Futures Grind Higher With All Eyes On Red-Hot CPI

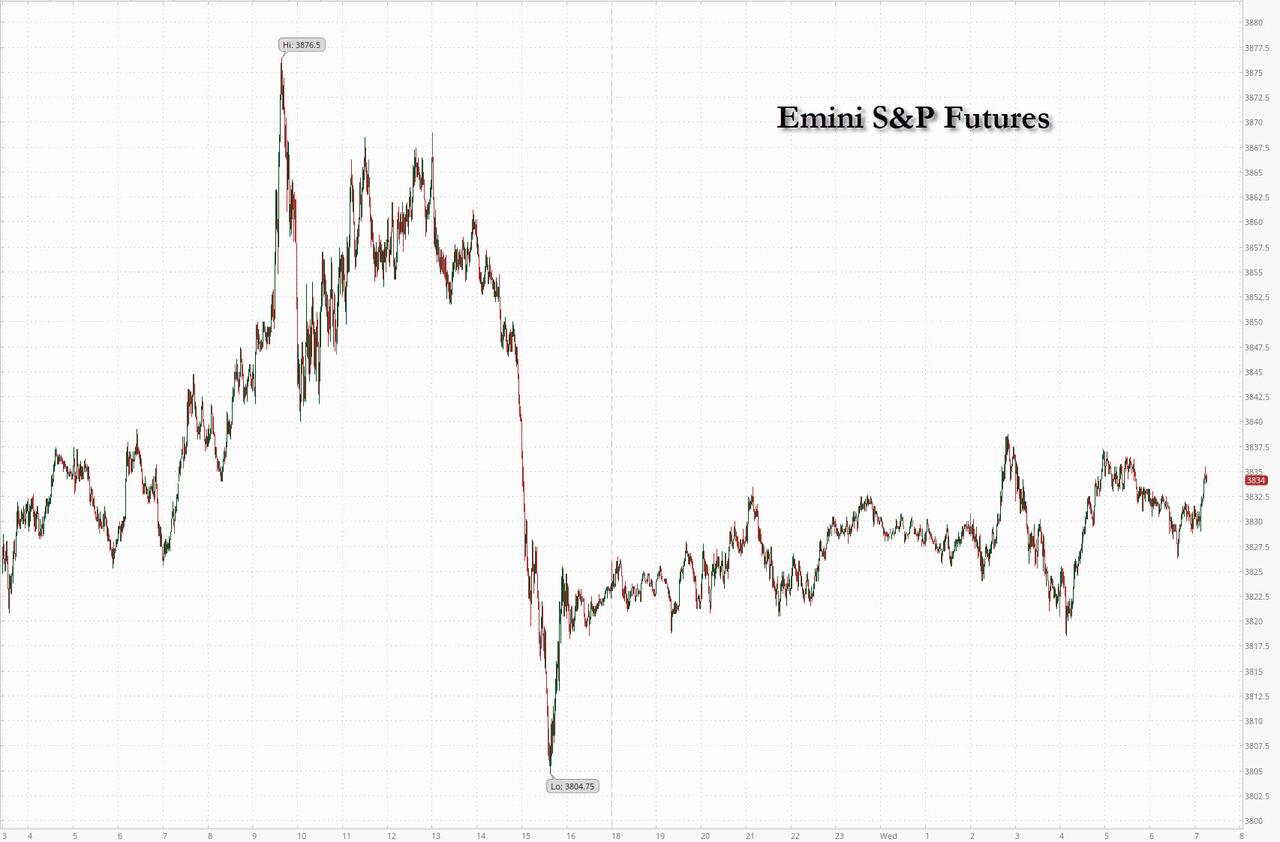

After yesterday’s last hour stock market puke prompted by a fake CPI “leak” that showed inflation rising more than double digits in June which sent spoos just over 3,800, US index futures advanced ahead of a report that will show inflation hitting a fresh four-decade high according to Bloomberg consensus which expects headline inflation to print 8.8%, ensuring another 75bps rate hike. Contracts on the S&P 500 rose 0.3% by 7:15 a.m. ET after the underlying gauge declined over the past three days. Nasdaq 100 futures were up 0.4% after the tech-heavy index shed 3% this week, reversing most of last week’s gains. The dollar dropped from a 2 year high, bitcoin rose but held below $20,000 and WTI crude oil stabilized at about $96 a barrel after a tumble.

