China Considers Stimulus, Higher Deficit Spending To Counter Property Bust

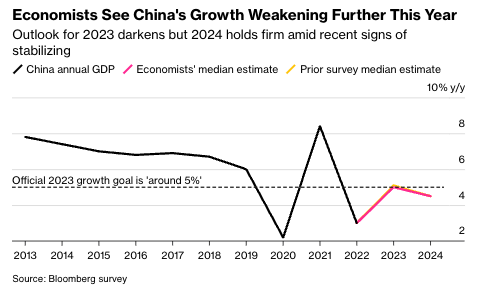

Wall Street analysts have recently cut China’s 2023 and 2024 economic growth. The world’s second-largest economy is at serious risk of missing Beijing’s GDP growth target for the second consecutive year and expanding below 5% for three years straight years – something not seen since the death of Mao Zedong in 1976.

A multi-year property downturn looks increasingly likely as China’s state-owned property developers now warn of widespread losses, fueling concerns that the housing crisis is expanding from the private sector to government-backed companies. Also, deflationary pressure has capped growth goals around 5%.

To counter the downturn, Beijing needs to deploy countercyclical policy tools. According to Bloomberg, citing people familiar with the matter, the government could soon announce a new wave of stimulus and expand the budget deficit above the 3% cap set in March. Another person said the official announcement about these new policies could come as early as this month but stressed talks are still ongoing.

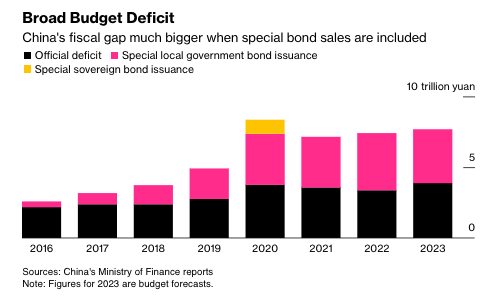

“Policymakers are weighing the issuance of at least 1 trillion yuan ($137 billion) of additional sovereign debt for spending on infrastructure such as water conservancy projects,” said the people.

Until now, the government has refrained from implementing extensive fiscal stimulus, even in the face of a worsening property downturn and increasing deflationary pressures. Maybe optically, Beijing wants more robust growth than the US amid rising tensions.

{kind=link}

“The ad hoc issuance of additional debt from the central government could provide extra policy support and more resources to re-engineer a stronger and faster recovery,” said Bruce Pang, chief economist at Jones Lang Lasalle Inc. “

Pang said, “China’s recovery story could be a relay race” stimulated by infrastructure spending and then fueled by spending among businesses and households.

“The plans, led by the Ministry of Finance and the National Development and Reform Commission, are subject to final approval by the State Council and legislators,” the people added.

According to Xiaojia Zhi, head of research at Credit Agricole CIB, the size of additional issuance under discussion is “modest,” or equivalent to about 0.7% of GDP.

“But the message would be positive,” Zhi said, adding that it’s a “reasonable consideration” given soft private demand, tight local fiscal conditions, and the ongoing property sector downturn. “The central government’s debt ratio remains low, and its balance sheet is still quite healthy.”

Here’s a summary of what Wall Street analysts are saying about potential new stimulus from China (list courtesy of Bloomberg):

Tommy Xie, an economist at Oversea-Chinese Banking Corp. Ltd.

- “I perceive this development as a constructive step toward addressing the issue of local government debt. While China’s aggregate government debt-to-GDP ratio aligns with those of many developed economies, the country’s distinct debt structure presents its own set of challenges.”

- “The proposition to enable the central government to assume a larger portion of the debt emerges as a viable solution. This approach could alleviate the financial strain on local governments, fostering an environment where resources can be reallocated and optimized to stimulate growth and bolster economic sentiment.”

Xiaojia Zhi, head of research at Credit Agricole CIB

- “China should do more to show they are committed to stabilize growth and boost demand. A modestly higher deficit by the central government should not be too concerning to investors. It’s necessary for the central bank to shoulder more responsibility to boost fiscal spending and stimulate demand.”

- “While this is yet to be confirmed, I think this is a reasonable consideration, given that private demand is still soft, and local fiscal conditions remain tight given the property sector downturn. The central government debt ratio remains low, and its balance sheet still quite healthy. One trillion yuan is a modest amount — about 0.7% GDP — but the message would be positive.”

Kiyong Seong, lead Asia macro strategist at Societe Generale SA

- “Mulling an additional bond issuance at this time of the year is a positive surprise. However, a speculated destination of infrastructure investment will dilute the positive impact. Therefore, there could be a marginal upside risk to China rates, but no meaningful downside impact on USD/CNY.”

- “An additional bond issuance is not free, probably at the expense of a bit higher yields or at least smaller scale of a decline in bond yields going forwards. Then, it would be better to be spent on the area with more direct effect on consumption recovery.”

Ding Shuang, chief economist for greater China and North Asia at Standard Chartered Plc.

- “The initiative would sound more reasonable if it was contemplated three months ago, when China just suffered a setback in its post-Covid recovery in the second quarter. Given the fiscal room under the approved budget is not fully utilized, and the economy has seen marginal improvement in August and September, I think the timing of introducing additional fiscal stimulus is questionable.”

He Wei, China economist at Gavekal Dragonomics

“It will lift the economy and increase the chance for China to reach GDP growth of 5% this year. If the additional sovereign debt can be used in time, it will bring a decent quarterly growth in the fourth quarter.”

Talk of a new round of stimulus comes as readers have been well-informed about the worsening property bust:

- Traders Brace For China’s Property Slump To Drag For Years

- China’s Housing Slump Far Worse Than Reported; Half Of State-Owned Builders Warn Of “Widespread” Losses

- Six Red Flags Pointing To China’s Economic Slowdown

{kind=link}

If Bloomberg’s report turns out to be just rumors – and no stimulus is seen – then the global economy will likely continue to deteriorate as most US CEOs warn of recession in 2024.

Tyler Durden

Tue, 10/10/2023 – 07:45

source

This post has been republished with implied permission from a publicly-available RSS feed found on Zero Hedge. The views expressed by the original author(s) do not necessarily reflect the opinions or views of The Libertarian Hub, its owners or administrators. Any images included in the original article belong to and are the sole responsibility of the original author/website. The Libertarian Hub makes no claims of ownership of any imported photos/images and shall not be held liable for any unintended copyright infringement. Submit a DCMA takedown request.

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com