Key Events This Week: PCE, Durables And A Barrage Of Fed Speakers

First a quick word about the week which just passed: as DB’s Jim Reid notes, “I think everyone felt they were swimming in a tsunami of newsflow last week after one of the most incredible macro weeks in recent memory in terms of breadth of events. Yes there have been more extreme weeks in crises but last week had a bit more variety and was outside of a crisis period. If over 500bps of global rate hikes wasn’t enough, you also had 2yr US yields moving higher for the 12th successive day on Friday (the longest steak since data begins in 1976), the BoJ intervening in FX markets for the first time since 1998, and what can only be termed as one of the darker days for sterling assets on record on Friday after a mammoth tax giveaway in what was a mini-budget in name and not by nature.”

With that in mind, let’s go over the key event overnight, where the right-wing alliance led by Giorgia Meloni’s Brothers of Italy party was set to become the nation’s first woman prime minister after exit polls gave it a clear majority. With the full results due later today, she is predicted to win up to 26% of the vote ahead of her closest rival Enrico Letta from the centre left. The right wing alliance is slated to be on course for around 43% of the vote, enough for a majority if correct. Not surprisingly, the euro is extending its losses against the dollar for the fifth day, its longest streak since April 28, falling as much as -0.5% to 0.9638.

Looking at the week ahead, we have an array of consumer-driven economic data in the US and some important European inflation prints. We will also get a number of consumer sentiment indicators across the key economies and PMIs from Asia. Away from the data, there are more than 30 central banker appearances across the Fed and the ECB to keep markets busy. Tomorrow also sees referendums in the Russia-annexed Ukrainian territories as the conflict goes into its eight month.

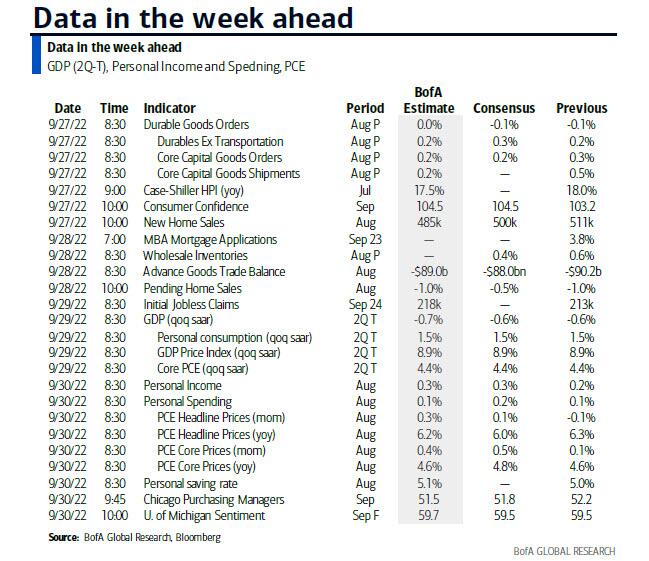

Going through the data in more details now. Starting with the US, the PCE and personal income and spending data will be front and centre for markets next week as they gauge the extent of inflationary pressures and the strength of the consumer. The Fed’s preferred inflation gauge, the PCE, due Friday, will be watched for signs of price pressures we saw in last week’s CPI report. DB economists expect core PCE to edge higher by +0.5% MoM (vs +0.1% in July) which won’t allow the Fed to take the foot off the tightening pedal. For the other two data points, DB forecasts a +0.1% MoM increase for both income and consumption. Final US Q2 GDP will also be released on Thursday and although DB expect no change to the -0.6% second reading, watch out for the annual benchmark revisions back to Q1 2017. History could be re-written that could have some implications for how we all think about the economy. In other US data, we will also get the consumer confidence index on Tuesday, along with durable goods orders, and inventories data on Wednesday, with the Chicago PMI on Friday.