Among notable pre-market movers, Twitter rose 1% after suing Elon Musk over his abandoned $44 billion takeover bid, accusing the billionaire of having buyer’s remorse after his fortune declined. Meanwhile, Atara Biotherapeutics tumbled 36% after the biotech firm gave an update on its multiple sclerosis therapy with Cowen strategists saying that the interim analysis of the ATA188 Phase 2 study was “inconclusive.” Here are other notable premarket movers:

- Stitch Fix (SFIX US) jumps 9.3% in premarket trading after J William Gurley, a board member and general partner at venture capital firm Benchmark, bought $5.43 million of shares in the company. Gurley’s purchase comes as the online personal-styling platform’s stock has fallen 73% this year.

- Atara Biotherapeutics (ATRA US) shares drop 41% in US premarket trading, after the biotech company gave an update on its multiple sclerosis therapy, with Cowen saying that the interim analysis of the Phase 2 study was “inconclusive” and Roth flagging potential “additional risks.”

- Humanigen (HGEN US) shares plummet as much as 76% in US premarket trading, after the biotech firm said that its Covid-19 drug trial didn’t achieve statistical significance on the primary endpoint, with Cantor Fitzgerald cutting its rating on Humanigen to neutral from overweight.

- Keep an eye on Apple (AAPL US) shares as Citi lowers its estimates for the company given cooling consumer spending trends amid macro woes and continued supply chain bottlenecks.

- Hannon Armstrong (HASI US) stocks could be active as analysts defended the climate-change investment firm after its shares slumped 19% on Tuesday. The losses followed a report from short seller Carson Block’s Muddy Waters Capital that criticized its accounting practices.

- Watch Alphabet (GOOGL US) stocks as Cowen trims 2022 Google Search and YouTube ad estimates, following checks that suggested that Search is seeing healthy demand but the business is decelerating, largely in line with expectations.

US inflation is projected to have continued to heat up in June, hitting a fresh pandemic peak. The consumer price index probably increased 8.8% from a year earlier, marking the largest jump since 1981, as discussed some banks expected a slightly softer print although others sees headline CPI rising as much as 9.0%. The consumer-price reading will be a major decisive factor for the Fed in its upcoming meeting as it decides how much further it should tighten policy to tame soaring inflation. Its hawkish policy already stoked fears the economy is heading for a recession this year.

“This is widely expected to be a really strong print,” Lauren Goodwin, economist and portfolio strategist at New York Life Investments, said on Bloomberg Television. “Even if it is not, I don’t think that changes the Fed’s perspective in a couple of weeks. We won’t have enough evidence that inflation is convincingly turning over.”

Meanwhile, the International Monetary Fund cut its growth projections for the US economy and warned that a broad-based surge in inflation poses “systemic risks” to both the country and the global economy.

Traders are also on tenterhooks for the latest corporate earnings getting underway this week and monitoring for a brewing energy crisis in Europe if Russia cuts off gas supplies in the fallout from its invasion of Ukraine. After today’s CPI, investor focus will turn to the start of the earnings season, which kicks off tomorrow with major Wall Street banks.

Meanwhile in Europe, the region’s benchmark Stoxx 600 Index fell 0.5% while the Euro Stoxx 50 slumped as much as 1.2% before roughly halving losses, amid deteriorating economic outlook. Shares of insurance companies and automakers led the drop.. FTSE 100 and FTSE MIB lag on the recovery. Autos, insurance and travel are the worst-performing sectors. Here are the biggest movers:

- Saipem shares tumble as much as 45%, extending Tuesday’s 49% slump, after only 70% of its EU2 billion rights offering was taken up by investors, signaling low confidence in the engineering company’s turnaround plan.

