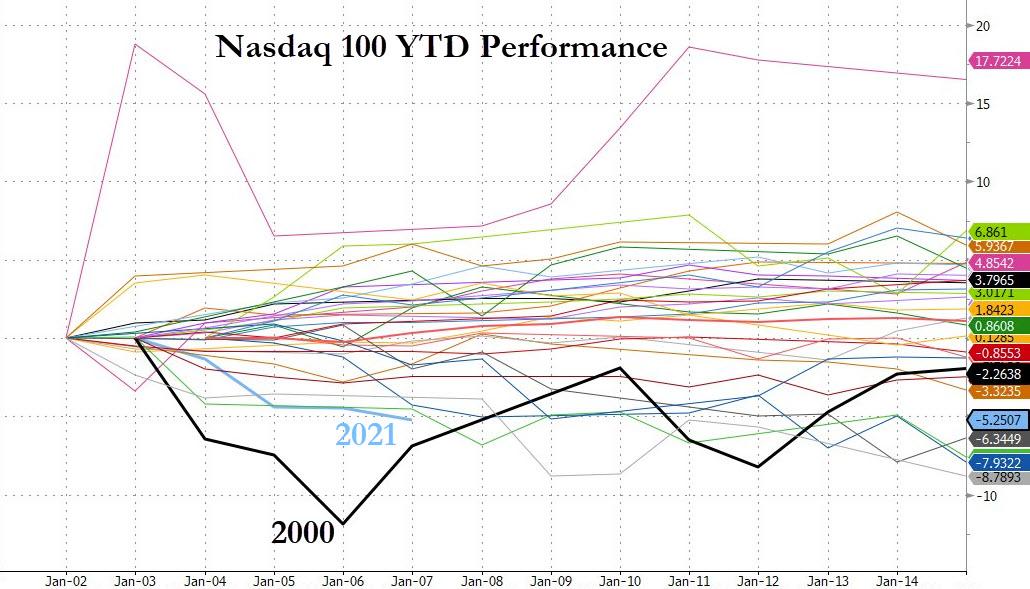

Nasdaq 100 Suffers Worst Start To Year Since 2000; Rates & Risk-Parity Routed

Investors appear to be starting the year with an aversion to long duration stocks and instead are leaning into Value stocks with closer ties to an economic recovery. Growth stocks fell to a key technical level this week relative to Value stocks…

Source: Bloomberg

Nasdaq down 7 of the last 8 days and was by far the week’s worst performer as The Dow clung to unchanged on the year today (but faded into the close to end red like the rest). The S&P ended down 2% and Small Caps down 3% on the week. That is Nasdaq’s worst week since Feb 2021…

“Many retail investors have arguably too high exposure to speculative growth equities and thus they have high interest rate exposure without knowing it,” writes Peter Garnry, Saxo Bank’s head of equity strategy.

“As we have said for a year now, it is wise to begin balancing the portfolio blending growth with more low equity duration assets and especially those with supposedly inflation hedging capabilities.”