Over in Europe, all eyes will be on September’s inflation data, including the Euro Area flash CPI release on Friday. Our economists are expecting the measure to hit a record +9.5%, up from the previous record of +9.1% in August. Other data in the region will include consumer and economic sentiment from Germany, France, Italy and the Eurozone throughout the week. Meanwhile, EU energy ministers will meet again on Friday regarding the emergency intervention amid elevated energy prices.

Finally, next week’s earnings line up will feature a number of retail bellwethers on Thursday. Among them will be Nike, H&M and Next. Micron will report that day as well. The day by day guide to the week below contains many of the key Fed and ECB speakers including Powell and Lagarde.

Courtesy of DB, here is a day-by-day calendar of events in the coming week:

Monday September 26

- Data: US September Dallas Fed manufacturing activity index, August Chicago Fed national activity index, Japan September PMIs, Germany September IFO survey

- Central banks: Fed’s Bostic speaks, ECB’s Lagarde, Nagel, Guindos, Centeno and Panetta speak, BoE’s Tenreyro speaks

- Other: OECD’s Interim Economic Outlook

Tuesday September 27

- Data: US September Conference Board consumer confidence index, Richmond Fed manufacturing index, August durable and capital goods orders, new home sales, July FHFA house price index, China August industrial profits, Japan August services PPI, Eurozone August M3

- Central banks: Fed’s Powell, Bullard and Evans speak, BoE’s Pill speaks, ECB’s Guindos, Panetta, Villeroy and Centeno speak

Wednesday September 28

- Data: US August advance goods trade balance, wholesale inventories, retail inventories, pending home sales, Germany October GfK consumer confidence index, France September consumer confidence, Italy September consumer and manufacturing confidence index, September economic sentiment, July industrial sales

- Central banks: Fed’s Daly, Bullard, Bostic and Evans speak, ECB’s Lagarde and Holzmann speak, BoE’s Cunliffe and Dingra speak

Thursday September 29

- Data: US third Q2 GDP reading, initial jobless claims, Germany September CPI, Italy August PPI, UK August consumer credit, mortgage approvals, M4, Eurozone September economic and industrial confidence

- Central banks: Fed’s Mester, Bullard and Daly speak, ECB’s Simkus, Panetta, Centeno, Villeroy, Knot, Elderson, Rehn, Guindos, Kazaks, Muller, de Cos and Lane speak, BoE’s Ramsden and Hauser speak

- Earnings: Nike, Micron, H&M, Next

Friday September 30

- Data: US September MNI Chicago PMI, August PCE core deflator, personal income and spending, China September PMIs, Japan September consumer confidence index, August jobless rate, retail sales, industrial production, department store, supermarket sales, housing starts, France, Italy and Eurozone September CPI, France August PPI, consumer spending, UK September Lloyds business barometer, Q2 current account balance, Germany September unemployment claims rate, Italy and Eurozone August unemployment rate

- Central banks: Fed’s Brainard and Williams speak, ECB’s Schnabel speaks

- Other: EU energy ministers meeting

* * *

Finally, looking at just the US, Goldman writes that the key economic data releases this week are the durable goods report on Tuesday and the core PCE report on Friday. There are several speaking engagements from Fed officials this week, including remarks by Chair Powell on Wednesday at a St. Louis Fed event on community banking and by Vice Chair Brainard on Friday at a New York Fed event on monetary policy and financial stability.

Monday, September 26

- 10:00 AM Boston Fed President Collins (FOMC voter) speaks: Boston Fed President Susan Collins will speak at a Boston Chamber of Commerce event. This will be Susan Collins’s first public appearance as President of the Boston Fed.