- Svenska Cellulosa falls as much as 4.1% and DS Smith declines 2.7% as Exane BNP downgrades its ratings on both, saying it anticipates a robust 2Q for packaging, but a correction in pulp prices.

- Bayer drops as much as 3% after a US appeals court reinstated a lawsuit by a Roundup herbicide user who claims the company failed to warn him of cancer risks.

- Galp Energia falls as much as 2.8% following its second-quarter production update, with analysts saying volumes were softer than anticipated.

- Vontobel declines as much as 6%, and EFG falls as much as 5.2% after Citi cut both to sell and kept a buy rating on Julius Baer, saying that it still sees good value in Swiss banks and prefers larger players to independents.

- Evonik falls as much as 3.9% after Barclays cut its rating to equal-weight, saying that it sees opportunities in Brenntag and Lanxess among European chemicals stocks.

- Orion gains as much as 7.9% after the pharmaceutical company raised its FY outlook after announcing it plans to work with MSD on developing and commercializing ODM-208, a drug for prostate cancer.

- Outokumpu gains as much as 6.5% after the stainless steel producer sold the majority of its Long Products business, a transaction which Jefferies and Morgan Stanley describe as positive.

- Hugo Boss rises as much as 3.1% as Jefferies says the company appears to be outperforming its luxury peers, and that expectations of continued growth, “comfortable” guidance and a successful rebrand are starting to move the market.

- Verallia gains as much as 3.3% after being initiated with a buy rating at Jefferies, which says the glass-packaging maker’s discount to peers is “unjustified.”

Earlier in the session, Asian stocks advanced, led by the region’s technology shares. The MSCI Asia Pacific Index gained as much as 0.6%, halting a two-day slide that dragged the benchmark to the lowest level in two years on Tuesday. Tech names such as TSMC, JD.com and Meituan contributed the most to the rally. Information technology was the region’s best-performing sector as the Hang Seng Tech Index bounced back after its recent drops sent the measure into a technical correction. Taiwan’s benchmark jumped nearly 3% as the government vowed to support the stock market for the first time since the early days of the pandemic. Equities posted moderate gains in South Korea and New Zealand after their central banks hiked interest rates by 50 basis points as expected. Thailand’s stock market was closed for a holiday. “Central bankers, policy makers all over the world are gonna have to pick their spots on how much inflation they’re prepared to tolerate versus how much a growth downdraft they wanna create,” Ben Powell, chief APAC investment strategist at BlackRock Investment Institute, said in a Bloomberg TV interview. In addition to today’s data on consumer prices to assess what the Federal Reserve will do next, traders are also monitoring corporate earnings results in Asia for signs of any impact from China’s lockdowns during the second quarter.

Japanese stocks advanced as investors await US data that may show inflation hit a fresh four-decade high. The Topix index rose 0.3% to 1,888.85 at the 3pm close in Tokyo, while the Nikkei 225 advanced 0.5% to 26,478.77. Recruit Holdings Co. contributed the most to the Topix’s gain, increasing 2.9%. Out of 2,170 shares in the index, 1,400 rose and 633 fell, while 137 were unchanged. “Japanese stocks will have a hard time finding a sense of direction before the US CPI announcement,” said Mitsushige Akino a senior executive officer at Ichiyoshi Asset Management.

