Fiduciary Wall Of Shame: These “Woke” Managers Caved To ESG Pressure And Missed Oil’s Epic Run Higher

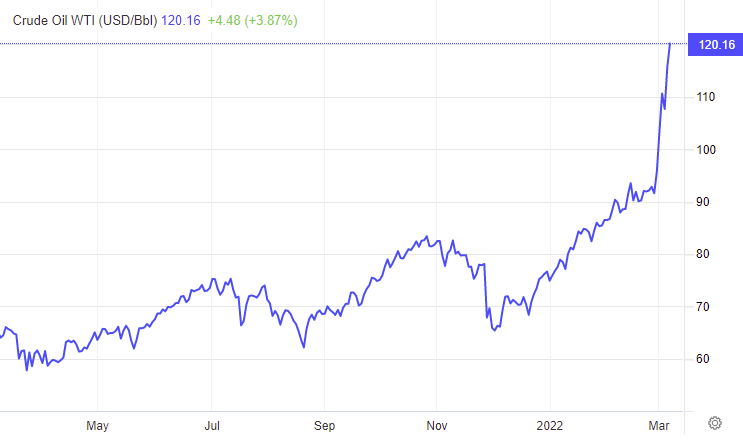

With oil now raging through $120 a barrel with little or no signs of stopping, we thought it would be a good time to look back over the “woke” virtue signaling ESG idiocy investment decisions that some actively managed funds made over the course of the last year.

Of course, leading off, you had managers like Cathie Wood, who claimed in 2020 that oil would be going to $12 per barrel, due to global demand peaking and the “world shifting to electric vehicles”. Wood amended this prediction brilliantly in 2021, when she said that she then saw a “$70 ceiling” on oil, continuing to push her narrative that EVs would “keep crude from breaking out”.

That, obviously, has not been the case.

Recall, we wrote about the “geniuses” at Harvard’s endowment, who said in September 2021 (when oil was about 40% lower), that they would stop investing in fossil fuels. The fund made the change after what Bloomberg called “years of sustained activism from students calling for fossil-fuel divestment”.

We’re sure the students have been baffled taking their ECON 101 courses this year, learning about discounting cash flows while the very school they are attending’s endowment has missed out on hefty dividends and fat streams of cash. Perhaps the students minds will change when the cafeteria is forced to forego their favorite organic, gluten-free grass fed lunches due to budget constraints.

Regardless, Harvard was following in the footsteps of schools like the University of California and the U.K.’s Cambridge University. The University said last year it would also work to forge a path to “net zero” greenhouse gas emissions by 2050.

That, of course, wasn’t fast enough for a “students group”, Bloomberg wrote last year, who had nothing to do with their time so they took to filing a complaint in March with the Massachusetts attorney general “in an attempt to force the university to sell its estimated $838 million fossil fuel holdings”.

Oil has ripped about 40% higher since then. Great job, future brilliant minds of America!

Also remember that in December 2021, it was reported that cities like Irvine, Calif. were holding meetings to “explore ways of discontinuing the city’s oil and gas holdings, among other types of investments deemed incompatible with city values”. At the time, the city had $5 million in Exxon Mobil.

The city’s values obviously don’t include making money.

The same report said that “an increasing number of agencies have sent requests” to CalPERS to try and ask them to divest of their fossil fuel companies.

The City of Encinitas also voted last September to “urge CalPERS to take such divestment action and update the city’s own investment policy which doesn’t have any direct fossil fuel holdings.”

Now that CalPERS is lightening up their oil and gas exposure, they can focus more on dumping their exposure to Russia, right before those stocks once again rip higher. “CalPERS and CalSTRS, the nation’s two largest public pension funds, and the UC system, have a combined $1.5 billion in Russian investments,” the LA Times reported.

Finally, in early February, when oil was still easily in the double digits, the $280 billion NY State Pension fund dumped 21 shale companies because they “hadn’t committed to low emissions”.

New York Comptroller Thomas DiNapoli commented at the time: “To protect the state pension fund, we are restricting investments in companies that we believe are unprepared to adapt to a low-carbon future.”

“In other words, to protect the fund, we must destroy its returns,” we retorted, noting that at the time, executives were calling the economics of the industry “the best in years”.

“The reason that ‘guru’ is such a popular word is because ‘charlatan’ is so hard to spell.” – William Bernstein. Exhibit 27,844 … pic.twitter.com/12qIvIoCPh

— Spencer Jakab (@Spencerjakab) March 7, 2022

Tyler Durden

Tue, 03/08/2022 – 11:05

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com