For context, this is the worst start to a year for the Nasdaq 100 since 2000…

Source: Bloomberg

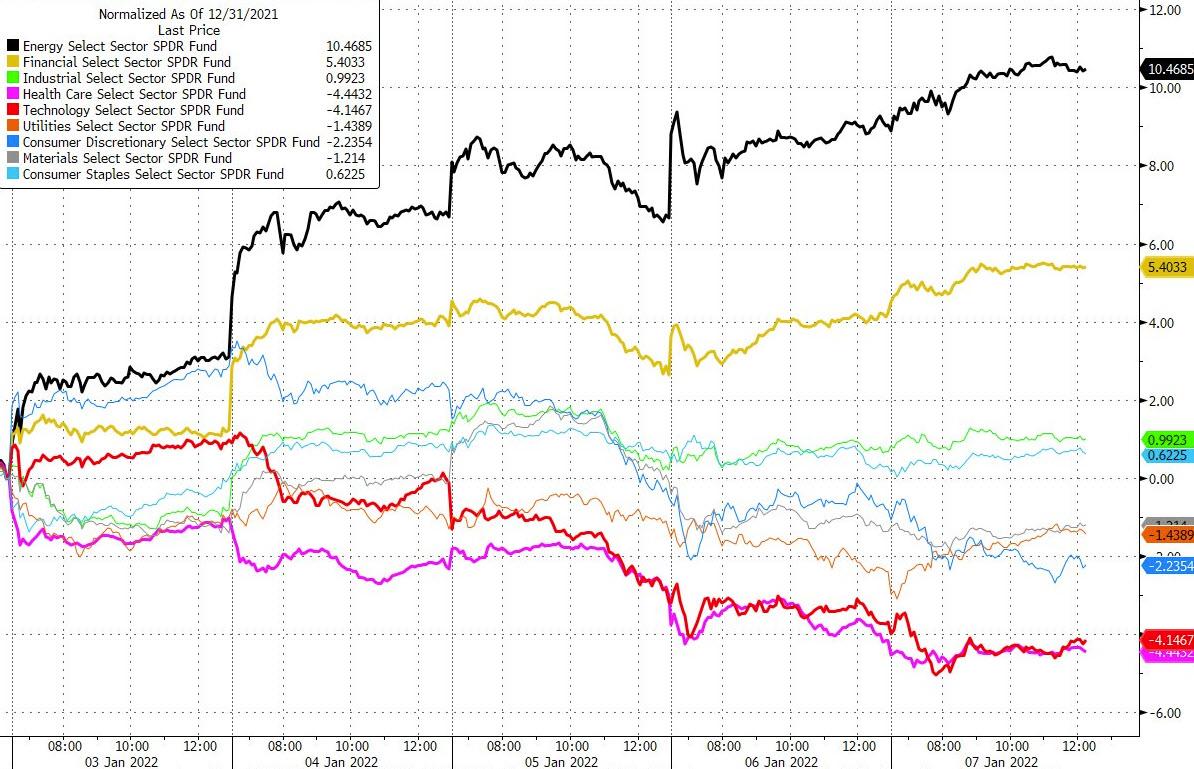

Energy and Financials outperformed this week as Tech and Healthcare lagged…

Source: Bloomberg

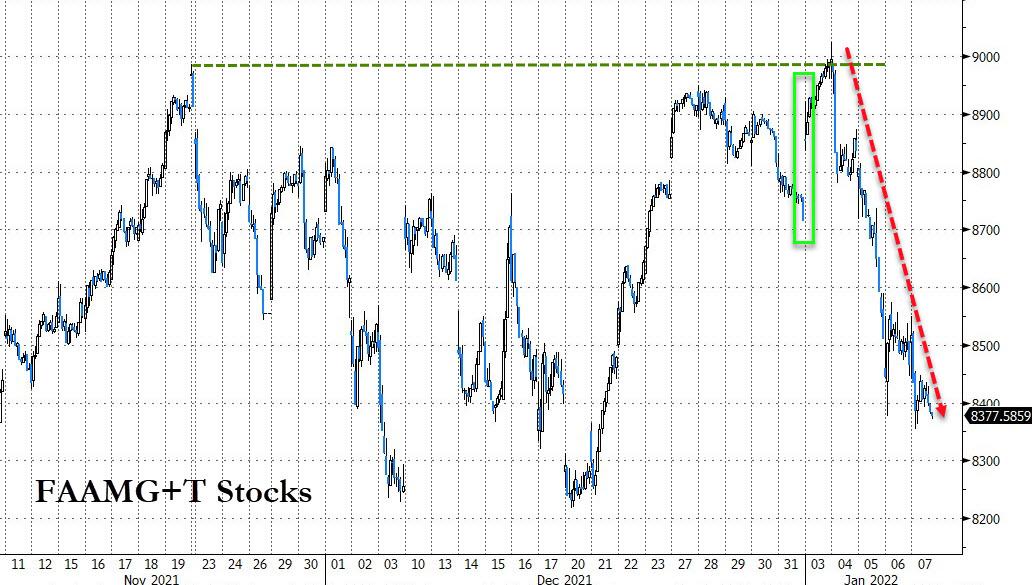

FAAMG+T Stocks (which represent 25%+ of the S&P 500 market cap) were a disastrophe this week…

Source: Bloomberg

Erasing all the Santa Claus rally…

Nasdaq Biotech Index is on track to close 5.8% lower in its worst weekly drop since March 2020, breaking below key support back to Dec 2020…

Source: Bloomberg

The S&P Airlines Index rose over 7% this week – its best week since early November – as Omicron anxiety began to fade and several nations lifted travel restrictions…

Source: Bloomberg

Risk-Parity and vol-focused funds were clubbed like a baby seal this week with one example, RPAR, suffering its biggest weekly drop since the COVID collapse in March 2020..