In FX, the Bloomberg Dollar Spot Index held near its highest level in more than two years and the greenback traded mixed against its Group-of-10 peers as traders awaited US inflation data later on Wednesday for clues on the Federal Reserve’s rate trajectory. JPY and SEK are the weakest performers in G-10 FX, CHF and AUD outperform. EUR/USD stalls again, declining 6 pips shy of parity before recovering slightly. Money markets raised bets on the pace of BOE rate hikes after the UK economy grew faster than the median estimate in May to ease fears of a recession. UK GDP rose by a surprisingly robust 0.5% amid a surge in visits to doctors and holiday bookings, after an 0.2% decline in April, a figure that was revised higher. New Zealand’s dollar initially fell and then erased losses after the central bank raised interest rates by 50 basis points as economists forecast. The yen underperformed all its Group-of-10 peers amid expectations US CPI will be strong enough to keep wagers high for a continued aggressive rate-hike cycle by the Federal Reserve. Super-long sectors led drop in government bond yields after purchases by the Bank of Japan.

In rates, the 10-year Treasury yield was little changed at 2.97% after falling two basis points on Tuesday. Cash TSYs are comparatively quiet ahead of today’s CPI release. German and UK curves bear-flatten, underperforming Treasuries. Peripheral spreads widen to Germany with 10y BTP/Bund back near 200bps. Gilts and Bunds fell, underperforming Treasuries. Money markets raised bets on the pace of BOE rate hikes after the UK economy grew faster than the median estimate in May to ease fears of a recession.

In commodities, crude futures advance. WTI drifts 1.1% higher to trade near $96.90. Most base metals trade in the green; LME lead rises 1.1%, outperforming peers. LME zinc lags, dropping 0.2%. Spot gold is little changed at $1,726/oz

To the day ahead now, and data releases include the US CPI release for June, as well as UK monthly GDP for May and Euro Area industrial production for May. Otherwise from central banks, the Bank of Canada will be making their latest policy decision, and the Federal Reserve will release their Beige Book.

Market Snapshot

- S&P 500 futures up 0.2% to 3,830.50

- STOXX Europe 600 down 0.8% to 413.52

- MXAP up 0.3% to 155.40

- MXAPJ up 0.5% to 511.37

- Nikkei up 0.5% to 26,478.77

- Topix up 0.3% to 1,888.85

- Hang Seng Index down 0.2% to 20,797.95

- Shanghai Composite little changed at 3,284.29

- Sensex down 0.5% to 53,636.37

- Australia S&P/ASX 200 up 0.2% to 6,621.56

- Kospi up 0.5% to 2,328.61

- German 10Y yield little changed at 1.16%

- Euro little changed at $1.0038

- Brent Futures up 1.1% to $100.63/bbl

- Gold spot up 0.0% to $1,726.85

- U.S. Dollar Index little changed at 108.15

Top Overnight News from Bloomberg

- The planned reopening of a key Russian gas pipeline next week may be a bigger deal for the euro than the first interest-rate hike in a decade by the ECB. Both are set for July 21. While the ECB’s plans to start lifting rates have been well flagged and hence priced in by markets, there’s more doubt over whether Russia will actually restore gas flows to Europe after maintenance on the Nord Stream 1 pipeline is completed

- China will take advantage of the market-based adjustment mechanism of deposit rates and guide financial institutions to transmit the effect of falling deposit rates to their borrowers as part of efforts to lower real lending rates, Zou Lan, head of PBOC’s monetary policy department, says at a briefing

- The ECB is watching the euro-dollar exchange rate as recent lows can further stoke already record inflation, according to Governing Council member Francois Villeroy De Galhau

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were mostly positive as the region shrugged off the weak lead from Wall St but with upside capped amid central bank rate hikes and ahead of upcoming key risk events including Chinese trade and US CPI data. ASX 200 traded indecisively as strength in tech was offset by losses in energy after the recent slump in oil prices. Nikkei 225 was underpinned by a weaker currency but with gains limited after a ramp-up in Tokyo COVID cases. Hang Seng and Shanghai Comp. gained but with the mainland choppy ahead of Chinese trade data, while Hong Kong tech stocks were bolstered after China approved 67 domestic games in July.

Top Asian News

- China’s Customs said foreign trade is expected to achieve stable growth and that trade growth in May and June reversed the declining trend, but noted that foreign trade faces instabilities and uncertain factors, according to Reuters.

