“Traditional” Vs “Disruptive” Portfolio Construction & Why It Matters So Much!

Authored by Peter Tchir via Academy Securities,

Most of the time, Wall Street tends to focus on big institutional flows. For years that was probably okay, but that led to horrible decisions during the pandemic. Retail flows were a crucial driver of markets, and we are at an inflection point where retail will be a big determinant of what happens next!

This expands on the “non virtuous” cycle work we first presented in Bad to the Bone. It will also clarify some thoughts on crypto as a leading indicator of stocks that we touched on in Friday morning’s email.

Sorry, Not Sorry

This portfolio construction analysis:

-

Will be overly simplified.

-

Will annoy you at times.

-

Will make you smile at times (hopefully).

-

Will, after further consideration, help you understand some market dynamics that are at play and could trigger the next big move (and why I’m concerned that is to the downside).

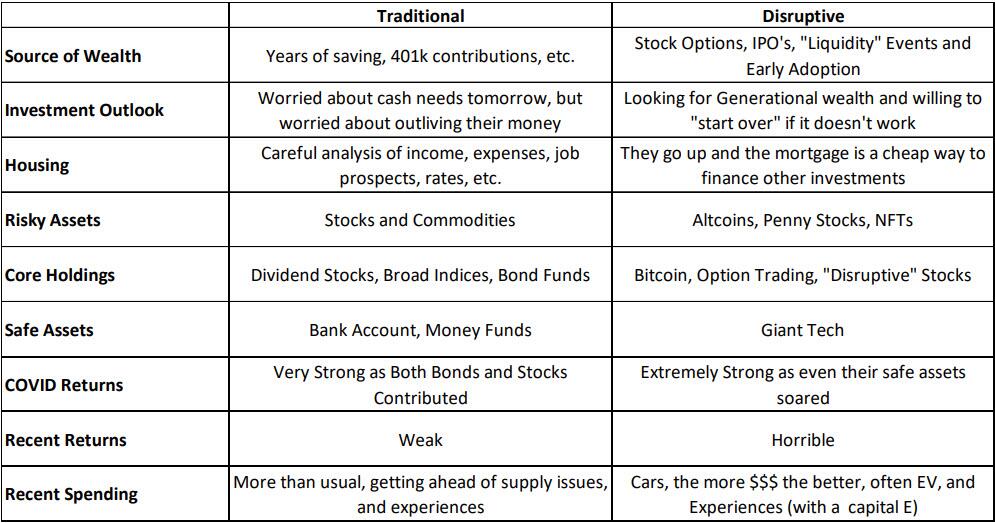

“Traditional” vs “Disruptive” Portfolio Construction

Let’s use “traditional” to mean the sort of investor that existed well before COVID. Maybe an investor that would have been the “norm” for individual investors, circa 2017. Let’s then imagine a class of investor that is “disruptive” by nature and was doing well pre-COVID, but flourished during COVID.

I did warn you that it would be simplistic and some parts would likely anger you, but let’s just run with this as the two main ways that retail is constructing portfolios and once you think about it, probably does cover the vast majority of retail investors.

The Traditional Investors’ “Conundrum”

TINA forced even conservative investors into more risk than they would traditionally take. The fear of not having enough money for their potential lifespan forced them into equities. Equities were no longer the pariah of conservative investors and they remained significant components well into retirement.

That worked great, but there really was no alternative.

I expect this group is already “de-risking.” They can decrease risk for similar expected returns.

The S&P 500 expected dividend yield is up to about 1.6%, though the recent increase from 1.4% in March and 1.3% at the end of December is by stocks dropping in price (the S&P 500 is down 15.6%) rather than by dividend growth. At the same time, the 10-year Treasury yield has risen from 1.5% to almost 3%. You can plow money into corporate credit to pick up additional current income and even the money market funds are back to paying some interest.

Fear of rising rates has caused big bond fund ETF outflows. The Muni market, mostly reflective of retail, has been a seemingly never-ending series of BWIC after BWIC (bid wanted in competition).

But, if you felt you needed to own dividend stocks to get income and those stocks are down hard and their yields now pale in comparison to Treasuries, do you start de-risking?