- 10:30 AM Dallas Fed manufacturing index, September (consensus -12.0, last -12.9)

- 12:00 PM Atlanta Fed President Bostic (FOMC non-voter) speaks: Atlanta Fed President Raphael Bostic will discuss income and wealth inequality during a virtual event hosted by the Washington Post. Audience Q&A is expected. On August 26th, President Bostic noted that a “restrictive [level of the federal funds rate] is somewhere in the 3.5-3.75% range.” While President Bostic emphasized that he did not expect a recession, he noted he was “hopeful” that tighter monetary policy would “start to bite,” and that he was “starting to hear signs that some of the supply-chain challenges that we’ve had … are starting to ease.” Since President Bostic’s remarks, the FOMC delivered a 75bp hike at its September meeting. The September Summary of Economic Projections showed a median projection for the federal funds rate at 4.375% for end-2022, implying that a 75bp hike in November is probably the Committee’s baseline. The median dot was 4.625% for end-2023, 3.875% for end-2024, and 2.875% for end-2025. We now expect the Fed to hike by 75bp in November, 50bp in December, and 25bp in February, to a terminal rate of 4.625%.

- 12:30 PM Dallas Fed President Logan (FOMC non-voter) speaks: Dallas Fed President Lorie Logan will take part in a moderated discussion at an event in Fort Worth hosted by the Independent Bankers Association of Texas. Audience Q&A is expected. This will be Lorie Logan’s first public appearance as President of the Dallas Fed.

- 04:00 PM Cleveland Fed President Mester (FOMC voter) speaks: Cleveland Fed President Loretta Mester will discuss the economic outlook at an event hosted by MIT. Text and audience Q&A are expected. On September 7th, President Mester argued that “it will be necessary to move the nominal fed funds rate up to somewhat above 4% by early next year and hold it there,” adding that she does not “anticipate the Fed [to cut] the fed funds rate target next year.” President Mester also noted that it was “far too soon to conclude that inflation has peaked, let alone that it is on a sustainable downward path to 2 percent,” stressing that “services inflation … is at its highest level since the early 1990s,” and that “given developments related to the ongoing war in Ukraine, gas and energy prices may move higher again later this year.” Since President Mester’s remarks, core CPI surprised to the upside in August, with broad-based strength in cyclical and wage-sensitive services categories including shelter, restaurants, medical care, education, and personal care.

Tuesday, September 27

- 03:30 AM Chicago Fed President Evans (FOMC non-voter) speaks: Chicago Fed President Charles Evans will take part in an interview on CNBC Europe. On September 8th, President Evans said he expected growth to be “pretty decent” in 2023. President Evans noted that he expected the labor market would “only … slow a bit,” and that he thought it was “possible that the number of vacancies [could] decline without serious increases in unemployment.”

- 06:15 AM Chicago Fed President Evans (FOMC non-voter) speaks: Chicago Fed President Charles Evans will discuss the outlook for the economy and monetary policy at an event in London hosted by the Official Monetary and Financial Institutions Forum.

- 07:30 AM Fed Chair Powell speaks: Fed Chair Jerome Powell will take part in a panel discussion on digital currencies hosted by the Bank of France. Moderated Q&A is expected. At the press conference following the FOMC’s September meeting, Chair Powell noted that the Committee was moving its policy stance “purposefully to a level that will be sufficiently restrictive to return inflation to 2 percent.” As discussed in our FOMC recap, Chair Powell’s discussion of what the FOMC needs to see to slow the pace of tightening put a bit more emphasis on inflation than his remarks following the FOMC’s July meeting. And while Chair Powell had emphasized in the July press conferences that the FOMC is aiming for below-potential growth, not a recession, he dropped the latter half of that point this time.

- 08:30 AM Durable goods orders, August preliminary (GS -0.7%, consensus -0.1%, last -0.1%); Durable goods orders ex-transportation, August preliminary (GS +0.3%, consensus +0.3%, last +0.2%); Core capital goods orders, August preliminary (GS +0.4%, consensus +0.2%, last +0.3%); Core capital goods shipments, August preliminary (GS +0.7%, consensus +0.3%, last +0.5%): We estimate that durable goods orders fell 0.7% in the preliminary August report, reflecting a pullback in commercial aircraft orders. However, we also expect a continued solid rise in shipments of core capital goods (+0.7%) due to strong domestic production trends and higher prices. We assume a more moderate rise in new orders for that category (+0.4%) due to softening foreign demand in August.