- “Lanzhou in NW China’s Gansu Province has sealed off its 4 districts for 7 days to curb the latest COVID19 flare-up which started from last Friday and has led to 143 infections as of 10 am on Wed”, according to Global Times.

European bourses are pressured and towards the mid-point of the morning’s parameters as we await US inflation data, Euro Stoxx 50 -0.6%. Sectors, are predominently in the red with defensively-inclined names lagging though Energy outperforms and is green amid benchmark action. Stateside, futures are modestly firmer but have been choppy with pre-CPI positioning underway; ES +0.2%. Alphabet (GOOGL) said, on July 12th, that due to the hiring progress already attained, will slow the hiring process for remainder of year, via Reuters; like all Cos, not immune to economic headwinds. Kroger (KR) is launching an annual membership, provides unlimited free deliveries on orders over USD 35 and fuel discounts of up-to USD 1/gallon alongside other savings.

Top European News

- UK lawmakers are to push ahead with legislation to tear up the post-Brexit trade deal today, according to FT.

- Network Rail offered workers at two unions pay hikes in a bid to avert further crippling strikes, according to FT.

- Italy’s Salvini says the League Party is not willing to remain in the government if the 5-Star Party quits, adding that if 5-Star does not back a Thursday confidence vote, Italy should call snap elections. Subsequently, Democratic Party is unwilling to form new governments without the 5-Star Party, according to a party source cited by Reuters.

Geopolitical

- China’s military said it monitored and drove away a US destroyer which entered the South China Sea Paracel Islands, while it added that the actions of the US military seriously violated China’s sovereignty and security. Furthermore, the US military stated that USS Benfold asserted navigational rights and freedoms near the Paracel Islands consistent with international law, according to Reuters.

- US Navy says the Ronald Reagan Carrier Strike Group is operating in the South China Sea.

- Venezuela detained at least three Americans earlier this year accused of attempting to enter the country illegally, according to sources cited by Reuters.

- Iran Foreign Ministry spokesperson says results of the negotiations with Saudi Arabia have been promising, sides have an interest to continue talks. Subsequently, Iran President Raisi says it will not retreat from its ‘rightful’ stance in talks to revive the 2015 JCPOA, state TV reported.

Central Banks

- RBNZ hiked the OCR by 50bps to 2.50%, as expected, and said it remains appropriate to continue to tighten policy, while it will tighten conditions at a pace to maintain price stability and support maximum sustainable employment. RBNZ added the Committee is resolute in its commitment to ensuring price inflation returns to the 1%-3% target range and it agreed to lift the OCR to a level where it is confident consumer price inflation will settle within the target range but added that once aggregate supply and demand are more balanced, the OCR can return to a lower and more neutral level. Furthermore, the Committee agreed to maintain the approach of briskly lifting the OCR and remained comfortable with the projected path of the OCR it outlined in May, as well as noted that there are near-term upside risks to consumer prices and also medium-term downside risks to economic activity.

- BoK raised its Base Rate by 50bps to 2.25%, as expected, with the decision made unanimously. BoK stated that South Korea’s 2022 growth will moderate further from an earlier projection and inflation will remain high for some time, as well as noted that inflation will surpass the May forecast for the entire of 2022 and that core inflation is to be higher than 4% for a considerable period. Furthermore, BoK Governor Rhee said more policy tightening of 25bps looks appropriate going forward should current inflation continue for the time being and that it is reasonable to expect rates at 2.75%-3.00% by year-end.

- ECB’s Villeroy says it is not the EUR that is weak but the USD that is strong.

FX

- Greenback grinds higher ahead of US inflation data, but remains restrained, DXY back above 108.000 within 108.020-390 range.

- Aussie regroups alongside base metals and awaits labour report for further impetus; AUD/USD approaching 0.6800 vs sub-0.6750 low.

- Franc forges safe-haven gains vs Dollar and Euro, USD/CHF below 0.9800 and EUR/CHF under 0.9850.