The “will I have enough” comes down to total return and carry. For whatever reason, and I’m not sure of the reason, the “will I have enough” investors seem to focus on yield more than anything and seem far more willing to take bond losses on a mark to market basis than they do on stocks. Ok, I cannot fully blame them, but there is this strange detachment from total return vs income, at least when I get more involved in that space.

I would not be surprised if these investors, while generally de-risking, weren’t adding some “hot sauce” to their portfolios. Taking some flyers on disruptive stocks and other assets that they “missed” during the crisis, but can now buy at “bargain” prices (or at least much cheaper than their peak prices).

While it will be gradual, I think this “de-risking” is occurring and will continue to occur as “traditional” investors go back to their roots and take on more “traditional” portfolios containing fewer equities and more bonds.

The Disruptive Investors’ Problem #1 – Crypto

While traditional investors face a conundrum, the disruptive investors face a real problem.

Bitcoin is at its lowest levels since December 2020. Anyone who added bitcoin during that timeframe is now underwater.

Making the situation more perilous (and why I’m currently so bearish crypto) is that:

-

Adoption and interest are waning.

-

When the average person sees something go up 10% a week and their media streams are filled with people calling for ever-increasing price targets, an asset class gets a lot of attention. When something stumbles and continues to stumble, even after a very successful run, the “told you so” crowd gets a lot more airtime. In December we wrote that TINA, BOGO, and FOMO’s Engines Are Stuttering. That thesis continues to play out and is worth a read.

-

We had a strong “use case”– Russia invading Ukraine. Currency restrictions. Sanctions. But, after a brief post invasion pop, crypto has renewed its descent. That likely discourages new investors.

-

-

When “stable” coins become “unstable.” This is the extent of my current knowledge, but here is my best take. Stable coins act as an “intermediate” step where people transacting in the crypto universe can remain in the crypto space without taking the market volatility of the cryptocurrencies. Terra (Luna), usually referred to as UST, was a $20 billion market cap algo based stable coin. I will be honest, I’m not sure what an algo based stable coin is, and I’m not about to find out, because it apparently went “poof.” Tether, known as USDT (notice how Q Macro Strategy Peter Tchir “Traditional” vs “Disruptive” Portfolio Construction & Why It Matters So Much! May 15, 2022 3 everything about crypto is meant to sound or look like a currency – great marketing), is worth $80 billion and is “supposedly” backed by some sort of assets. That at least I understand. I can relate to something being backed by something. There have been repeated questions about what is actually backing it, but those have been met by repeated assertions that it is in fact backed by assets. Tether (which was trading below $1) has rebounded since Thursday. I don’t know, but if you’ve gotten to this point and haven’t invested in crypto but are thinking about starting now, I’d love an explanation (btw, “stable coins” is another brilliant marketing moniker – there really is a trend here). I’m digging deeper into this whole area, but I don’t see how it is anything but a red flag.

-

China is trying to crack down on crypto use. One way is enforcement and the other way (no idea how they’d do it but always in the back of my mind) is the fact that you don’t have to worry about money outside of the system if you figure out a way to drive it to zero. I’m told its impossible, but I’ll leave it as low probability rather than impossible.

-

The U.S. and Western Europe will impose regulations. Mostly for tax purposes, but increasingly to ensure that less can occur outside the system.

-

I strongly believe that the NSA helped track some well publicized ransomware payments and helped get that returned. One, it tells me what a big, powerful entity can do if they focus on the space (assuming my “guess” is correct) which makes me think back to the China point. Two, ransomware as a “use” case may be dropping.

I’m extremely bearish crypto here. I understand that the “maxis” (bitcoin maximalists, who loath crypto other than bitcoin) point to many of the problems listed above as a reason to view bitcoin as a “flight to safety” play in crypto, but I don’t buy into it.

This is not the time, nor the place, but all you have to do is scroll through Twitter and you will find people with 100s of thousands of followers who say things just blatantly and factually incorrect. I’m not arguing about those who say it is going to $1 million, or those who tout that it is an inflation hedge, or those who say it is going to zero (and pound their chests on every drop, despite being wrong for the past few years), just people who state things as “facts” that are not in fact, facts. How many people are being “influenced” by the influencers? I think a high number and that scares me for the longer-term viability of the product (given everything else mentioned), but more importantly, leads me to believe the price drop could be larger than many expect.