This helps explain why both bonds and stocks were hammered (obviously along with the hawkish tilt from policymakers) as RP funds force-delevered. The start of 2022 saw the worst aggregate weekly loss for bonds and stocks since the market carnage in March 2020…

Source: Bloomberg

On the bond side of the world, it was a bloodbath with the belly clubbed like a baby seal (7Y +26bps on the week, 2Y +13bps, 30Y +20bps)…

Source: Bloomberg

The 10Y Yield broke out to its highest in 2 years while 30Y remains below the Oct 2021 highs for now…

Source: Bloomberg

U.S. interest-rate swap spreads were wider across the curve today as corporate treasurers braced for another swath of high-grade corporate supply while money managers hedge interest-rate risk. That widening kept pressure on Treasuries. Higher rates inspired corporate borrowers to pay in 30-year swaps and sell cash bonds about 30 minutes after the December labor market data. That means they are locking in rates in the long-end ahead of future issuance. Next week’s issuance is expected at ~$30b, but if this week’s more than $60b in issuance is any guide, that number is likely to rise, especially given the increase in borrowing rates.

All of which explains why the yield curve suddenly flipped from flattening (a fundamental-based move driven by policy-error fears) after the payrolls print to steepening – a technically-driven move…

Source: Bloomberg

Notably, after 2 last peaks in COVID-19 cases, 10-year yields jumped 50-60bps following 3 months…

Source: Bloomberg

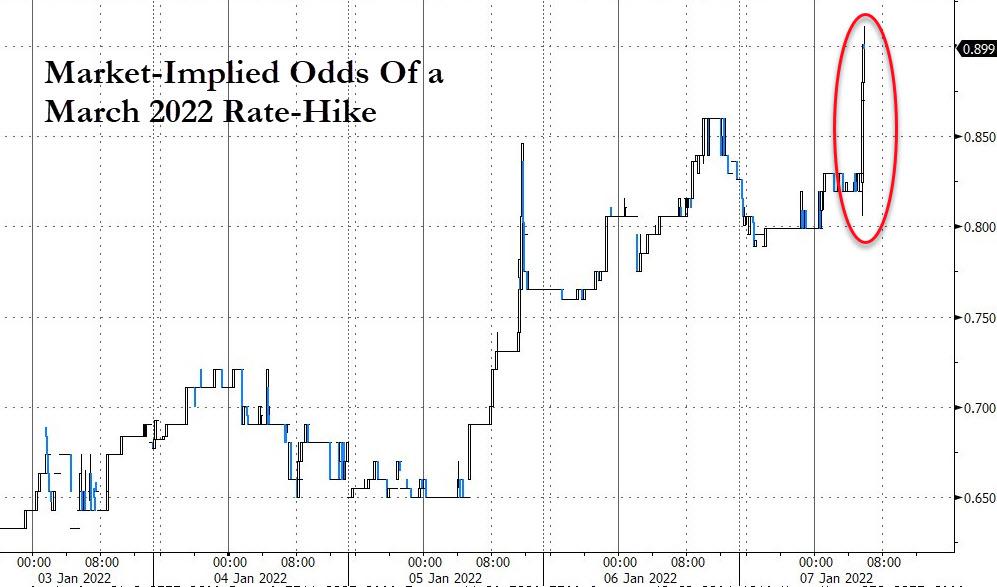

This morning’s sent STIRs soaring, pushing the odds of a March 2022 rate-hike above 90%! and a 50% chance of a 4th rate-hike by Dec 2022…

