‘em, especially if we get shortages. In a compelling sign of Biden’s dementia (like we are short of those), he is trying to block workers from entering a broken labor market because of their vaccine status. At the time of this writing, the unvaccinated holdouts are Alamo-strong. Goldman analysts optimistically estimate “only 7 million” workers will hold firm—only 7 friggin’ million.ref 16 Mark my words: Historians will destroy this administration for their draconian policies.

If the part that blew out is 0.1% of the entire machine, and the other 99.9% still works perfectly, the entire machine is still dead in the water without that critical component. That is a pretty good definition of systemic vulnerability and fragility, a fragility that becomes much, much worse if there are two or three components which are on indefinite back order.

~ Charles Hugh Smith (@chsm1th), OfTwoMinds blog

Broken Supply Chains. Just-in-time inventory management has given way to a there’s-no-fucking-parts problem. I have spent enormous energy trying to decipher the source of the broken supply chains by reaching out to those much smarter than I. I asked Twitter for examples of supply problems and got a blast from the fire hydrant. In short, an economy is a complex machine that doesn’t run well if you start removing parts. For the first time in decades, having the money does not guarantee access to the goods. Transportation Secretary Pete Buttigieg admitted challenges will be “going into the long term.”

Truck drivers are akin to the missing honey bees; where did they go and how do we function without them? A (smart) truck driver told me that the pay sucks; it’s a “sweatshop on wheels.” Delays at the docks went from three-hours to three-days. When you are paid by the job, that is intolerable; you quit. He said many drivers on the top end demographically (grumpy old farts) simply retired, and generous signing bonuses are not bringing them back. Truck driving was a precarious and undependable job before the pandemic. California labor laws are nightmarishly inflexible (ostensibly to protect workers), making it impossible to call audibles at the line of scrimmage to problem solve. An estimated 40% of all imports come through Long Beach and Los Angeles,ref 17 and they are failing to unload the containers and dispense with the empties, creating California’s ultimate recycling problem. Shipping companies are also using jingle-mail, abandoning their mounting debts, their vessels, and even their onboard crews without adequate food.ref 18 It must be tempting to beach the ships and hop off.

How does any normal human being become a scientist and have zero understanding of how an economy works, or what damage shutdowns, zoom school and trillions in government spending actually mean for people? I mean, what kind of scientist is that?

~ Brian Wesbury (@wesbury), Chief Economist, First Trust Portfolios

Even the fast-food chains were having trouble sourcing key foods and packaging materials. Food supplier Sysco couldn’t get truck drivers. The Road Warrior model got real as truckers started repairing their trucks by cannibalizing other trucks for parts. Semiconductor shortages remind us that everything has chips and won’t work without them. Drought, rolling blackouts, and earthquakes in the semi-conductor capital of the world, Taiwan, were “terrorizing the island.”ref 19 Imagine what a hostile takeover by China would do.

Get this…Hearing similar issues with LA Port supply chains. Company has semis that need a specific sensor to run. Trucks sidelined and will not run without sensor. Also…These trucks are used to take containers from the Port in LA. Recursive systematic collapse.

~ Chris Close (@soclose2me)

Recall the allusion to energy-supply mishaps that seemed eerily common this year. There have been a number of other disruptions. JBS Meat plants got hit by ransomware, jeopardizing key food supplies.ref 20 Turkey’s Bosphorus Strait got clogged by a crude tanker.ref 21 An estimated 800 barges got stuck in the Mississippi River because of a cracked bridge.ref 22 Ireland’s Health IT system got hacked.ref 23 (The hacking community thinks these are CIA operations.)ref 24The Suez Canal got blocked, stalling an estimated $400 million per hour in goods.ref 25 It’s hard to say if this is my hypersensitive awareness of normal systems prone to Murphy’s Law or if something else is at play. (Enough foreshadowing, Dave.)

Inflation

During this time of reopening, we are likely to see some upward pressure on prices…But those pressures are likely to be temporary as they are associated with the reopening process.

~ Jerome Powell, Chair of FOMC

Inflation isn’t transitory.

~ Paul Tudor Jones (@ptj_official), Gazillionaire Founder of Tudor Investment Corp

On an absolute basis, [inflation] mentions skyrocketed to near-record highs from 2011, pointing to, at the very least, “transitory” hyperinflation ahead.

~ Bank of America analyst

Transitory hyperinflation? Thermonuclear war is transitory too. We’re always told that inflation is too much money chasing too few goods, but let’s try inserting the probe a bit deeper given the stakes. Everybody’s favorite model is that inflation is here, real, and anything but transitory. Simpletons will declare that can’t be right because the majority is never right. I am sympathetic to that idea—they are often wrong—but, unlike market sentiment indicators from whence this contrary notion emerges, uniformly high inflation expectations correlate with uniformly high inflation. That is when the Fed’s inflationary boosters against every and all market dips have been transcribed into society’s DNA. A recent poll showed that 87% of Americans are worried about inflation. That’s a DNA-level problem because they start adapting to it in highly inflationary ways. Once the inflationary mindset has a firm grip, it will require a Volcker-esque leader to adjust attitudes by beating us with a stick ignoring the rule of thumb.ref 1

The truth is that we know very little about inflation, including its causes and cures. I describe it as mysterious, so I believe we should put even less stock in predictions surrounding inflation than in other areas.

~ Howard Marks (@HowardMarksBook), found of Oaktree Capital Management

Pondering this new inflationary world demands we pretend the CPI and PPI chain-weighted, hedonically-adjusted, malarkey-infested stats are non-fiction, which forces us to turn to anecdotal information. This year poses special problems because of goofy year-over-year comparisons—the so-called “base effect.” Sane economists realize 2020 is a dysfunctional benchmark and turn to month-over-month metrics instead. Even so, the low-balled CPI and PPI came roaring in at high single-digit values even using month-over-month comparisons. The inflation debate remains a complex story, which I will ponder if only to collect my thoughts.

