A Policy Mistake In The Making

Authored by Lance Roberts via RealInvestmentAdvice.com,

“Market Instability” Causes BOE To Reverse QT. Is The Fed Next?

“Market instability” remains the most significant risk to central banks globally. Despite their desire to combat surging inflation, market instability is a greater risk to global economies due to the massive amounts of leverage. We previously discussed the importance of controlling instability. To wit:

“Interestingly, the Fed is dependent on both market participants and consumers, believing in this idea. With the entirety of the financial ecosystem now more heavily levered than ever due to the Fed’s profligate measures of suppressing interest rates and flooding the system with excessive levels of liquidity, the “instability of stability” is now the most significant risk.

The ‘stability/instability paradox’ assumes that all players are rational, and such rationality implies avoidance of complete destruction. In other words, all players will act rationally, and no one will push ‘the big red button.’”

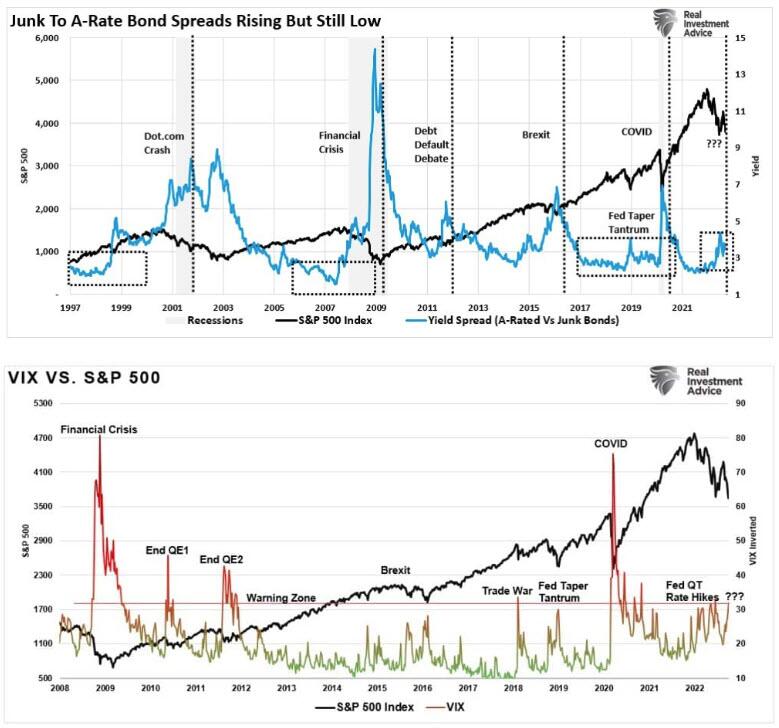

So far, the Fed remains fortunate with a low volatility decline in markets. In other words, “market stability” continues to afford the Federal Reserve the operating room needed for the most aggressive rate hiking campaign since the late 70s. Market volatility and credit spreads remain “well contained” despite drastically higher interest rates and an ongoing stock market decline.

However, stable markets can become unstable rapidly when something breaks due to rising rates or volatility. The Bank of England (BOE) is an excellent example of what happens when things go awry. The BOE was forced to start buying bonds to solve a potential crisis with U.K. pension funds. The pension funds receive margin with yields fall and post additional collateral when yields rise. However, when yields spike, as they have recently, the pension funds are hit with “margin calls,” which have the potential to cause market instability. Due to leverage built up through the entire financial system, market instability can spread like a virus through global markets. Such was last seen with the Lehman Crisis in 2008.

Is the BOE’s actions an isolated event? Maybe not. According to Charles Gasparino, the Fed could be next.

SCOOP (1/2): @federalreserve officials getting increasingly worried about “financial stability” as opposed to inflation as higher rates begin to crush bonds, several big investors tell me. Fed growing worried about possible “Lehman Moment” w a 4% FF rate as Bonds and derivatives

— Charles Gasparino (@CGasparino) September 30, 2022

The Market Instability Risk

The Federal Reserve is deeply committed to its aggressive campaign to quell surging inflation. As Jerome Powell stated at this year’s Jackson Hole Summit:

“Restoring price stability will take some time and requires using our tools forcefully to bring demand and supply into better balance. Reducing inflation is likely to require a sustained period of below-trend growth. Moreover, there will very likely be some softening of labor market conditions. While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses. These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain.”