Source: Bloomberg

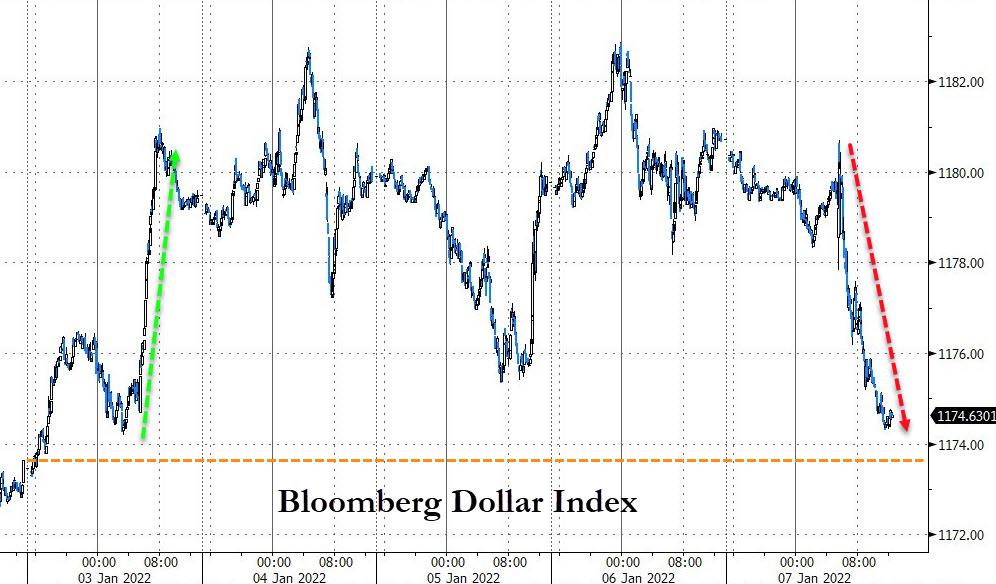

The dollar ended the week only marginally higher, oddly giving the week’s gains back today after the ‘hawkish’ jobs data…