I didn’t even delve into the “alt” coins or NFTs, which are bigger disasters waiting to happen (if it hasn’t already happened). That was the “play” money part of their portfolio and that for many is gone (along with interest in penny stocks).

The Disruptive Investors’ Problem #2 – Disruptive Stocks

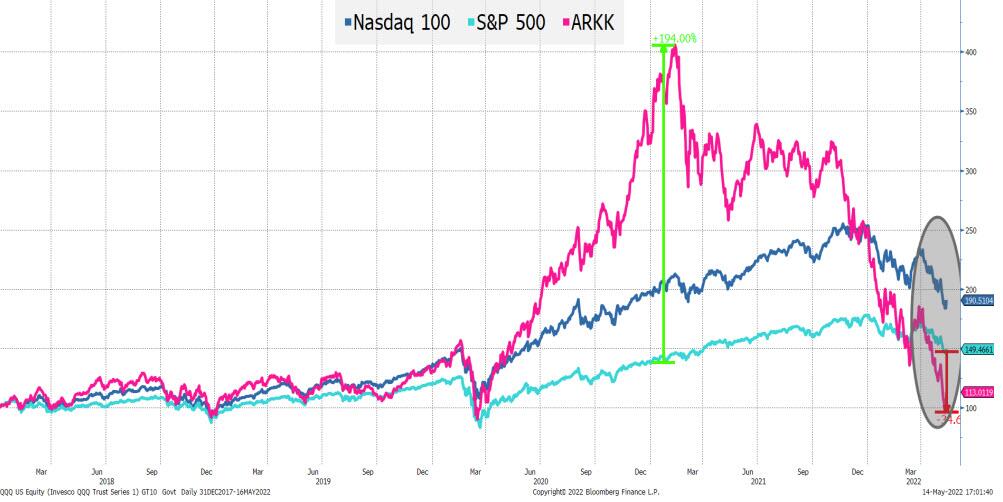

I’m not even going to include the cannabis related stocks because it makes the chart too complex, is piling on, and isn’t 100% related to my thesis, but probably could be.

ARKK, at one point in early 2021, had outperformed the S&P 500 (SPY) by 194%! And the S&P’s gains were not shabby! It had even blown away the returns of the Nasdaq 100 (QQQ). Now, in a “stunning” reversal, its returns since the start of 2018 are now lower than either of those!

As mentioned before, I do think more people are betting on a rebound (ARKK and TQQQ – 3x leveraged QQQ – have been getting extreme inflows), but some part of the disruptive investor must be nervous that they aren’t diversified at all?

The Disruptive Investors’ Problem #3 – Cash Equivalents?

Maybe I am wrong in what these investors considered “safe” assets. Ways to park their money. Maybe, they didn’t view giant tech as a cash holding/easy to access and was certain to go higher.

I may be wrong on that, but we have seen some of those companies turn over recently.

What if I’m right? What if the “disruptive investor” suddenly realizes that their portfolio should look a lot more like the traditional investor’s portfolio?

I think it might be difficult to distinguish between capitulation and a rebalancing from “disruptive” to “traditional,” but I’d argue that we have been seeing signs of that and it is unlikely to be over.

The End of “Gambling” Nation?

David Portnoy, the president of Barstool Sports (@stoolpresidente on Twitter) has gone from calling markets and competing with Cramer for social media’s most vocal stock “analyst” to mostly focusing on one-bite pizza reviews and sports, which he does extremely well!

DKNG down from $70 to $12, PENN down from $135 to $31, HOOD down from $70 to $11, and COIN down from $350 to $68 (though it almost broke $40 on Friday) all benefitted from this “gambling” mentality we saw during COVID. Maybe HOOD and COIN were experiencing “investing,” but I don’t think it is a leap of faith to consider at least some of it “gambling” or at least having the mentality of a “gambler” rather than an investor (you cannot convince me otherwise on weekly options on single stocks).

These are all tied together and all represent a dramatic shift in “disruptive” behavior.

TQQQ

I am going to come back to TQQQ for a moment.