While the Federal Reserve is willing to cause “some pain” to achieve victory, they hope to do so without evoking a recession. Such may be a challenge for two primary reasons:

-

The Fed remains focused on lagging economic data, such as employment, which are highly subject to future revisions, and;

-

Changes to monetary policy do not show up in the economy until roughly 9-12 months in the future.

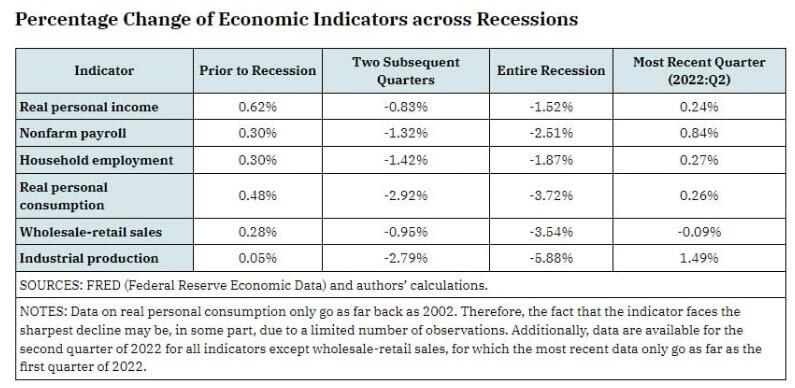

The problem with the Fed’s use of economic data to guide monetary policy decisions was the subject of a St. Louis Federal Reserve research note. To wit:

“In the two quarters leading up to the average recession, all measures were still experiencing varying degrees of positive growth. Meanwhile, immediately following the onset of the average recession, all six indicators declined, which ultimately persisted for the entirety of the recession.”

Such brings us to the second most critical point.

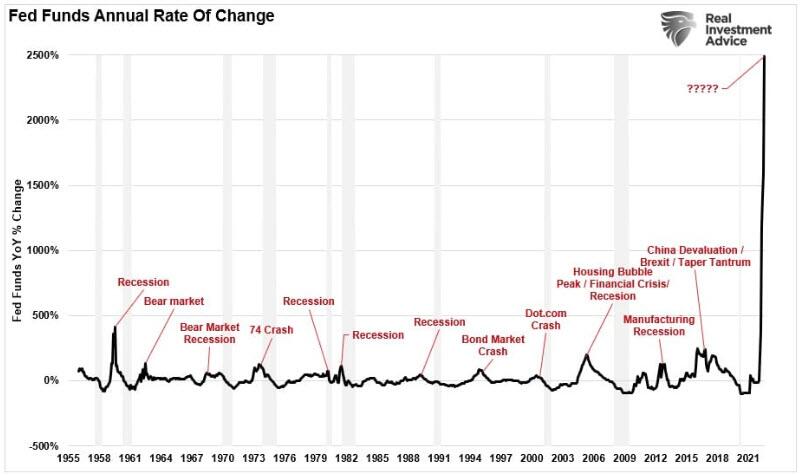

Changes to monetary policy have a 9-12 month lag before showing up in the economy. Therefore, as the Fed is hiking rates based on lagging economic data, the risk of a “policy mistake” becomes heightened. By the time the economic data deteriorates, the preceding rate hikes have yet to impact the economy, which eventually deepens the recession.

As shown, the annual rate of change of the Fed Funds rate is now the most aggressive increase in history. However, every previous rate hiking campaign has led to a recession, bear markets, or economic event.

However, the Federal Reserve does not operate in an economic vacuum. Other factors also contribute to the tightening of monetary policy and the impact on economic growth. When those other factors such as higher interest rates, falling asset prices, or a surging dollar coincide with the Fed’s policy campaign, the risk of “market instability” increases.