Source: Bloomberg

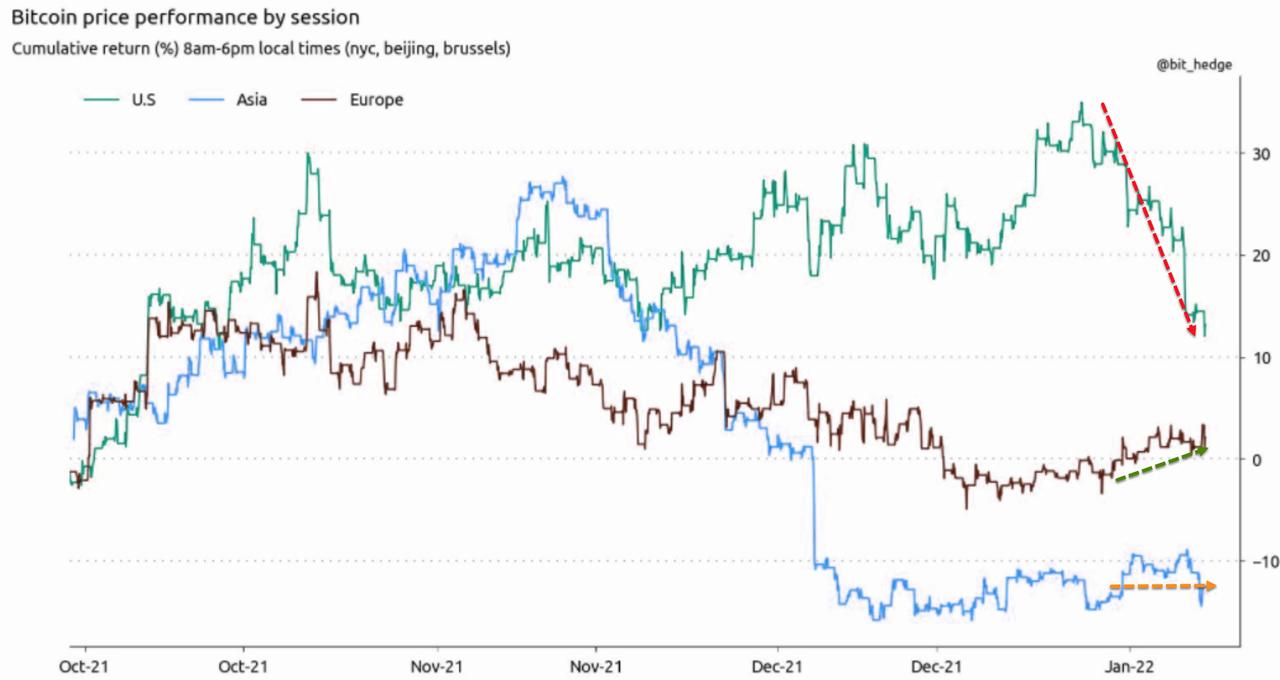

Cryptos were ugly this week to start 2022, with Ethereum the worst performer…

Source: Bloomberg

With Bitcoin breaking down to a $40,000 handle today, its lowest since late September 2021…’

Source: Bloomberg

Notably The US session is dominating the selling pressure on cryptos, perhaps suggesting this is more related to mega-cap tech liquidation

Commodity markets were very mixed with crude surging while precious metals and copper were sold…

Source: Bloomberg

WTI rallied up to $80 this week, erasing all concerns over Omicron impacting demand and any short-term gain from Biden’s cunning plan to cut gas prices…

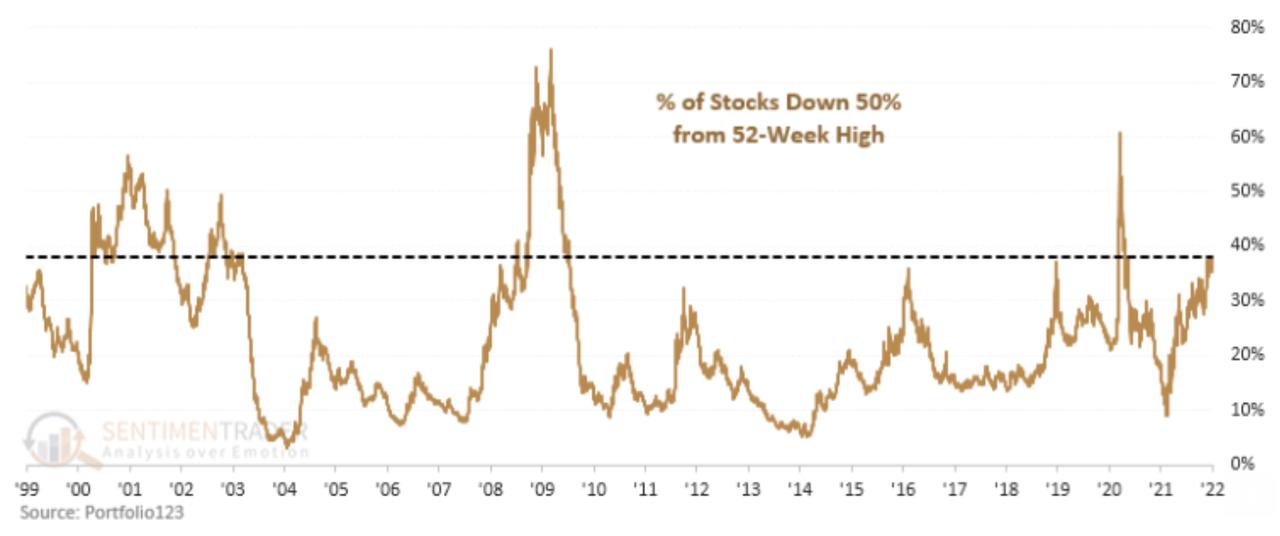

Finally, we note that Sentimentrader points out there is a massive meltdown in Nasdaq stocks:

“After Wednesday’s post-FOMC selloff, more than 38% of stocks trading on the Nasdaq are now down 50% from their 52-week highs. Only 13% of days since 1999 have seen more stocks cut in half.”

And in case you believe in BTFD, you probably should consider this: “When at least 35% of stocks are down by half, the Composite has been down by an average of 47% (!) from its 3-year high.”

And there is simply no way that a modest 2% drop in the S&P will trigger the Powell Put!

Tyler Durden

Fri, 01/07/2022 – 16:01

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com