- 09:00 AM FHFA house price index, July (consensus +0.1%, last +0.1%)

- 09:00 AM S&P/Case-Shiller 20-city home price index, July (GS +0.2%, consensus +0.20%, last +0.44%): We estimate that the S&P/Case-Shiller 20-city home price index rose 0.2% in July, following a 0.44% (18.65% yoy) increase in June.

- 09:55 AM St. Louis Fed President Bullard (FOMC voter) speaks: St. Louis Fed President James Bullard will discuss the economic outlook during a policy forum in London. Audience Q&A is expected. On August 18th, President Bullard noted that his “baseline would be that probably inflation will be more persistent than what many on Wall Street expect, and that it’s going to be higher for longer.”

- 10:00 AM Conference Board consumer confidence, September (GS 103.5, consensus 104.0, last 103.2): We estimate that the Conference Board consumer confidence index increased to 103.5 in September.

- 10:00 AM Richmond Fed manufacturing index, September (consensus -11, last -8)

- 10:00 AM New home sales, August (GS -1.0%, consensus -2.2%, last -12.6%): We estimate that new home sales declined 1.0% in August, following 12.6% decline in July.

- 08:35 PM San Francisco President Mary Daly (FOMC non-voter) speaks: San Francisco Fed President Mary Daly will take part in a moderated Q&A at a banking symposium in Singapore. On August 18th, President Daly argued that the Fed needed to “get the rate up, … likely to restrictive territory,” and that the “raise-and-hold strategy … has historically paid off for us.” President Daly also noted that the Fed was “facing a global economy that is growing slower, … [that] that will push back on US growth,” and that the FOMC needed “to take that into consideration.”

Wednesday, September 28

- 08:30 AM Advance goods trade balance, August (GS -$87.0bn, consensus -$88.8bn, last -$90.2bn): We estimate that the goods trade deficit narrowed by $3.2bn to $87.0bn in August compared to the final July report, reflecting a decrease in imports.

- 08:30 AM Wholesale inventories, August preliminary (consensus +0.5%, last +0.6%)

- 08:35 AM Atlanta Fed President Bostic (FOMC non-voter) speaks: Atlanta Fed President Raphael Bostic will take part in a moderated Q&A on leadership hosted by the Atlanta Fed. Audience and media Q&A is expected.

- 10:00 AM Pending home sales, August (GS flat, consensus -1.0%, last -1.0%): We estimate pending home sales were flat in August, following a 1.0% decline in July.

- 10:10 AM Fed Chair Powell, St. Louis Fed President Bullard (FOMC voter), and Fed Governor Bowman speak: Fed Chair Jerome Powell and St. Louis Fed President James Bullard will deliver welcoming remarks and Fed Governor Michelle Bowman will give a speech on the new landscape for banking competition at a community banking event hosted by the St. Louis Fed. Prepared text for Chair Powell’s remarks and Governor Bowman’s speech is expected. On August 6th, Governor Bowman noted that “similarly-sized increases” in the federal funds rate to the FOMC’s 75bp hikes in June and July “should be on the table until we see inflation declining in a consistent, meaningful, and lasting way.”

- 02:00 PM Chicago Fed President Evans (FOMC non-voter) speaks: Chicago Fed President Charles Evans will discuss the economic outlook during an event hosted by the London School of Economics. Media Q&A is expected.

Thursday, September 29

- 08:30 AM GDP (third), Q2 (GS -0.6%, consensus -0.6%, last -0.6%): Personal consumption, Q2 (GS +1.5%, consensus +1.5%, last +1.5%): We estimate no revision on net in the third vintage of the Q2 GDP report (previously reported at -0.6% qoq ar). The release will also include the quinquennial comprehensive update, benchmarking the 2017 GDP data to the economic census of that year and updating the 2017-2022 quarterly series based on the latest data available.

- 08:30 AM Initial jobless claims, week ended September 24 (GS 215k, consensus 218k, last 213k); Continuing jobless claims, week ended September 17 (consensus 1,393k, last 1,417k): We estimate initial jobless claims edged up to 215k in the week ended September 24.