Have we ever seen a country in history persistently running a broad money growth rate at 10% that didn’t have inflation at 4% or above? The answer is no.

~ Russell Napier, recovered deflationist/author, ERIC Electronic Research

Inflation-Deflation Debate. Aside from asset deflationists, of which there are potentially many, the macroeconomists predicting old-school deflation were restricted to diehards like Lacy Hunt, Russell Napier, and Mish Shedlock. Well, we lost Napier this year; he thinks the inflation boogieman has been released.ref 2 To paraphrase and summarize, Russell sees financial repression-adjusted (real) bond yields staying deeply negative for a decade or two. This would be akin to the post-WWII era but lacking the wonderful post-war economy and equity valuations rising threefold in two decades to pick up the slack for disastrous returns on fixed income. Inflation is and will be exacerbated by supply shortages and loss of the disinflationary tailwind as China starts demanding market prices for their goods. There will be no last-call on binges caused by Government-backed bank loans and imposed “politically directed growth” (Green New Deals). It’s a 24–7 casino. The fun early phases of financial repression witnessing equities, bonds, and real estate getting bids will give way to the fugly economy-choking stagflationary downside. Napier underscores contractors pre-buying materials for future use as a textbook case of rising money velocity. He concedes that projecting money velocity is “like trying to juggle an incontinent squid: Something you really don’t want to do, and you’re very unlikely to be successful.” For me, the Napier money shot—cover your faces—is that he thinks the Fed has turned the bond market over to the government, which will force bond purchases through statutory control discussed in previous YIRs. And we all know that government programs never end.

We simply do not have the resources to fund ourselves and to obtain a higher standard of living, which means that the economy will falter as we go forward, inflation will move lower.

~ Lacy Hunt, the legend from Hoisington Investment Management

Lacy Hunt’s analyses are so deep my brain aches.ref 3 His base case is and has been for many years that a stagnating economy will create deflationary drag. Contrary to sell-side equity analysts, Lacy notes that the economy has been sucking balls (paraphrased) for while now as indicated by flat corporate profits and flat per capita GDP over the last decade. He knows his history, and history shows growth is stifled as you struggle to burn off debt. I wonder, however, when this debt roast is to commence. When will the rate of debt accrual shrink relative to GDP and bring the 40-year bond bull market to a timely death? We all gained from bond portfolios rising with dropping rates, but now interest rates are at lows not seen since the Lydians made the first gold coin. The duration risk—the risk that your bond portfolio will hand your ass to you if rates flicker upwards—is now epic.ref 4 That flashing red LED clock is counting down toward zero. For the time being, Lacy hangs onto a deflationary-disinflationary model with the proviso that if the Fed starts monetizing debt in earnest that he would switch teams (flip the game board over and stomp away in disgust).

Inflation is nonlinear…as human perceptions and forward beliefs become more attuned to the notion that inflation is coming, self-reinforcement causes rapidly increasing acceleration of both velocity and inflation….Policymakers always think they can control inflation before it surges beyond their control. History indicates otherwise.

~ Paul Singer, Elliott Management

The inflation-deflation debate is complicated by the tail risk of a catastrophic deflationary-like credit and asset collapse disrupting an otherwise compelling inflation narrative. Possible price changes in risk assets are covered in lurid detail in the Valuations and Broken Markets sections. A collapse in these markets would cause the “wealth effect” —consumers’ responding to their perceived wealth hyped by the Fed as a miracle of their monetary policy—could do a clutch-free flip into reverse. Such a collapse in consumer durability does not necessarily mean that prices of critical goods can’t keep rising. This already allows talking heads to breathlessly exclaim that retail sales are rising as consumers are forced to pay more for essential goods.

There is one type of inflation that the Fed has never had control over…inflation that is caused by shortages and supply shocks.

~ Daniel Amerman (@DanielAmerman1), financial analyst and author

Supply Shocks. The inflation story rode in on the backs of shortages although causality is not that simple. First-world consumers have not seen an inflationary supply shock of since the oil embargoes of the Carter era, and they have never witnessed the fractured supply chains and wholesale shortages in all goods across both the old and new economies. If spiking lumber prices throttle home construction, one can imagine the price of existing homes will be climbing markedly too. The broken labor markets are driving up labor costs profoundly. Locking everything down did not help produce anything.

Oh boy, we’re seeing it all over the place. You read about lumber prices, but we’re seeing it in all of our businesses. The obvious bottlenecks in the supply chain arena are pushing up prices. It’s very reminiscent of the ‘70s.

~ Sam Zell, real estate titan, on inflation

Most people haven’t had a forty-plus-year career, and they’ve only seen declining inflation over the last 30-plus years. So this is going to be a pretty big shock.

~ Larry Fink, CEO of Blackrock

Constraints on energy and food production—euphemistically called energy and food insecurity—could emerge in the winter of 2021–22. How does one calculate the inflationary effects of goods and services that are no longer available at any price? Many think central banks print money—that is debatable—but they sure as hell can’t print widgets or real GDP.

Policymakers’ defense of their current monetary policy stance is no longer credible.

~ John Carson, former Chief Economist at Alliance Bernstein

I think these are the least responsible macroeconomic policies we’ve had in the last 40 years.

~ Larry Summers

The real danger is that the longer the supply bottlenecks and attendant price pressures last, the more likely they will shape the expectations of consumers and businesspeople, shifting their views on pricing and wages in particular.

~ Raphael Bostic (@RaphaelBostic), Atlanta Fed president