It closed on Friday with a market cap of about $13 billion with 414 million shares outstanding. On April first, it had 321 million shares outstanding, so people have added about 100 million shares to this ETF in the last 6 weeks. TQQQ has dropped from $58 to $32 during that time. People are adding almost every day. There is very little capitulation (actually no capitulation). SQQQ – the 3x inverse – has fewer shares now than it did in January despite rallying from $29 to $52 over that time period. The aforementioned ARKK has by far the most shares outstanding in its history (though a much smaller total market cap).

But I digress, so back to TQQQ.

TQQQ had a market cap of $13 billion on Friday. QQQ closed at $302 (TQQQ doesn’t actually buy QQQ, but let’s pretend it does, since that simplifies the math).

On Monday, TQQQ has to be set up to deliver 3x the daily percentage change in the Nasdaq 100 (QQQ is our proxy).

So, let’s assume that TQQQ borrows $26 billion to buy $39 billion of QQQ (129 million shares).

That means that whatever happens on Monday, TQQQ will have made or lost 3x the daily percentage change.

For example, if QQQ went up 3% on Monday, it would close at $311.06 (using $302 as starting price).

The shares held by TQQQ would be worth $40.17 billion, which after they repaid the loan would be worth $14.17 billion (or 9% higher than the $13 billion TQQQ started the day at).

But this is where it gets interesting!

As we went into Monday’s close, QQQ would need to be prepared to match 3 times the daily percentage change.

Even at the elevated price of QQQ, TQQQ would need to hold 136.6 million shares going into Tuesday (instead of the 129 million shares it already had).

So, TQQQ would have a buy order in at the close on 7.5 million shares of QQQ or $2.3 billion!

The daily rebalancing of a 3x leveraged fund creates additional buys on up days and additional sells on down days! It tends to make moves even bigger than they would be otherwise.

Think about that, a fund that is “only” $13 billion needing to buy as much as $2.3 billion if we get a 3% move (which seems the norm) and there were no inflows! This is the exact sort of mechanism that caused the inverse VIX ETFs to explode, though by their nature they actually had much higher leverage because of the way the underlying share count was calculated, but that should be a sobering reminder.

The reverse also happens and TQQQ will have to sell into the close on down days, but so far, that has been largely offset by fund inflows!

What if the fund inflows stop?

My Fear

My biggest fear is a shift from “disruptive” portfolios to “traditional” portfolios.

-

The riskiest portion has been hard for many (NFT, Alt Coins, etc.)

-

The “core” investment, other disruptive stocks, bitcoin, etc., has been hit hard.

-

The companies they are working for may have gone from upping pay to suddenly being focused on costs, making salary less certain going forward.

-

The thing that they viewed as the “piggy” bank is suddenly under pressure as well.

These things occurring force a large unwind. Unfortunately, some of the “safe” stocks have come to represent huge portions of the indices, which would quickly spread losses.

Could we have TQQQ “go poof” like the VIX ETNs? No, the leverage isn’t there.

Could we have a limit down day as outflows combine with rebalancing and other selling to hit broad markets? I do not see why not.

Could this happen if crypto rebounds? I doubt it, in fact, I think crypto would need to be the catalyst for more of the moves we have seen, but if crypto goes down and stays down (given its poor liquidity), we see a very ugly day in risk assets.

Bottom Line

I think we could see the Fed soften its stance now that Powell is being confirmed. That would help risk assets, but I’m far more concerned that Thursday’s crypto led selling pressure was only a taste of what is to come. I don’t know the timing, but puts for the next month seem worth it.

I will also be watching to see if there is any “profit” taking on the recent bounces in the crypto and disruptive stocks.

On Treasuries, we will get TIC data on Monday that shows what China, the Saudis, and other countries did with their Treasury holdings in March (I suspect that they reduced their exposure and that will explain some of the relative performance of Treasuries versus the debt of other countries).

I don’t see liquidity improving in the coming weeks as we are at best halfway through people rethinking about risk and reward and adjusting their portfolios accordingly (hedge funds, large asset managers, traditional, and disruptive investors included).

Maybe this was all just a crazy way to think about markets, how they are intertwined, and what is happening, but it explains a lot and highlights some serious and plausible risks!

As much as I think tone at the Fed will change, I’m more nervous than bullish (again) – ugh!

Tyler Durden

Sun, 05/15/2022 – 12:15

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com