- Kiwi somewhat deflated after RBNZ maintained half-point tightening pace, guidance and OCR path, NZD/USD capped into 0.6150.

- Sterling underpinned by above-forecast UK data and remarks from BoE Governor Bailey leaning towards bigger than 25bp hike, Cable straddling 1.1900 and EUR/GBP pivoting 100 and 200 DMAs.

- Loonie looking for a BoC boost via 75bp rate increase and hawkish guidance, USD/CAD towards the low end of 1.3050-00 band with 1.57bln option expiries rolling off at the round number.

- Yen undermined by firmer US Treasury yields pre-CPI and post-weak 10-year note the auction, USD/JPY rebounds through 137.00 again.

- Yuan pares some losses after China’s trade surplus tops consensus and PBoC pledges to up support for real economy; USD/CNH and USD/CNY testing bids and support on either side of 6.7200.

Fixed Income

- Debt fades from early EU highs irrespective of risk-off sentiment as clock ticks down to key US CPI data.

- Bunds pull up just ahead of 153.00, Gilts into 116.00 and T-note shy of 119-00.

- Italian and German supply relatively well received, but impending long bond refunding comes hot on the heels of tepid demand for 10 year issuance.

Commodities

- Crude benchmarks are bid after a concerted pick-up in the European morning that occurred without any obvious fresh fundamental driver.

- US Private Inventory Data (bbls): Crude +4.7mln (exp. -0.2mln), Gasoline +2.9mln (exp. -0.4mln), Distillates +3.2mln (exp. +1.6mln), Cushing +0.3mln.

- Libya’s Government of National Unity decided to replace the NOC chairman and board, according to a government source. NOC later announced the lifting of the force majeure on exports from the Brega and Zueitina oil terminals, while it added that negotiations were conducted to allow exports from Es Sider port and resume output at the Al Waha and Mellita fields, according to Reuters.

- Eni (ENI IM) Chair says Italy will be able to replace 50% of Russian gas flows with other sources this winter, and 80% next winter, via Reuters citing a paper.

- Hungary Foreign Minister says it could purchase up to 700 MCM of gas on the market ahead of the heating season, in addition to long-term supply deal with Russia.

- IEA OMR: 2023 demand 101.3mln BPD, +2.1mln BPD; led by strong growth in non-OECD countries. 2022 demand cut by 200k BPD, seeing a rise of 1.7mln to 99.2mln BPD

- Spot gold is modestly firmer managing to capitalise on the session’s bout of USD easing, LME Copper has benefited from the generally constructive APAC tone though participants will remain cognisant of and cautious around the China-COVID situation.

US Event Calendar

- 07:00: July MBA Mortgage Applications -1.7%, prior -5.4%

- 08:30: June CPI YoY, est. 8.8%, prior 8.6%; MoM, est. 1.1%, prior 1.0%

- 08:30: June CPI Ex Food and Energy YoY, est. 5.7%, prior 6.0%; MoM, est. 0.5%, prior 0.6%

- 08:30: June Real Avg Hourly Earning YoY, prior -3.0%, revised -2.9%

- 08:30: June Real Avg Weekly Earnings YoY, prior -3.9%, revised -4.0%

- 14:00: U.S. Federal Reserve Releases Beige Book

- 14:00: June Monthly Budget Statement, est. -$75b, prior -$174.2b

DB’s Jim Reid concludes the overnight wrap

I’m supposed to be off for the next three days with the family but given how busy things are I’m delaying two of the days until August. However I can’t escape a Theme Park outing tomorrow so I’m still doing that. I hate Theme Parks and rollercoasters with a passion. Readers might remember the last time I went I had an argument with someone who pushed in with his whole family in the queue ahead of me. I was most disgruntled at the end of a long day and vowed never to return. However my kids love them. If it were up to me my preferences would dominate and we wouldn’t go but unfortunately my selfless wife puts our kids first. Probably a good thing!!