A Policy Mistake In The Making

The current bout of inflation is vastly different than that seen in the late 70s.

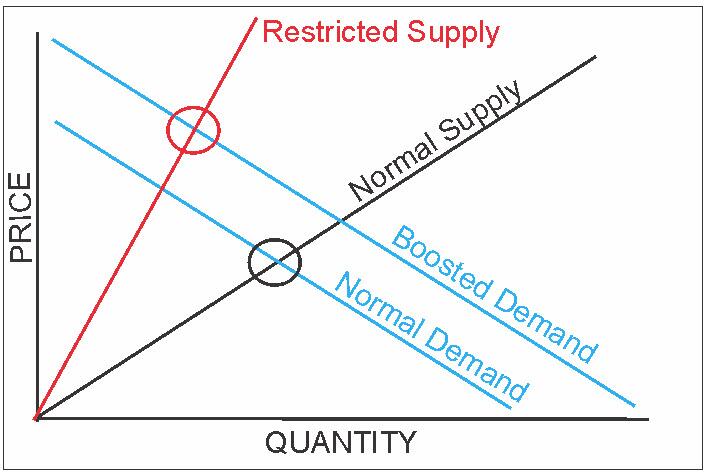

Milton Friedman once stated corporations don’t cause inflation; governments create inflation by printing money. There was no better example of this than the massive Government interventions in 2020 and 2021 that sent subsequent rounds of checks to households (creating demand) when an economic shutdown constrained supply due to the pandemic.

The following economic illustration shows such taught in every “Econ 101” class. Unsurprisingly, inflation is the consequence if supply is restricted and demand increases by providing “stimulus” checks.

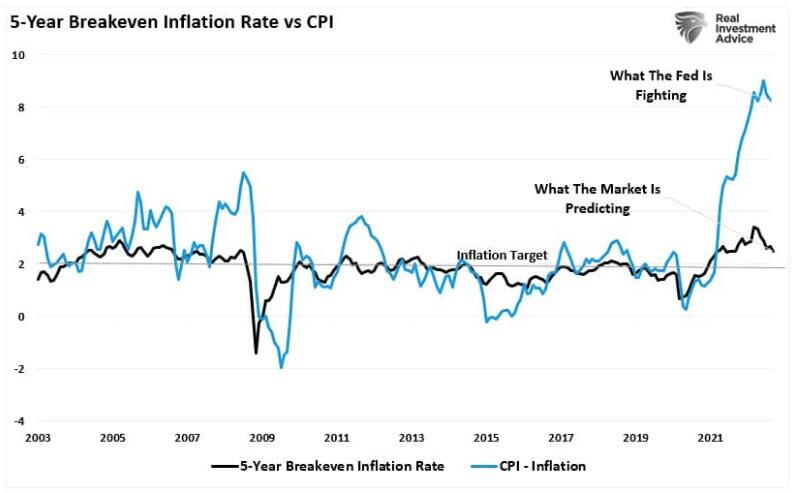

The problem for the Fed is the influence of lagging economic data on its decisions. In contrast, forward estimates for inflation are already falling quickly as economic demand falters due to collapsing liquidity.