- 09:30 AM St. Louis Fed President Bullard (FOMC voter) speaks: St. Louis Fed President James Bullard will discuss the economic outlook at a virtual forum on emerging markets. Audience and media Q&A is expected.

- 01:00 PM Cleveland Fed President Mester (FOMC voter) speaks: Cleveland Fed President Loretta Mester and ECB Executive Board member Philip Lane will take part in a policy panel during a Cleveland Fed conference on inflation.

- 04:45 PM San Francisco Fed President Daly (FOMC non-voter) speaks: San Francisco Fed President Mary Daly will deliver a speech at Boise State University. Text and media Q&A are expected.

Friday, September 30

- 08:30 AM Personal income, August (GS +0.4%, consensus +0.3%, last +0.2%); Personal spending, August (GS +0.4%, consensus +0.2%, last +0.1%); PCE price index, August (GS +0.23%, consensus +0.2%, last -0.07%); PCE price index (yoy), August (GS +6.12%, consensus +6.1%, last +6.28%); Core PCE price index, August (GS +0.49%, consensus +0.5%, last +0.08%); Core PCE price index (yoy), August (GS +4.74%, consensus +4.7%, last +4.56%): Based on details in the PPI, CPI, and import price reports, we forecast that the core PCE price index rose by 0.49% month-over-month in August, corresponding to a 4.74% increase from a year earlier. Additionally, we expect that the headline PCE price index increased by 0.23% in August, corresponding to a +6.12% increase from a year earlier. We expect that personal income and spending both increased by 0.4% in August.

- 09:00 AM Fed Vice Chair Brainard speaks: Fed Vice Chair Lael Brainard will deliver opening remarks at a conference hosted by the New York Fed on monetary policy and financial vulnerabilities. Text is expected. On September 23rd, Vice Chair Brainard noted that “wages haven’t kept up with inflation and inflation is very high,” and emphasized that “inflation … puts special burdens on lower-income families as well as on people with fixed incomes.” Earlier, on September 7th, Vice Chair Brainard argued that “monetary policy will need to be restrictive for some time to provide confidence that inflation is moving down to target,” while noting that “the economic environment is highly uncertain, and the path of policy will be data dependent.”

- 09:45 AM Chicago PMI, September (GS 54.5, consensus 59.5, last 59.5): We estimate that the Chicago PMI declined 5pt to 54.5 in September, reflecting weak industrial trends abroad and the Chicago PMI’s elevated level relative to other business surveys, which were mixed in the month (GS manufacturing survey tracker +0.3pt to 50.3).

- 10:00 AM University of Michigan consumer sentiment, September final (GS 60.5, consensus 59.5, last 59.5): We expect the University of Michigan consumer sentiment index increased by 1.0pt to 60.5 in the final September reading.

- 11:00 AM Fed Governor Bowman speaks: Fed Governor Michelle Bowman will give a speech on large bank supervision at a virtual event hosted by the Institute of International Finance. Text and moderated Q&A are expected.

- 12:30 PM Richmond Fed President Barkin (FOMC non-voter) speaks: Richmond Fed President Thomas Barkin will give a speech on the drivers of inflation during an event hosted by George Mason University. Text, audience, and media Q&A are expected. On September 7th, President Barkin noted that he has “a bias in general towards moving more quickly, rather than more slowly, as long as you don’t inadvertently break something along the way,” and argued that “the destination is real rates in positive territory and my intent would be to maintain them there until such time as we really are convinced that we put inflation to bed.”

- 04:15 PM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will make closing remarks at a conference hosted by the New York Fed on how monetary policy affects financial vulnerabilities. On August 30th, President Williams noted that the Fed needs “to get not just to neutral in a real interest rate sense, but you’re actually trying to get … demand in line with supply.” President Williams also noted that the economy was “coming into … the second half of the year … still with some positive momentum,” and emphasized that “the economy’s growing [and] the labor market is very strong.”

Source: DB, Goldman, BofA

Tyler Durden

Mon, 09/26/2022 – 09:44

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com