I’ll be here now for the all important US CPI today but I’ll miss the ceremonial start of earnings season tomorrow with this week seeing a small selection of major US financials and consumer packaged goods companies reporting. My colleague Binky has just released his full preview, available here. He expects earnings to beat in the low single digits percentage region, below the long-run historical average of 5%. Earnings are likely to be 3.1% qoq along with downward revisions to forward estimates. Heading into earnings season, estimates have been revised lower for every sector but energy, which has experienced upgrades. Using a bottom-up approach, yoy EPS growth will come in at 5.7%.

Heading into CPI and earnings, after markets had climbed a wall of worry since mid-June, they seem to be losing a bit of footing again over the last few days as fears of a recession dominate again, alongside fears of aggressive rate hikes by central banks, rising Covid cases in China and the prospect of Russia cutting off Europe’s gas. This gloomy backdrop saw the S&P 500 (-0.92%) lose ground for a 3rd day running, whilst those fears of weakening demand sent Brent crude oil prices back beneath $100/bbl and also led to day two of a new fresh sizeable rally in sovereign bonds. Oil is little changed in Asia trade with Brent and WTI futures almost flat at $99.76/bbl and $95.99/bbl respectively as we go to press.

However, today’s main focus will almost certainly be on the US CPI release for June, which will set the stage for the Fed’s next decision in just two weeks’ time. Remember that it was last month’s much stronger-than-expected report that sparked a tumultuous market reaction that culminated in the Fed moving by 75bps at a single meeting for the first time since 1994, having previously only signalled a 50bps move. So any further surprises today could have a big impact. In terms of what to expect, our US economists are looking for an above-consensus monthly reading for both headline CPI (+1.3%) and core CPI (+0.6%), which in turn would take the year-on-year headline CPI up to its highest level since 1981, at +9.0%.

Although we’re expecting another strong inflation print today, ahead of that release there were actually growing signs of respite on the inflation front thanks to further losses amongst a number of key commodities. Brent Crude (-7.11%) and WTI (-7.93%) oil prices saw substantial losses, copper prices (-4.10%) hit a 19-month low and gold (-0.46%) hit a 9-month low. Indeed, the only major exception to that pattern was the usual suspect of European natural gas (+4.92%) which just about reversed the previous day’s decline following cuts to Norwegian capacity. Our research colleagues in Frankfurt published a detailed note yesterday on the gas supply issue (link here), where they run through 3 scenarios of how things might evolve, including what happens if Russia completely turns off the gas taps to Germany after the maintenance period that would involve gas being rationed during the winter months.

Although many will welcome the decline in those commodities mentioned above, the bad news is that the reason they’re declining is because of recession fears, and yesterday saw a number of additional recessionary indicators flash with growing alarm. One in particular is the 2s10s curve, which has inverted before every one of the last 10 US recessions, and remains near its most inverted of this cycle so far at -8.5bps after dipping below -12bps intraday. We would stress that while we are the yield curve’s biggest fan, it usually takes a minimum of three quarters from inversion to recession so we still think it may take a bit of time from the first inversion in March to confirm the almost inevitable recession.

For the 1s10s and the 2s5s curve, it was much the same story of being the most inverted so far this cycle, and the 3m10s curve reached its flattest since November 2020. And whilst the Fed have told us to focus on their preferred near-term forward spread (18m3m minus 3m), even that closed beneath 100bps for the first time so far this year at 94bps (from a peak of 270bps in early April), so these measures are all trending in the wrong direction from a recessionary standpoint.

In terms of the absolute yield moves, the risk-off tone saw them move lower on both sides of the Atlantic. 10yr Treasury yields fell -2.4bps to 2.97% albeit having being as much as -9.6bps lower intraday. There was a discrete bounce in longer-dated Treasury yields following the 2bp tail in the 10yr auction. Yields are fairly stable in Asian trading. Meanwhile in Europe, those on 10yr bunds (-11.3bps), OATs (-12.8bps) and BTPs (-9.8bps) all fell back too, as concerns about the economic situation led investors to price in a less aggressive pace of monetary tightening over the coming months, particularly from the ECB. That also meant that the Euro itself moved ever closer to parity against the US Dollar yesterday, and you had to look to 5 decimal places to see that it just avoided that milestone, with an intraday low of $1.00003 during the European morning, ending the day just a hair lower versus the dollar, down -0.03% at $1.0037.