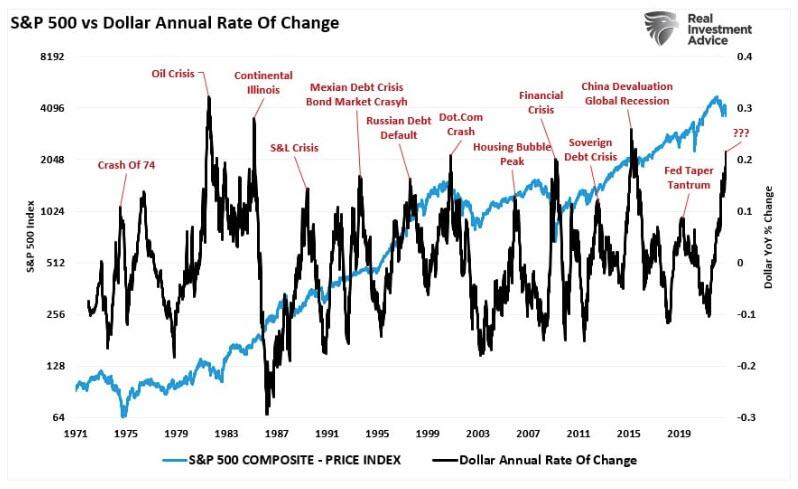

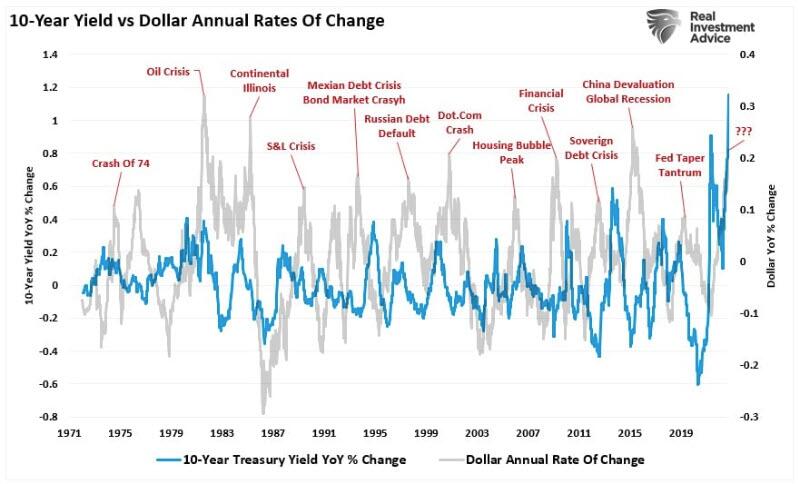

Historically, the “best cure for high prices is high prices.” In other words, inflation would resolve itself as high costs curtail consumption. However, the Fed is not operating in a vacuum. While the Fed is hiking interest rates to slow economic activity, interest rates and the dollar have also increased dramatically in recent months. Those increases apply further downward economic pressures by increasing costs domestically and globally. Not surprisingly, sharp annual increases in the dollar are coincident with market instability and economic fallout.

Furthermore, the surge in the dollar accompanied the sharpest increase in interest rates in history. Sharp increases in interest rates, particularly in a heavily indebted economy, are problematic as debt servicing requirements and borrowing costs surge. Interest rates alone can destabilize an economy, but when combined with a surging dollar and inflation, the risks of market instability increase markedly.

The Fed Will Blink

After more than 12 years of the most unprecedented monetary policy program in U.S. history, the Federal Reserve has put itself into a poor situation. They risk an inflation spiral if they don’t hike rates to quell inflation. If the Fed hikes rates to kill inflation, the risk of a recession and market instability increases.

As noted at the outset, the behavioral biases of individuals remain the most serious risk facing the Fed. For now, investors have not “hit the big red button,” which gives the Fed breathing room to lift rates. However, the BOE discovered that market instability surfaces quickly when “something breaks.”

When will the Fed find the limits of its monetary interventions? We don’t know, but we suspect they have already passed the point of no return, and history is an excellent guide to the adverse outcomes.

-

In the early ’70s, it was the “Nifty Fifty” stocks,

-

Then Mexican and Argentine bonds a few years after that

-

“Portfolio Insurance” was the “thing” in the mid -80’s

-

Dot.com anything was an excellent investment in 1999

-

Real estate has been a boom/bust cycle roughly every other decade, but 2007 was a doozy.

-

Today, it’s real estate, FAANNGT, debt, credit, private equity, SPACs, IPOs, “Meme” stocks…or rather…” everything.”

The Federal Reserve continues to state its intentions to hike rates and reduce its balance sheet at the fastest pace in history, as inflation is the enemy it must defeat. However, while high inflation is detrimental to economic growth, market instability is far more insidious. Such is why the Federal Reserve rushed to bail out banks in 2008.

Unfortunately, we doubt the Fed has the stomach for “market instability.” As such, we doubt they will hike rates as much as the market currently expects.

Tyler Durden

Tue, 10/04/2022 – 16:20

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com