JPMorgan Warns FTX Collapse Will Spark “Cascade Of Margin Calls”

Unlike the high profile crypto-linked blowups earlier this year, JPMorgan believes that there is something different about the ongoing FTX implosion.

First the bad news: as JPM flows and liquidity strategist Nick Panigirtzoglou writes overnight, “given the size and interlinkages of both FTX and Alameda Research with other entities of the crypto ecosystem including DeFi platforms it looks likely that a new cascade of margin calls, deleveraging and crypto company/platform failures is starting similar to what we saw last May/June following the collapse of Terra.”

Then again, this is the same Panigirtzoglou who just a few weeks ago was busy praising crypto’s nascent recovery. Nothing like a one-off event to totally U-turn your entire thesis.

To be sure, that doesn’t mean he is wrong, and this is how he frames the current quandary facing the crypto space – the $8bn of Alameda Research liabilities reported in the press “is big enough to create a similar wave of deleveraging to that seen following the $20bn Terra USD collapse last May. And similar to what we saw after the collapse of Terra USD, this deleveraging is likely to last for at least a few weeks unless a rescue for Alameda Research and FTX is agreed quickly.”

Yet what makes this new phase of deleveraging more problematic is that the number of entities with stronger balance sheets able to rescue those with low capital and high leverage is shrinking within the crypto ecosystem. If nothing else, SBF was frequently referred to as the next JPMorgan (not any more). FTX and Alameda Research had emerged last May/June as the main entities with apparently strong balance sheets to rescue weaker and more leveraged entities such as BlockFi, Voyager Digital and Celsius.

But now that the balance sheet strength of Alameda Research and FTX is under question only a few months after being perceived as strong balance sheet entities, it creates a confidence crisis and reduces the appetite of other crypto companies to come to the rescue.

What is certain, according to Panigirtzoglou, is that the collapse of Alameda Research/FTX will increase investor and regulatory pressure on crypto entities to disclose more information about their balance sheets, to safeguard client assets, to limit asset concentration and will induce more diligent risk management including management of counterparty risk among crypto market participants.

Paradoxically, FTX had been preferred over Binance by institutional clients such as hedge funds, so the past days’ events will likely change the way institutional investors interact with exchanges to ensure their assets are protected.

In this context, JPM notes that it is encouraging that nine exchanges including Binance, Gate.io, KuCoin, Poloniex, Bitget, Huobi, OKX, Deribit and Bybit have issued statements that they would publish their Merkle tree reserve certificates to increase transparency. Merkle trees allow Exchanges to store each user account’s hash value of assets in the leaf nodes of the Merkle tree. Assets on a leaf node can be audited and verified by a third party

On the positive side, and while it might take several weeks until the current deleveraging cycle peaks, the JPM strategist believes that “the hit to crypto market cap is likely to be smaller than post Terra given previous deleveraging.”

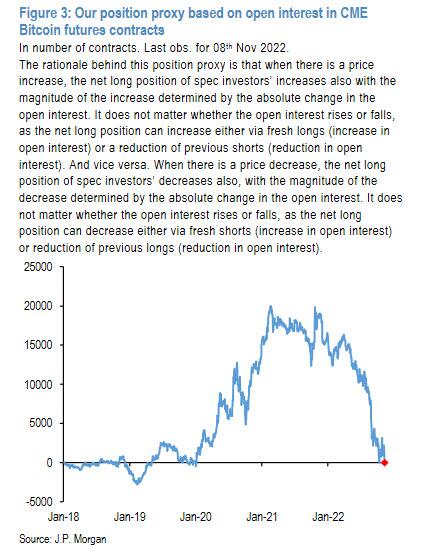

One metric to quantify the previous deleveraging is shown in the chart below, which depicts JPM’s position proxy for CME bitcoin futures: this position proxy stands close to levels last seen in January 2020 pointing to rather advanced deleveraging.

The deleveraging phase that followed the Terra collapse had induced a 50% decline in crypto market cap from around $1.7tr at the beginning of May to a low of $0.86tr by mid-June. With the crypto market cap standing at just above $1tr before the FTX/Alameda Research collapse, JPM’s guess is that the crypto market will find a floor above $500bn in the current deleveraging phase.

Another way of thinking about the downside from here is the bitcoin production cost which historically acted as a floor for the bitcoin price. At the moment, this production cost stands at $15k but it is likely to revisit the $13k low seen over the summer months. A production cost of $13k implies 25% downside from here which would bring the crypto market cap to a low of $650bn.

More in the full JPM report available to pro subs in the usual place.

Tyler Durden

Thu, 11/10/2022 – 18:00

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com