European equities staged a modest comeback from Monday’s selloff, while US equities ended lower after flirting with gains all day. The STOXX 600 gained +0.49%, with the DAX performing a touch better at +0.57%, bringing the STOXX 600 to just under flat for the week, while the DAX is still -0.84% lower on the week. The S&P 500 fell -0.92%, after trading near unchanged most of the day. Theories abounded for the late turnaround. Underlying market technicals pointed to potential algorithmic selling programs, whilst rumours spread in some circles that the CPI report was leaked and revealed a +10% print. Officials disabused us of the latter, but it nevertheless speaks to the heightened anxiety markets are trading with around inflationary data. In terms of the breakdown, energy shares (-2.03%) were the clear underperformer, but a wide-breadth of shares took a dip lower in the afternoon, sending the NASDAQ (-0.95%), FANG+ (-1.01%), and Russell 2000 (-0.22%) all lower on the day. So no clear macro driver for equities yesterday, but again, today’s CPI will be instructive about the near-term path.

Overnight in Asia equity markets are trading higher after recent losses. As I type, the Hang Seng (+0.81%) is leading gains across the region with the Kospi (+0.71%), Shanghai Composite (+0.36%), CSI (+0.26%), and the Nikkei (+0.33%) all trading up. Looking ahead, equity futures in the US point to a steady start with contracts on the S&P 500 (+0.14%) and NASDAQ 100 (+0.21%) moving higher.

Moving on to monetary policy action, the Bank of Korea (BOK) increased rates by 50bps, bringing the benchmark rate to 2.25% in order to help pullback inflation from a 24-yr high of 6%. The unprecedented rate hike size comes even as the central bank forecasts the country’s growth rate to lag “below the May forecast of 2.7%. Elsewhere, the Reserve Bank of New Zealand (RBNZ) in an expected move also increased its official cash rate (OCR) by 50bps for a third straight meeting to 2.5%.

Staying in Asia, another risk that’s been in a few headlines again is Covid. Partly this is because of the ongoing situation in China, where a steady stream of cases have been reported over recent days. But in addition to that, the US is considering whether to expand the recommendation of the second booster to all adults in light of the BA.5 omicron variant’s spread, and White House coronavirus coordinator Ashish Jha said that these discussions “have been going on for a while”. Of particular concern to officials, the BA.5 seems to evade immunity provided from prior infections.

Here in the UK, it’ll be another eventful day on the political scene as the first ballot of MPs takes place in the Conservative leadership election, which will also decide the next Prime Minister. 8 candidates will be on today’s ballot, and former Chancellor of the Exchequer Rishi Sunak is currently leading when it comes to MP’s endorsements, with yesterday seeing him gain that of Deputy PM Dominic Raab, among others. Candidates will need the support of at least 30 MPs today to progress onto the next ballot that takes place tomorrow.

There wasn’t much data yesterday, but the releases we did get only added to negative sentiment. First the German ZEW survey saw the expectations reading fall to its lowest level since the sovereign debt crisis at -53.8 (vs. -40.5 expected), whilst the current situation reading fell to -45.8 (vs. -34.5 expected). Separately, the NFIB’s small business optimism index from the US fell to 89.5 (vs. 92.5 expected).

To the day ahead now, and data releases include the US CPI release for June, as well as UK monthly GDP for May and Euro Area industrial production for May. Otherwise from central banks, the Bank of Canada will be making their latest policy decision, and the Federal Reserve will release their Beige Book.

Tyler Durden

Wed, 07/13/2022 – 07:57

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com